3 May 2021

4QFY21 Results Update | Sector: Technology

L&T Technology

Estimate change

TP change

Rating change

Bloomberg

Equity Shares (m)

M.Cap.(INRb)/(USDb)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

12M Avg Val (INR M)

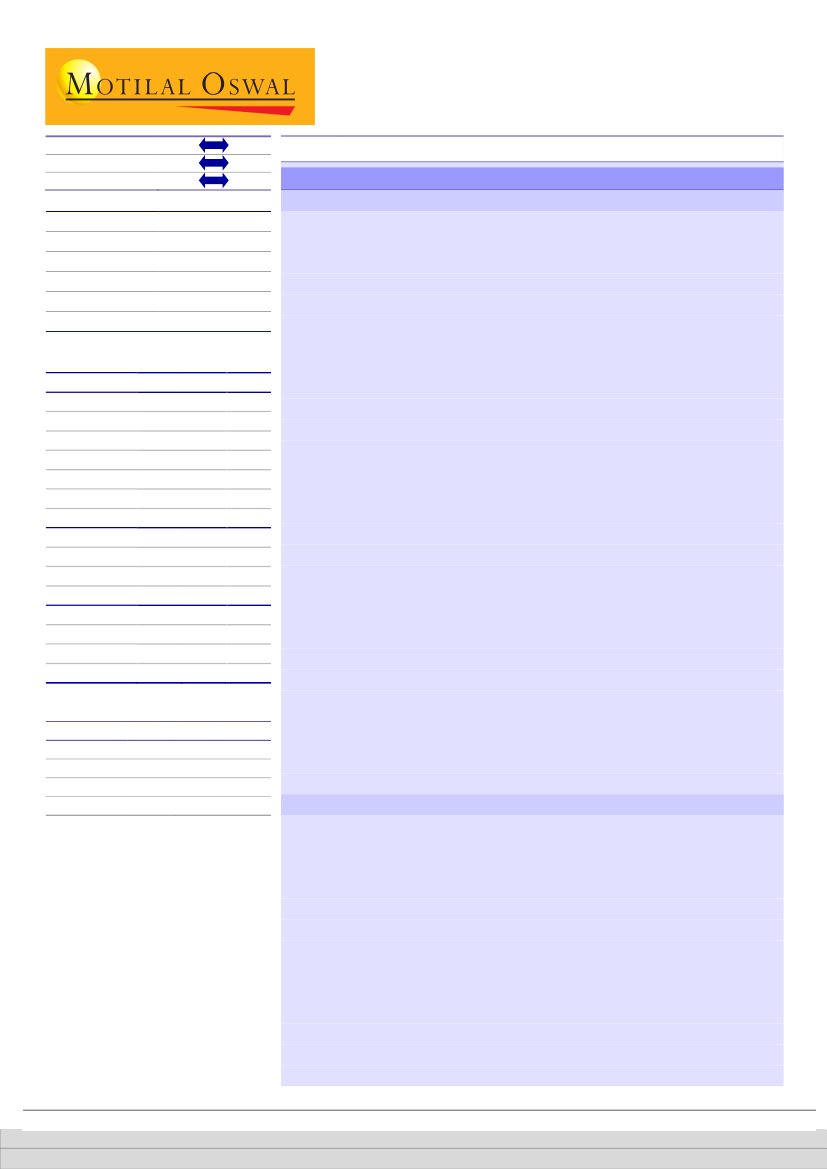

Financials & Valuations (INR b)

Y/E Mar

2021 2022E

Sales

EBIT Margin (%)

PAT

EPS (INR)

EPS Gr. (%)

BV/Sh. (INR)

Ratios

RoE (%)

RoCE (%)

Payout (%)

Valuations

P/E (x)

P/BV (x)

EV/EBITDA (x)

Div Yield (%)

44.5

8.4

27.3

0.8

33.1

7.3

20.5

0.9

26.8

6.2

16.2

1.1

21.2

16.2

35.0

23.7

18.5

30.0

25.0

19.7

30.0

54.5

14.5

6.6

62.8

(19.0)

330.8

63.5

16.7

8.9

84.4

34.4

385.1

CMP: INR2,797

TP:INR 3,130 (+12%)

Upward revisions likely on the guidance front

LTTS IN

106

293.8 / 4

3062 / 1066

5/50/82

532

Buy

Improving demand outlook and long growth trajectory are key drivers

LTTS reported 3.8% QoQ CC growth in 4QFY21, missing our estimate by

150bp. While segments like Plant Engineering (+9.9% QoQ, large deal ramp

up) and Transportation (+6.6% QoQ) did well, Telecom and Hi-Tech and

Medical Devices were flat QoQ. EBIT margin improved 140bp QoQ,

benefiting from better utilization and offshore mix.

The company continues to do well on the deal front, adding six large deals

(over USD10m), with two deals with a TCV of over USD25m. The

management expressed its confidence on the deal pipeline, which has a

good mix of smaller and larger deals, helped by a return to normal decision

making cycle in the US and Europe.

LTTS provided an initial FY22 USD revenue growth guidance of 13-15%. The

management attributing the modest guidance to their increased caution due

to the recent COVID-19 cases in India. While we are disappointed by the

guidance (our initial estimate was of mid-to-high teens), we see meaningful

scope for an upward revision as we progress through the fiscal.

With strong demand commentary across industries and key regions, and

capability to deliver services during the lockdown, LTTS should not see

meaningful disruption in the business. We bake in 17.5% revenue growth for

FY22E, partially on account of a favorable base.

We expect margin to remain rangebound from current levels in FY22 as the

wage hike and investments should offset a gradual improvement in

operating metrics. Given the low base of FY21, we factor in a 310bp EBIT

margin improvement over FY21-23E.

We see LTTS as a key beneficiary of growing tech adoption in ER&D, which

should grow by ~2x that of IT Services over FY18-23E. Moreover, with Digital

at 50% of revenue, it should also benefit from 18% growth in Digital ER&D

spends over this period. We have built in 17%/29% revenue/EBIT CAGR over

FY21-23E. We value the stock at 30x FY23E EPS.

Maintain BUY.

Revenue miss but margin in line; FY22 initial guidance below our estimate

In USD terms, revenue grew 1% YoY (v/s our estimate of 2.7%), operating

profit grew 9.3% (v/s our expectation of 10.6%), and PAT fell 5% (v/s our

expectation of being flat) in 4QFY21. The same declined 6.2%/15%/19% YoY

in FY21.

Revenue rose 3.9% QoQ (v/s our estimate of 5.6%) to USD197.5m in

4QFY21. In constant currency, the same was up 3.8% QoQ, but flat YoY.

During 4QFY21, LTTS won six deals with a TCV of over USD10m, which

includes two deals of over USD25m.

Revenue from Digital and leading-edge technologies stood at 52% in

4QFY21.

The management guided at USD revenue growth of 13-15% in FY22.

EBIT margin improved 140bp QoQ to 16.6% (in line) in 4QFY21 despite an

80bp increase in SGA expenses.

2023E

75.2

17.6

11.0

104.3

23.5

452.2

Shareholding pattern (%)

As On

Promoter

DII

FII

Others

Mar-21 Dec-20 Mar-20

74.2

74.3

74.6

6.4

6.4

4.9

9.1

8.9

8.4

10.3

10.5

12.1

FII Includes depository receipts

Mukul Garg– Research analyst

(Mukul.Garg@MotilalOswal.com)

Research analyst: Anmol Garg

(Anmol.Garg @MotilalOswal.com) /Heenal

Gada

(Heenal.Gada@MotilalOswal.com)

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.