Tata Motors

BSE SENSEX

35,322

S&P CNX

10,736

31 May 2018

Update

| Sector:

Automobiles

CMP: INR283

TP: INR471(+66%)

Stress Test: How low can the stock price go?

Liquidation value at ~INR256/share; favorable risk-reward at CMP

Buy

Stock Info

Bloomberg

Equity Shares (m)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

M.Cap. (INR b)

M.Cap. (USD b)

Avg Val, INRm

Free float (%)

TTMT IN

2,887

486 / 282

-17/-37/-54

903.1

14.4

3731.0

63.6

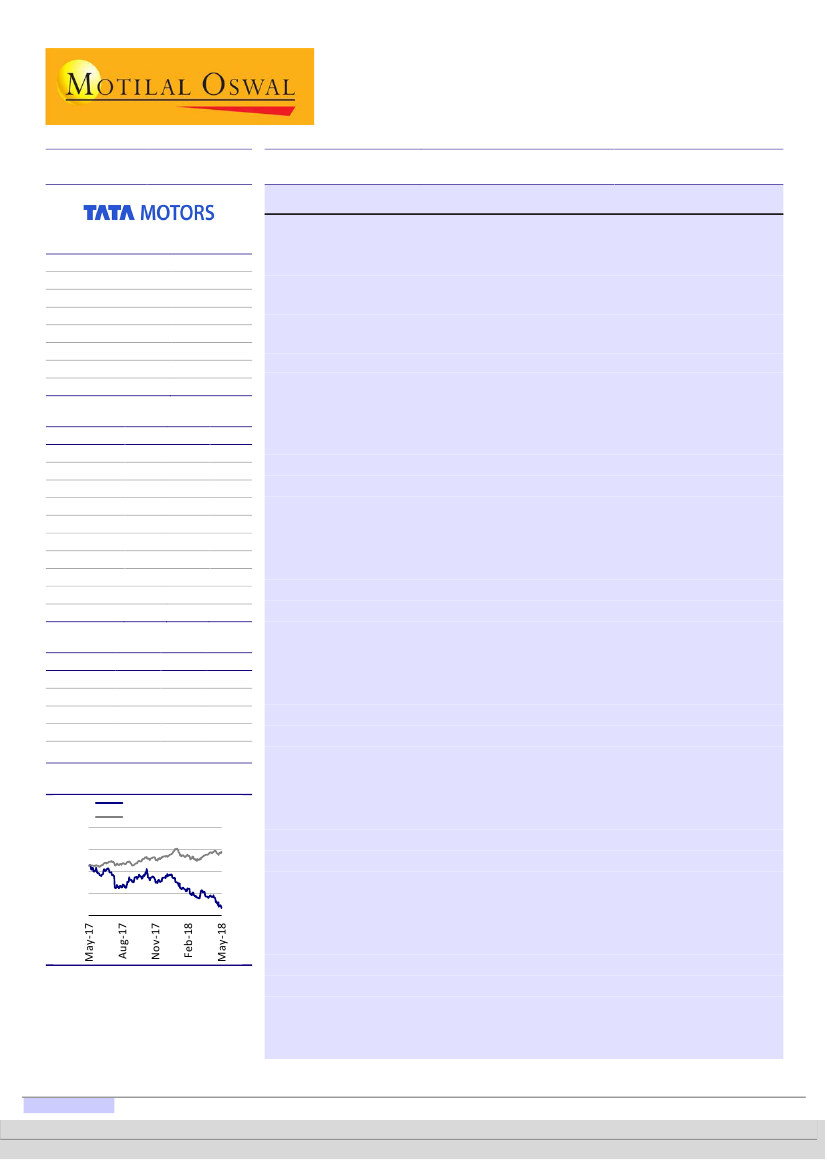

Tata Motors’ (TTMT) stock price has been under pressure, particularly since the beginning

of 2018, on account of concerns about the demand environment, the adverse GBP

movement, the noise on trade wars, etc. In CY18 YTD, TTMT’s share price has declined

~34%, as against a 7.8% decline in the BSE Auto Index and around 2.9% upmove in the

Nifty 50. In this note, we evaluate the worst-case scenario liquidation value for TTMT and

more realistic-case downside from current levels. We also highlight the potential triggers

– both positive and negative – that need to be closely watched.

Financials Snapshot (INR b)

Y/E Mar

2018 2019E 2020E

2,946 3,386 3,738

Net Sales

369.7 468.2 537.0

EBITDA

NP

77.8 146.6 179.6

Adj. EPS (INR)

22.9

43.2

52.9

15.7

88.3

22.6

EPS Gr. (%)

281.0 325.4 379.6

BV/Sh. (INR)

RoE (%)

10.1

14.2

15.0

RoCE (%)

6.4

7.4

8.1

12.3

6.6

5.3

P/E (x)

1.0

0.9

0.7

P/BV (x)

Shareholding pattern (%)

As On

Mar-18 Dec-17 Mar-17

Promoter

36.4

36.4

34.7

DII

17.7

17.1

15.5

FII

20.3

21.4

23.2

Others

25.7

25.1

26.6

FII Includes depository receipts

Stock Performance (1-year)

Tata Motors

Sensex - Rebased

650

550

450

350

250

We assess liquidation value at ~INR256/share or ~10% downside from current

level. This is after considering the intangible assets of JLR and India business at

35% of book value (based on 35% capitalization rate v/s JLR’s 80%). While

stocks have traded below their liquidation values in the past, barring any global

macro events, we do not see TTMT sustaining at such levels for a long time.

At ~INR256/share, TTMT would be valued at ~0.9x FY18 P/B, which is close to

its floor P/B valuation of 0.9x in the last 10 years.

Interestingly, even during the Global Financial Crisis (GFC) and worst financials

ever for JLR (EBIT margin of -6.5% in FY09), similar health of India financials

(EBITDA margins at 6.7% in FY09) and negative CFO, the bottom valuation for

TTMT was at 0.9x in 3QFY09.

Coincidentally, JLR’s peers BMW (0.98x) and Daimler's (0.76x) bottom

valuations are also around ~0.87x P/B (ex GFC).

We see the following drivers for the operating performance over 1-2 years:

Demand recovery for JLR, as base normalizes and full benefit of new

launches reflect in FY19.

Continued moderation in realized FX hedge losses in 1HFY19 and FX

starting to contribute positively from 2HFY19.

Lower-cost Slovakia plant supporting profitability.

Apart from above-mentioned visible triggers, the success in the following areas

can act as a re-rating trigger for the stock:

Strong response to its first BEV Jaguar I-Pace.

Efficiency and cost-cutting initiatives at JLR enabling achievement of the

EBIT margin target of 7-9% in the long term.

Strong response in China to locally made Jaguar XE and E-Pace.

Improving competitive positioning in both CV and PV businesses.

Break-even in PV business.

Monetization of non-core assets.

At current price, we see a very favourable risk-reward scenario for TTMT, with

worst-case downside of ~13% and base case upside of ~66%. Key risks to our

thesis: a) persistent weakness in demand environment for JLR, b) trade barriers

impacting competitive positioning of JLR and c) adverse FX movement.

Jinesh Gandhi - Research analyst

(Jinesh@MotilalOswal.com); +91 22 6129 1524

Research analyst: Deep Shah

(Deep.S@MotilalOswal.com); +91 22 61291533/

Suneeta Kamath

(Suneeta.Kamath@MotilalOswal.com); +91 22 61291534

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.