23 June 2020

India Strategy

BSE Sensex: 35,430

Motilal Oswal values your support in

the Asiamoney Brokers Poll 2020 for

India Research, Sales and Trading

team. We

request your ballot.

S&P CNX: 10,471

Indo-China Conflict: A look at sectoral inter-linkages with China

Pharma, Auto, Consumer Durables, Telecom Equipment most exposed

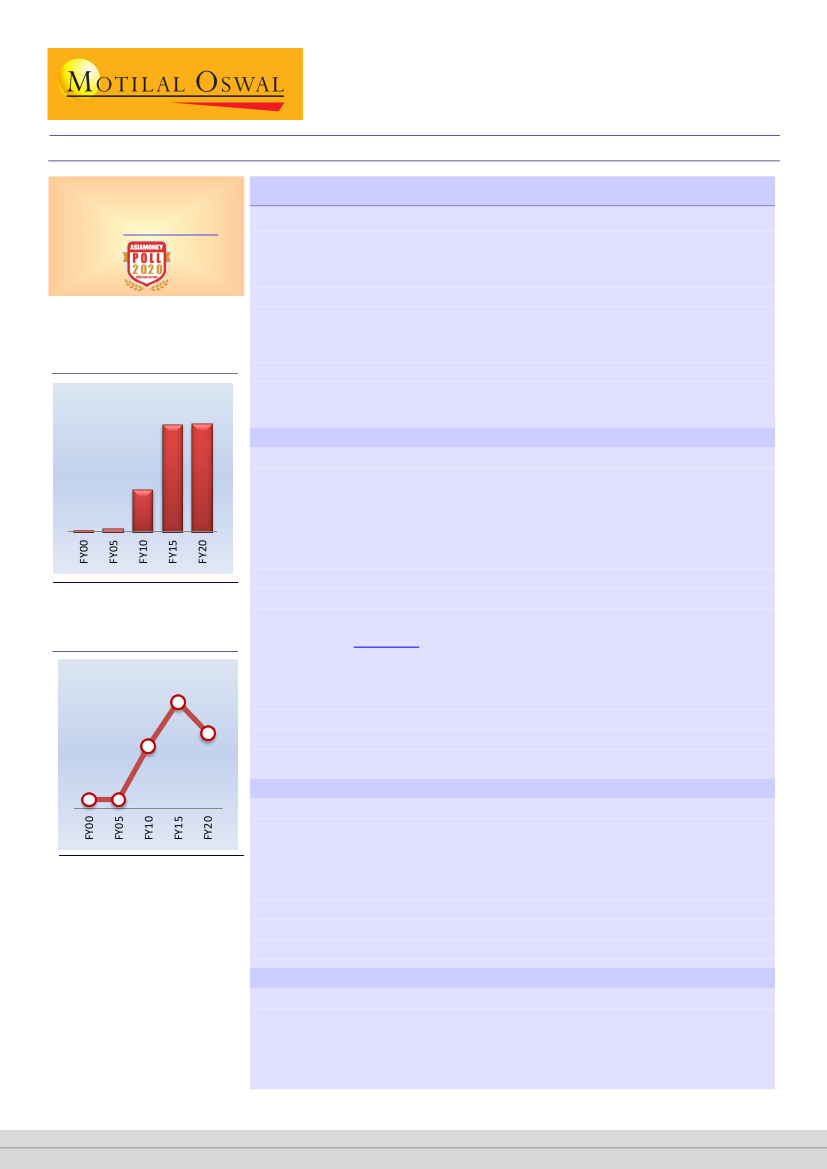

Trade Deficit with China (USD b)

48.5 48.6

The recent border conflict with China in the Galwan valley of Ladakh is

unprecedented and has heightened geopolitical tensions. This has caused significant

backlash in India.

Further, the narrative of reducing trade dependence on China is gaining steam.

In this report, we look at key India-China macro trade metrics and highlight sector-

wise exposure to China on imports, supply-chains and raw materials.

India's trade deficit with China has doubled in the last decade. From sectoral

perspective, Pharma, Consumer Durable, Telecom Equipment and Automobiles will

be relatively more impacted along with a spill-over to stringent trade policy

actions/retaliations if the India-China conflict escalates further.

Unprecedented geopolitical flare-up in Indo-China relations

19.2

0.8 1.5

Trade Deficit with China (% of

GDP)

2.4

1.7

1.4

0.2 0.2

The recent (15-16

th

Jun’20) flare-up on the Indo-China border in the Galwan Valley

of Ladakh is unprecedented. It has heightened geopolitical tensions between the

two nations leading to reports of potential escalation. The situation is currently

fluid with diplomatic and political emphasis on disengagement and a desired return

to normalcy at the earliest. However, these events have caused significant backlash

in India, giving rise to a narrative of reducing dependence on China – both on

business and commercial fronts. Media reports suggest that the Government of

India has asked the industry to prepare a list of products imported from China; this

would help identify non-essential imports for which local substitutes could then be

made available (Refer

here).

Further, business contracts awarded to Chinese firms

have been cancelled by some state governments (Maharashtra and Haryana). While

we would not like to hypothesize on the possible future steps being contemplated,

in this note we look at key macro trade parameters between India and China and

the inter-linkages of different sectors with China in terms of sales, supply chains as

well as investments. Moreover, we have also highlighted sectors and companies,

which would get impacted in case of import curbs or tariffs.

Snapshot of key macro trade metrics between India-China

From barely any deficit in FY00, India ran a trade deficit of USD48.6b (1.7% of GDP)

with China in FY20. India’s imports from China have risen steeply from just 2.6% of

total imports in FY00 to an all-time high of 16.4% in FY18 before easing to 14%

(USD65.3b) in FY20. India’s exports to China, as a percent of total exports, have just

started picking up pace after touching 3.4% in FY16. In FY20, it stood at USD16.6b

or 5.3% of total exports from India. Finally, as per official data from the Department

of Industrial Policy and Promotion (DIPP), China’s FDI inflow over FY00-20 to India

stood at a mere USD2.4b out of India’s total FDI inflow of USD470.1b.

Several sectors have material linkages with China

From a sectoral perspective Auto, Consumer Durables, Pharmaceuticals, Telecom,

Chemicals and Renewable Power sector (Solar) seem to be the most dependent in

terms of sourcing from China. Also, in many cases there appears to be a lack of

alternative suppliers at the same scale or costs. While Consumer Durables is

dependent on China for components, Pharma is dependent for API sourcing.

Research Analyst: Gautam Duggad

(Gautam.Duggad@MotilalOswal.com); +91 22 6129 1522;

Nikhil Gupta

(Nikhil.Gupta@MotilalOswal.com); +91 22 6129 1555

May 2020

Yaswi Agarwal

(Yaswi.Agarwal@motilaloswal.com); +91 22 7193 4196;

Jayant Parasramka

(Jayant.Parasramka@motilaloswal.com)

1

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

Investors are advised to refer through important disclosures made at the last page of the Research Report.