Sector Update | 21 March 2017

Aviation

Aviation

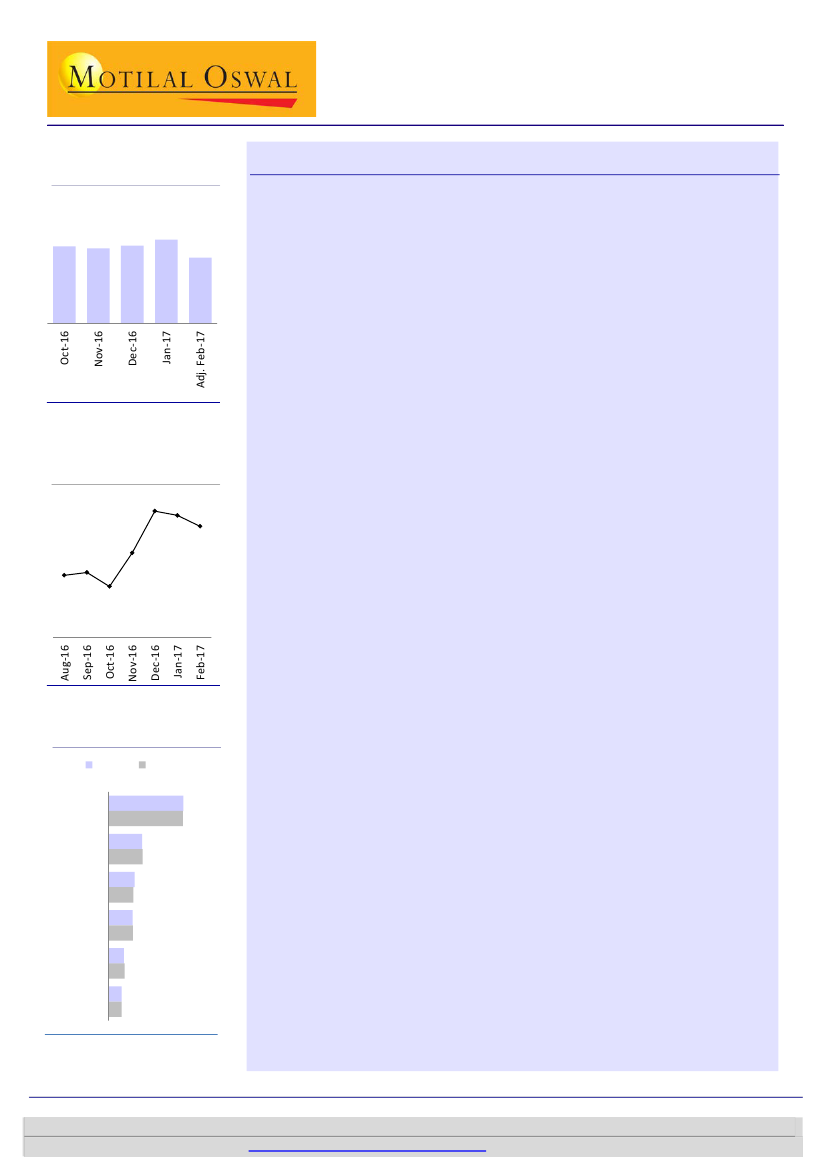

Domestic passenger growth

(YoY %)

Feb-16 domestic air passenger growth at ~20% YoY

Domestic load factor at 87.2%; IndiGo’s domestic ASK/RPK share highest

25.3

23.3 22.6 23.4

19.9

Domestic air passengers in India grew ~20% YoY (adj.) in Feb-17 (v/s +25.3% in Jan-17;

+23.1% in 3QFY17). However, we believe this strong growth would be at the cost of

yields, as seen in headline fares.

While Feb-17 ASK growth stood at 17.8% YoY (adj.) (v/s +21.1% in 3QFY17 and +19% in

2QFY17), RPKs increased 21% YoY (adj.) (v/s +22.8% in 3QFY17 and +24.5% in 2QFY17).

