Sector Update | 3 October 2017

Capex tracker

New project announcements decline sharply

Private sector investment proposals at 15-quarter low

We highlight key takeaways from the quarterly projects data released by Centre for

Monitoring Indian Economy (CMIE). We use this as a proxy for the Indian capex

cycle. CMIE tracks projects across stages of announcement, implementation and

completion, and takes into account stalled/shelved projects.

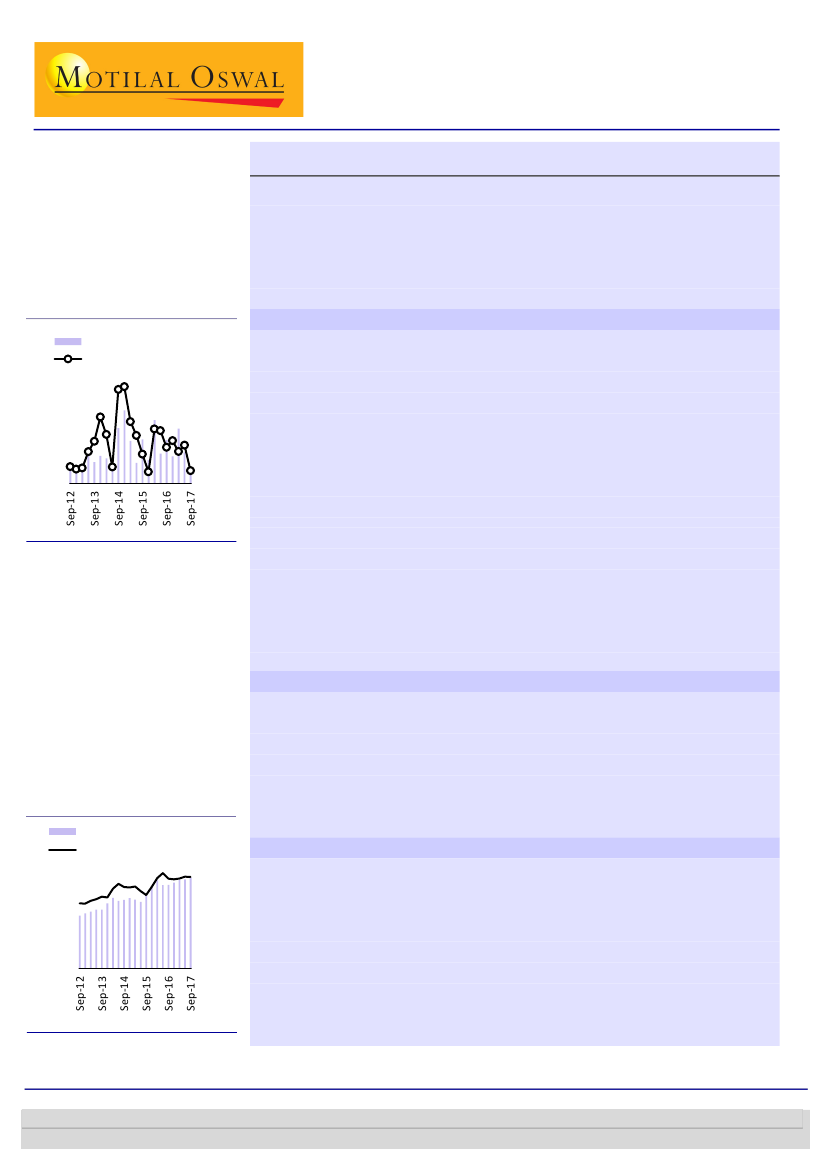

New project announcements

dip 64%

New Projects anncd INRb

Growth YoY (%)

200%

100%

0%

-100%

New project announcements dip 64% to INR845b

Intentions to set up new projects were at INR845b in 2QFY18, a dip of 64% YoY and

the lowest since June 2014, when the new Modi-led government assumed power.

Private sector investment proposals fell to their lowest in 15 quarters to INR313b

(down 83% YoY) and accounted for 37% of total new project proposals. The share of

government proposals was at 63% and stood at INR532b (down 9% YoY) – of this,

the share of state governments was 44%. State government investment proposals

stood at INR367b (up 68% YoY), primarily driven by the proposed INR200b Taj

International Airport project in Greater Noida. Uttar Pradesh accounts for 24% of

the new investment proposals during the quarter.

Our interactions with companies indicate that post GST implementation from July

01, 2017, government ordering has slowed, as the new GST rates are getting

integrated into new and existing contracts. Government orders should improve in

the coming quarters, as this impact fades. A sectoral analysis of proposals during the

quarter indicates steep declines in Electricity (-73% YoY; INR60b), Transport (-51%

YoY; INR328b) and Manufacturing (-76% YoY; INR303b).

6,000

4,000

2,000

0

Project completions slump 77% YoY to INR512b

During the quarter, project completions slumped 77% YoY to INR512b – this is much

lower than the average run rate of INR1t, and in fact, the lowest in three years.

Renegotiation of contracts post GST implementation from July 2017 could explain

part of this slow pace of execution. The slowdown seen in 2QFY18 comes after a

revival in completions over FY15-17 even in a period when project announcements

were subdued.

Stalled projects remain at elevated

levels (13.3% of the projects)

Stalled projects INRb

% of under implementation

15.0%

15000

10000

5000

0

10.0%

5.0%

0.0%

Stalled projects rise to INR13.2t, 13.3% of projects under implementation

Projects stalled remain elevated at INR13.2t, 13.3% of projects under

implementation. 40% of the stalled projects (INR5t) are due to lack of

environmental clearances (14%), lack of fuel (13%), or lack of funds (10.3%). Land

acquisition related problems account for another 9% of stalled projects. 67% of the

total stalled projects are private sector projects. Power projects, which constitute

39% of stalled projects, continue to dominate stalled projects. Other key sectors

with a high share of stalled projects are: Manufacturing (23%), Services (21%), and

Construc tion (10%). One of the key reasons for subdued new project

proposals/announcements is the high stalled projects.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

8 August 2016

1

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Ankur Sharma

(Ankur.VSharma@MotilalOswal.com); +91 22 3982 5449

Amit Shah

(Amit.Shah@MotilalOswal.com); +91 22 3029 5126