SECTOR: MEDIA

TV Today Network

STOCK INFO.

BLOOMBERG

BSE Sensex:20957.81

S&P CNX: 6241.10

TVTN@IN

REUTERS CODE

6 December 2013

Initiating Coverage

(Rs CRORES)

Buy

Rs118

TVTO.BO

Y/E MARCH

FY13

FY14E

FY15E

We recommend to BUY TV Today Network with one year price

target of

Rs

175 at 15xFY14E earnings.

TV Today Network runs four news channels namely AajTak,Headlines

Today,Tez and Dilli AajTak.

Digitisation, a windfall gains for broadcasters:

Broadcasters are

likely to enjoy windfall gains as digital cable opens up the under declared

pay-TV revenues. Digitisation will also ensure increase in cable

capacity, which will lead to reduction in carriage cost paid by

broadcasters to erstwhile analog cable oparators. The power of

bargaining will shift from distribution networks to content. In such a

scenario, we believe broadcasting networks will grow their profit at

CAGR of 35-40% during FY13-FY17 just because of increase in

subscription revenue, which will flow entirely to bottom line. Please

look at Table 1 and Table 2 for schedule of digitization and growth in

subscription revenue.

News Content's double whammy:

News channels suffer double

whammy as they need to pay high carriage fee on top of low

subscription income as compared to General Entertainment Channels

(GECs) to get their channels carried on analog networks. Carriage

fee is the single largest cost item in P&L of news channels at ~30-

35% of revenues. This has lead to financial bleeding of almost all

news channels. Two of the three listed players are barely profitable

and one is loss making for a long period of time. Digitisation will

reduce the carriage fee, which will ensure better financial performance

from news broadcasters.

TV Today Network, a turnaround:

Surge in revenues with not

much increase in associated cost will ensure a huge turnaround in

operational performance of the company. The company will likely report

life high profit at the end of FY14, which will also ensure RoE of

~20%. We expect revenues to grow at CAGR of 23% during FY13-

15E vs 10% growth during FY06-13. This will lead to disproportionate

growth in PAT at CAGR of 171% during FY13-15E vs PAT CAGR of

-11% during FY06-13.

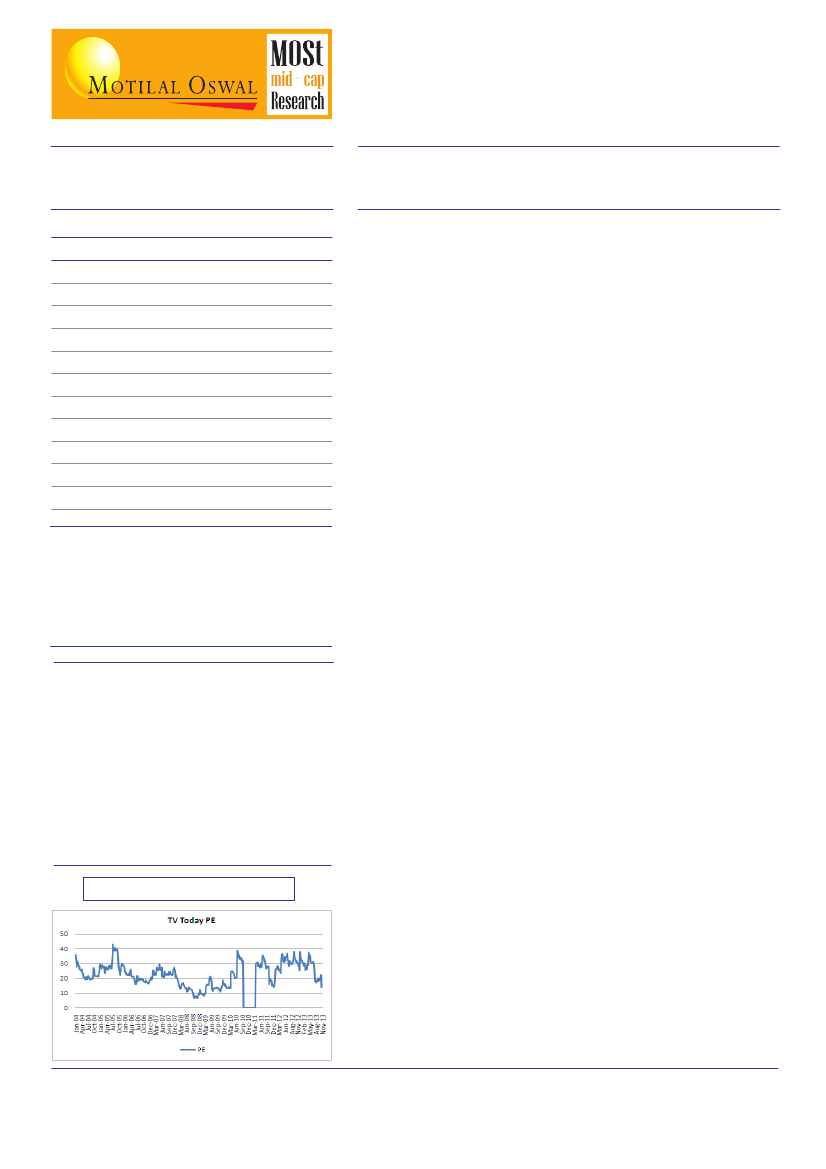

Valuations and View:TV

Today is play on turnaround of news

broadcasting business as well as general theme of digitization in media

space. The stock offers attractive risk reward at ~10x FY14E EPS

with ~4% dividend yield in FY14E. Historically, the company has traded

at median PE of 21x and lowest PE of 9x since listing in FY04.

Therefore, we believe there is a decent upside to stock in 1 year time

frame even if we take 30% discount to median valuations. Recommend

BUY with target price of Rs 175 in 12 months time (15x FY14E, 30%

discount to median valuations).

Sales

EBITDA

PAT

BV/Share (Rs.)

EPS (Rs.)

EPS growth (%)

P/E (x)

P/BV (x)

EV/EBITDA (x)

Div yld (x)

ROE (%)

313

42

12

55

2

15%

58

2.2

16.6

0.6%

4%

415

135

69

65

12

476%

10

1.8

4.5

4.2%

19%

477

164

88

74

15

27%

8

1.6

3.3

5.9%

21%

KEY FINANCIALS

Shares Outstanding (Cr.)

Market Cap. (Rs Cr.)

Market Cap. (US$ m)

Sales CAGR 3 Yrs to FY13E

PAT CAGR 3 Yrs to FY13E

5.95

702

115

12%

77%

STOCK DATA

52-W High/Low Range (Rs)

Major Shareholders (as of Dec 2010)

Promoter

Domestic Inst & Govt.

Foreign

Public & Others

Average Daily Turnover(6 months)

Volume

Value (Rs million)

1/6/12 Month Rel. Performance (%)

1/6/12 Month Abs. Performance (%)

175170

1.61

39/51/28

38/52/34

124/53

58%

4%

0%

39%

Maximum Buy Price :

Rs

Rs120

Rakesh Tarway

(rakesh.tarway@MotilalOswal.com); Tel: +91 22 30896679