Load factor stood at 87.2% in Feb-17 (v/s 84.8% in 3QFY17 and 83% in 2QFY17).

*adj.:

With 2016 being a leap year, we adjust pax/ASK/RPK numbers to calculate YoY change for Feb-17.

Domestic air passenger growth at ~20% YoY in Feb-17

88.7

87.2

82.5

82.2

81.1

84.5

Industry load factor (%)

88.3

India’s domestic air passengers grew ~20% YoY (adj.) in Feb-17. Domestic

passenger growth remained ~20% and above for the 16

th

straight month.

IndiGo’s passenger growth stood at +28.6% YoY (adj.) in Feb-17 (v/s +43% in

3QFY17 and +39% in 2QFY17).

SpiceJet’s domestic passenger volumes grew +20% YoY (adj.) in Feb-17 (v/s

+22% in 3QFY17).

Go Air’s domestic passenger volumes grew +30.4% YoY (adj.) in Feb-17 (v/s

+19% in 3QFY17).

Passenger volume growth (adj.) YoY for other airlines was as follows: Jet Airway:

+3.6% YoY (v/s +1.3% in 3QFY17); Air India: +4.9% (v/s +2% in 3QFY17).

IndiGo’s passenger market share stood at ~40% in Feb-17 (v/s +41.8% in 3QFY17

and +40% in 2QFY17).

Jet Airways’ market share remained below 20% for the eleventh consecutive

month at 18.3%. It had market share of above 20% since Jul-14.

Air India’s market share stood at 13.3% (v/s 13.1% in 3QFY17).

SpiceJet’s market share stood at 13.3% (v/s 12.8% in 3QFY17).

GoAir’s market share stood at 8.7% in Feb-17; it seems to have stabilized in the

8-9% range.

IndiGo’s domestic ASKs increased +23.5% YoY (adj.) (v/s +34% in 3QFY17); its

domestic ASK share stood at the highest at 41.5%.

SpiceJet’s domestic ASKs grew +23.4% YoY (adj.) (v/s +19.8% in 3QFY17).

Domestic ASKs of GoAir grew +20.3% YoY (adj.) (v/s +13.5% in 3QFY17) and

those of Jet grew +3% YoY (adj.) (v/s +3% in 3QFY17).

IndiGo’s RPKs grew +25.9% YoY (adj.) (v/s +38.9% in 3QFY17), with the highest

market share of 41.7% in Feb-17.

SpiceJet’s domestic RPKs grew +25.2% (adj.) YoY (v/s +21.2% in 3QFY17), with a

market share of 12.6% in Feb-17.

GoAir’s domestic RPKs grew +26.7% YoY (adj.) (v/s +18.7% in 3QFY17), with a

market share of 8.3% in Feb-17.

Jet’s RPK growth stood at +8% YoY (adj.), followed by Air India at +5.9% YoY

(adj.).

IndiGo’s passenger market share remains highest at ~40% in Feb-17

Passenger market share (%)

Jan-17

IndiGo

Jet

AI

SpiceJet

GoAir

Others

18.0

18.3

13.9

13.3

12.9

13.1

8.3

8.7

7.1

7.0

Feb-17

39.9

39.7

Domestic ASKs increase +17.8% YoY (adj.) in Feb-17 (v/s +21.1% in 3QFY17)

Domestic RPKs rise +21% YoY (adj.) in Feb-17 (v/s +22.8% in 3QFY17)

Swarnendu Bhushan

(Swarnendu.Bhushan@MotilalOswal.com); +91 22 6129 1529

Abhinil Dahiwale

(Abhinil.Dahiwale@motilaloswal.com); +91 22 3980 4309

21 March 2017

1

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on

www.motilaloswal.com/Institutional-Equities,

Bloomberg, Thomson Reuters, Factset and S&P Capital.