12 October 2011

2QFY12 Results Update | Sector: Technology

Infosys Technologies

BSE SENSEX

S&P CNX

16,958

Bloomberg

Equity Shares (m)

52-Week Range (INR)

1,6,12 Rel. Perf. (%)

M.Cap. (INR b)

M.Cap. (USD b)

5,099

INFO IN

571.2

3,494/2,169

19/-5/4

1,531.0

31.3

CMP: INR2,681

TP: INR3,170

Buy

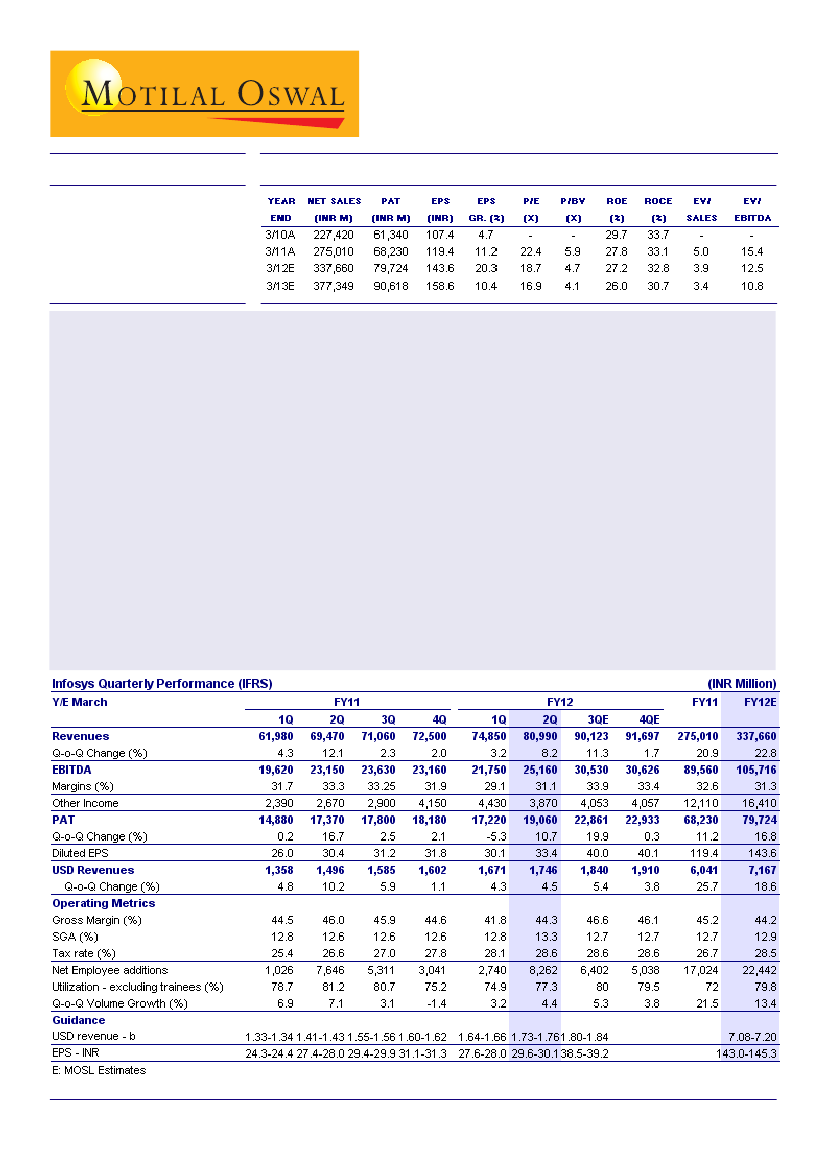

Infosys Technologies (INFO) posted strong volume growth in 2QFY12 (4.4% QoQ against our expectation of 3.7%)

with no cut in volume or pricing assumptions in its FY12 USD revenue growth guidance (17.1-19.1% v/s 18-20%

earlier, the change being driven by cross currency fluctuations). This lays to rest concerns over volume growth for the

year - a positive surprise for the street.

Change in the company's rupee EPS guidance (INR143.02-145.26 v/s INR128.2-130.1 earlier, 11.6% increase at the

upper end) was driven by a weaker rupee assumption of INR49 to the US dollar. We keep our USD revenue growth

estimates unchanged and factor in an average rupee/US dollar exchange rate of INR47.1 (v/s INR45 earlier) for FY12

and INR46 (v/s INR45 earlier) for FY13. Our revised EPS estimates are INR143.6 (v/s INR133.7 earlier) and INR158.6

(v/s INR152.5 earlier) for FY12 and FY13 respectively. 1% change in INR/USD impacts our EPS by 1.6%.

Change in currency assumptions in favor of a weaker rupee across the street is likely to make the stock/stocks in

the sector more susceptible to currency volatility.

Our core thesis remains intact: (i) Post restructuring INFO will be able to operate at higher utilization (78-82%, ex-

trainees), which was reiterated by the management. INFO's current utilization (ex-trainees) is 77.3%, leaving room

for a 470bp increase. (ii) INFO can maintain pricing with a focus on higher value businesses like consulting/PI and

products/platforms. Realization in 2QFY12 was up 100bp (constant currency). (iii) Narrowing differential in growth

rates v/s TCS will be visible over the next two quarters. INFO grew its telecom vertical after three successive quarters

of declines (excluding revenue declines from a large telco client, INFO's growth is not very different from TCS).

Reiterate

Buy

with a target price of INR3,170 (v/s INR3,050 earlier) implying an 18% upside.

Nitin Padmanabhan

(Nitin.Padmanabhan@MotilalOswal.com); Tel: +91 22 3982 5426

Ashish Chopra

(Ashish.Chopra@MotilalOswal.com); Tel: 3982 5424