WEEK IN A NUTSHELL

WIN-dow to the week that was

Week in a Nutshell (WIN)

Week

ended

th

13 July

2012

Key WIN-dicators

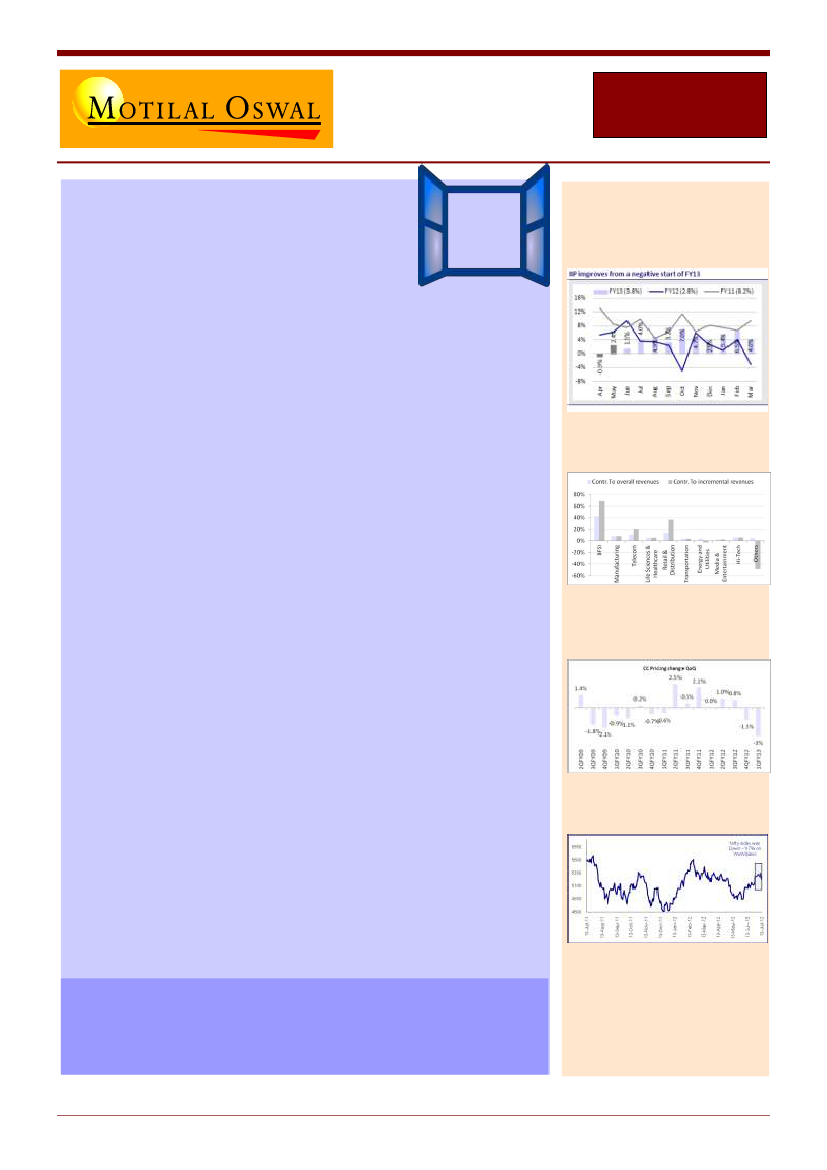

May IIP growth recovers to 2.4%

If ever the term “Lacking direction” is to be used it is now. Month on month

NIFTY has closed up a mere 1.6%. This lack of movement though hides large

inflows seen month to date with USD1.3B of equity investments, which dwarfs

the flows into peer markets in the region. The YTD number is just as divergent

with ~USD10B of inflows into India while the closest markets have pulled in less

than half this amount. This coincides with our PM and acting FM acknowledging

actions are required to build investor confidence. Should these materialize, we

are staring at potentially record inflow numbers for the year?

DO WE HAVE A NEW BELLWETHER IN INDIAN IT?

TCS once again beat expectations

and more importantly outpaced Infosys on all parameters. While dollar revenues

contracted for Infosys, TCS continued to grow, even outstripping on the volume

front. On margins as well TCS fared better on the back of better utilization rates.

Mgmt outlook continued as divergent with TCS top brass defying any macro

impacts and seeing continued opportunities and orders while Infosys mgmt cited

low near-term visibility which has worsened in the last quarter.

PRIVATE BANKS JUSTIFY VALUATIONS

Both HDFC Bank and Indusind came in with

results that justify their premium valuations. HDFC Bank surprised on both NIM as

well fee income, while its franchise continues to build on liabilities with 18%

increase in SA YoY.

Indusind Bank

delivered impressive numbers in a stressed liquidity situation, with

continued SA deposit growth, strong corporate loan and fee income growth. The

only point of concern is on the promoter ownership which is to be reduced to 10%

from the current ~19%. With QIP around the corner, this QIP + the reduction in

promoter stake should be the last big supply in the stock, which will be easily

lapped up by the fence sitters in the stock. Please read detailed notes

MAY IIP GROWTH RECOVERS TO 2.4%

while above expectations and signaled

moderate recovery of industry, Apr data saw downward revision. Capital Goods

sector saw continued downturn and in our belief this reading does not change the

st

growth-inflation balance. We expect RBI to cut policy rates by 50bps in its July 31

policy announcement.

TCS: BFSI, Telecom and Retail were

the key growth verticals

CC Pricing cut of 3% QoQ was a key

negative surprise in 1QFY13

WoW - Nifty Change (-1.7%)

Some of the highlights of this edition:

TCS & Infosys Result Highlights

Dr Reddy’s and ONGC management meeting highlights

Updates from NMDC site visit

WWW – WIN Weekend Wisdom

The history of the stock markets tells us that they will surprise

us in the future

WIN – Week In a Nutshell

1

13

th

July

2012