Sector Update | 17 June 2015

Financials

Please refer to our recent

thematic on liability

profile of Indian Banks

Deep dive into ARC business

Banks are ready, but resources at ARCs a key constraint

ARCs play a crucial role in the financial sector and help banks clean up stress loans.

After a prolonged lull (2008-13), asset sales surged by >3x YoY in FY14—helped by RBI

guideline of amortizing loss on sale to ARCs over an eight-quarter period.

Aggressive sales (higher MTM losses on security receipts in future) and ARCs’ agency

model approach (focus on management fees rather than recoveries) led to tightening

of guidelines by RBI in August 2014, which (amongst other things) increased ARCs’

minimum investment from 5% to 15%. This resulted in a sharp slowdown in asset

sales; however, we recently saw large PSBs such as SBI and BOI selling NPAs at a steep

discount to book value. Considering the changed dynamics, we expect more banks to

become realistic about valuations/recoveries and steep discount sale to continue.

While enablers are in place, capital remains one of the key challenges for the ARC

industry. Our detailed analysis factoring in available capitalization and borrowed

funds suggests ~INR200b of SR issuances in FY16 (similar to FY15). Funding constraints

are likely to result in higher bargaining power for ARCs. Our interactions with industry

participants indicate a discount of ~40-60% for future transactions v/s at par to ~30%

discount prior to guideline change in August 2014.

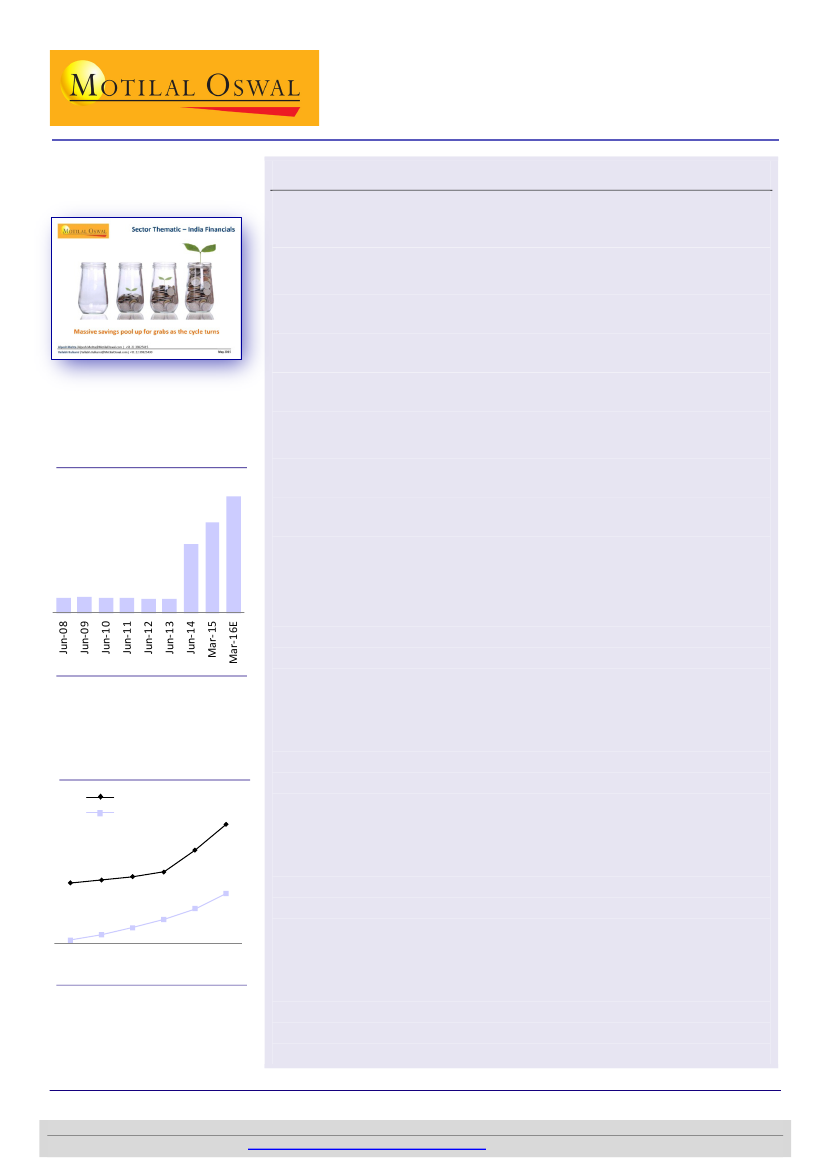

Stock of SRs have increased by

5x in last two years

SRs Outstanding (INR b)

710

550

420

94 100 95 92 85 88

Source: MOSL

Impact of new guidelines -

Business model no longer viable

on just management fees

IRR (earlier)

IRR (now)

39%

30%

25% 27% 28%

6%

10%

15%

21%

50%

1%

80

4%

70

60

50

40

30

Sale consideration paid by ARC

Source: MOSL

Banks adjusting to new reality; asset sale to drive stress loans lower:

Post

the sharp slowdown in stress asset sales, activity picked up in 1HCY15, with

the key change being banks (led by SBI) willing to take higher losses. Our

industry interactions suggest that the ARC industry has structurally moved

from agency business (focus on fees for IRR) to fund-based business (focus

on recoveries and realistic pricing for IRR). With the banks willing to sell

higher NPAs at a significant discount, headline stress loans on balance sheet

are likely to decline; however, credit costs will remain elevated due to

amortization charges arising out of losses on sale.

Capital remains a key challenge for the ARC industry:

Net worth of ARC

industry is INR30b and capital employed is INR60b. While the industry can

effectively have leverage of 6.7x+ (15% CAR, assuming entire as Tier I),

uneven cash flows remain a key constraint for debt servicing. Other

structural problems—(a) low-debt philosophy adopted by ARCIL (50% of

industry net worth), (b) 49% sponsor shareholding cap, and (c) largely

retail/SME/MSME-focused ARCs—have lowered capital availability for

acquiring large/mid corporate loans. Our estimates suggest that a rupee

invested in an ARC can help banks clean INR85 of stress loans (Exhibit 15).

Key enablers for growth:

In FY16, banks (especially PSBs) are widely

expected to use the extended RBI dispensation of amortization of losses on

sale of assets to ARCs. Increasing the dispensation for banks beyond 31-

Mar-16, removing the 49% cap on sponsor shareholding, strengthening the

judicial system and sale of lower-vintage accounts at a reasonable price

(better recovery incentives) are a few triggers for higher asset sales.

Alpesh Mehta

(Alpesh.Mehta@MotilalOswal.com); +91 22 3982 5415

Vallabh Kulkarni

(Vallabh.Kulkarni@MotilalOswal.com); +91 22 3982 5430

Investors are advised to refer through disclosures made at the end of the Research Report.

Motilal Oswal research is available on

www.motilaloswal.com/Institutional-Equities,

Bloomberg, Thomson Reuters, Factset and S&P Capital.