WEEK IN A NUTSHELL

WIN-dow to the week that was

Week In a Nutshell (WIN).

Week

ended

st

21 Oct

Key WIN-dicators

The HEAVY Season Starts. Volatile Week with a sea of results,

most being inline apart from a few disappointments. Maruti

STRIKE called off is a big relief to all the industry watchers. This

week saw the FM finally admit that both 8% growth and the

fiscal deficit will be a challenge to hold on to. While market has

factored this long ago, as they say cognizance of a problem is the

first step towards resolving the same. Primary article inflation

spike is not a convenient backdrop for upcoming RBI policy (25

th

)

THE GOOD:

Private banks put up an extremely good show in

terms of results – Restraint in Corporate Credit, Aggression in

Consumer Loans, Controlling Opex and measured expansion. NPAs

have not shown up here (yet?) and hence low credit cost

cushioning during low growth periods.

THE BAD:

L&T facing considerable headwinds – Slowdown in

order intake, margins pressure and competition. While things can

get worse, we should not forget that they are the best

executioners in India. HCL Tech disappointed on volume growth

inspite of a repeated focused strategy on the same. TCS caught up

with itself – Inline numbers and stock down 10%! Initial signals

from Asian Paints point towards input cost pressure and volume

growth challenge

THE UGLY:

NHB comes out with customer friendly but draconian

regulations in terms of modus and time of implementation. To

bridge the gap between Old and New customers’ floating rates

can be herculean and extremely profit dilutive. WILL THE MIGHTY

FALL? Crompton gives us GRIEF again. The sense of operating de-

leverage truly seen here. Tough to call any stop here with almost

complete loss of faith.

Some of the highlights of this edition

Metals: RoIC Vs RoCE – Brilliant Report - Summary

The Unspoken Battle – PERNOD Vs UNSP

Summary of all important results

Happy Reading and Have a GREAT WEEKEND!!

WISHING YOU HAPPY AND PROSPEROUS DIWALI

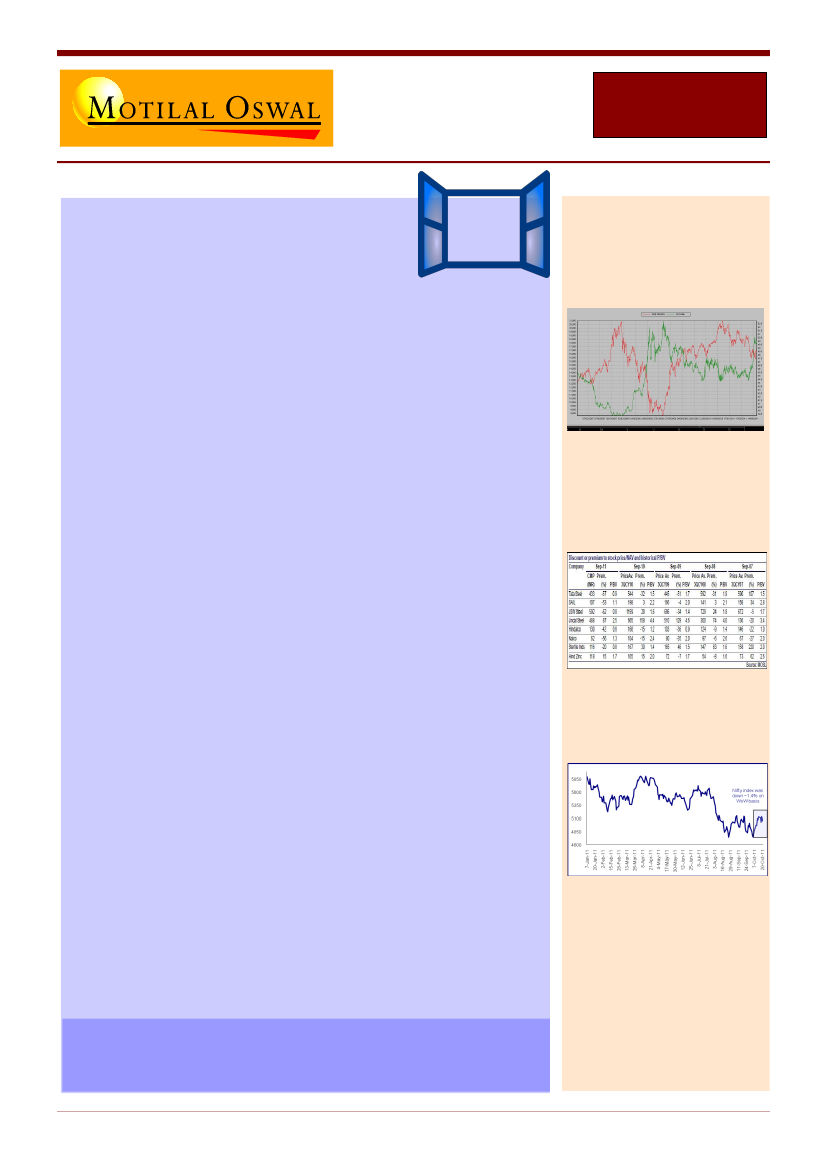

DXY and SENSEX – FALL TO COME

METALS – MUST READ REPORT

WoW - Nifty Change (-1.4%)

WWW – WIN Weekend Wisdom

Investing is an act of faith. FAITH in future, capitalism and

humanity!

WIN – Week In a Nutshell

1

21 Oct

2011