WEEK IN A NUTSHELL

WIN-dow to the week that was

Week In a Nutshell (WIN).

Week

ended

9 Sep

Key WIN-dicators

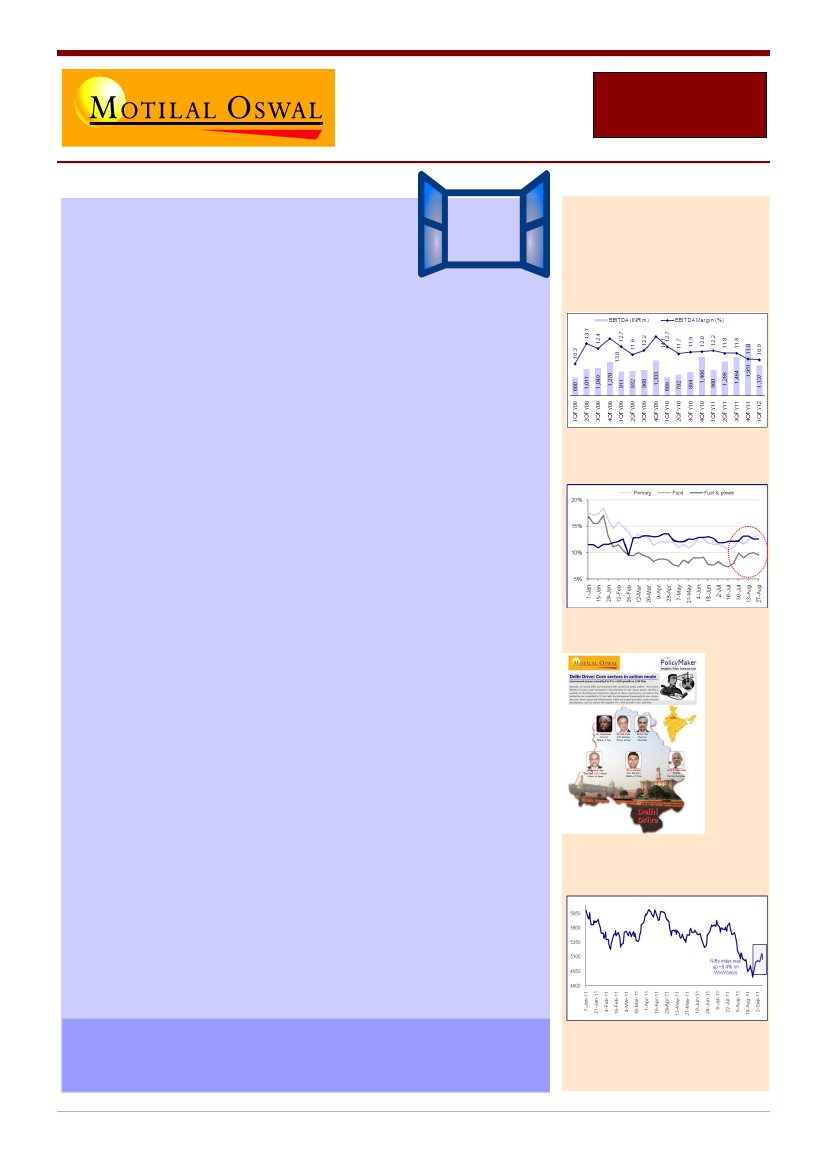

THERMAX – Margins seeing structural

change?

Markets for the week were flat with all the hard work through the

week (gain of 2%) lost on the last trading day. While one of the calmest

week in terms of news flow for some time, the highlight being the

outlining of the 447 USD Bn JOBS PLAN by President Barack Obama. If

one has to play contrarian, this is the first of the last 3 packages which

has not been received with a bug HURRAH – So can it work??

TELECOM –

The sector just does not go out of news. This time there was

an exchange of volleys - Mr. Sunil Mittal leading with an announcement

of a definite increase in tariffs in the future to make up for lower

revenues. TRAI responded with indication of intervention if tariffs keep

going up. Mr. Himanshu of Idea reiterated that publicity around tariff

hikes is overdone and long term growth will depend on data.

LABOUR TROUBLE –

Maruti continues to have problems at Manesar and

it does not seem to be a short term one. It couldn’t have been more ill-

timed considering success of their New Swift. The company is having to

juggle around employees from one factory to another and also in cases

move some lines to Gurgaon. One or a combination of the following are

at play – Political motive, Maruti losing the upper hand in bargaining

with prosperity of the auto belt, and lastly, loose labour laws in India.

We were lucky to have a services boom and skip industrial progression. If

we now need a manufacturing boom, we need stronger labour laws.

Maharashtra increased daily wages

from INR 127/day to INR 200/day

resulting in increased outlay of INR 50 Bn. This compares with spending

of less than INR 3.5 Bn over the last 3 years. Wonder why!!!

PRIMARY INFLATION – Not letting up

Delhi – Policy Drive, Must Read

Some of the highlights of this edition

Policymaker Series – Meeting Notes with various ministries

Union Bank of India management meet takeaways

Indonesia and India Power plants

WoW - Nifty Change (+0.4%)

Happy Reading and Have a GREAT WEEKEND!!

WWW – WIN Weekend Wisdom

Investing probably is not played best as a group sport

WIN – Week In a Nutshell

1

9 Sep

2011