Metals Weekly

8 November 2011

Metals Weekly

Valuations: Indian companies

Price

EV/EBITDA P/BV

(INR) FY12E FY13E FY12E

Steel

Tata Steel

SAIL

JSW Steel

JSPL

Sesa Goa

Non-ferrous

Sterlite Inds.

HZL

Nalco

Hindalco

468

111

711

577

211

5.6

7.7

7.2

9.7

6.2

4.5

7.5

5.7

8.7

6.1

1.5

1.1

0.9

3.0

1.1

Metal Prices

CMP

7-NOV

HRC Tube grade - Mumbai (INR/ton)3 7 , 1 7 1

HRC (USD/ton) fob CIS

653

HRC (USD/ton) fob China

668

Sponge iron - Raipur (INR/ton)

23,800

Pig iron - Raipur (INR/ton)

24,751

Iron ore spot (USD/ton) cfr China

133

Coke (USD/ton) fob

390

Shred. scrap (USD/ton) fob Rotterdam 3 9 8

LME inventories (‘000 ton)

3m LME (USD/ton)

Indian prices (INR ‘000/ton)

LME inventories (‘000 ton)

3m LME (USD/ton)

Indian prices (INR ‘000/ton)

LME inventories (‘000 ton)

3m LME (USD/ton)

Indian prices (INR ‘000/ton)

4,546

2,140

104

763

1,952

94

415

7,825

386

%

-1

4

0

0

0

1

-3

-2

0

-5

-4

-3

-2

1

-2

-1

-3

3

-1

1

0

0

-8

Week

31-OCT

Quarter

% 1-OCT

YTD CY11

% 1-JAN

9 33,998

3

635

-9

736

2 3 19,400

1 7 21,124

-25

176

0

390

-2

406

6

-13

-6

9

-15

-14

12

-16

-12

4,277

2,470

110

699

2,308

109

371

9,346

439

37,625

- 2 38,078

628

-9

718

6 6 9 -10

738

23,800

8 22,000

24,751

1 24,479

1 3 2 -26

179

4 0 0 -10

435

404

-8

434

4,547

2,242

108

783

1,985

93

0

-1

-4

-7

5

1

4,558

2,157

108

824

1,860

93

475

6,800

340

123

123

63

139

4.3

4.7

5.7

5.5

3.4

3.8

3.3

5.1

0.9

1.9

1.3

1.4

Mid-caps

Monnet Ispat

435

Godawari

120

Sarda Energy

123

Tata Sponge

331

Adhunik Metaliks 4 3

Bhushan Steel 3 3 5

Jai Balaji

93

Rain Comm.

29

Prakash Inds.

46

13.7

3.0

9.6

2.1

5.6

8.8

7.4

2.8

2.3

9.2

3.5

6.4

1.2

4.7

8.1

7.8

2.9

1.5

1.2

0.6

0.5

0.9

0.5

1.0

1.1

0.5

0.3

4 2 3 -13

7,885 1 5

399 1 3

27,201

56,003

1,982

1.11

49.3

1,912

Note: Detailed table on pg 19

Source: MOSL

Gold (INR/10gms)

27,898

Sliver (INR/1kg)

55,625

Lead 3m LME (USD/ton)

2,010

Ferro-chrome 6-8%C60%(USD/lb Cr) 1 . 1 1

INR/USD

BDI

49.1

1,766

7 26,077

9 51,100

2

1,961

-3

1.15

0

-6

49.2

1,886

3 6 20,575

2 1 46,065

-21

2,550

-16

1.32

10

0

44.7

1,773

Valuations: Global companies

Price

Steel

A. Mittal

Posco

Nucor

Gerdau

Bao Steel

US Steel

EV/EBITDA P/BV

CY11 CY12 CY11

5.7

4.9

7.2

7.2

7.1

6.2

6.5

4.7

4.7

4.7

4.3

5.4

4.4

4.8

6.0

6.0

5.6

5.9

4.5

4.1

4.5

4.2

0.5

0.9

1.0

1.6

1.1

0.9

0.8

1.3

1.0

2.8

2.0

Source: MMR/LME/Metal Bulletin/SteelPricesIndia/MOSL

EUR 14.7

USD 27.4

USD 39.0

BRL 15.7

CNY 5.4

k KRW 378.5

Non-ferrous

Alcoa

USD 10.8

Teck Res. USD 38.9

Xstrata

BHP

Rio Tinto

GBp 10.0

AUD 37.7

AUD 68.8

Indian steel producers cut HRC prices by > USD20/ton; steel demand

still sluggish; aluminum prices down 5%

Indian steel producers have cut HRC prices by > INR1,000/ton in November.

Demand remains sluggish in a seasonally stronger second half of the financial

year.

Domestic steel prices declined 1.4% WoW for flat products and 0.5% WoW

for long products. Prices of both sponge iron and pig iron were flat WoW at

INR23,800/ton and NR24,751/ton, respectively.

Base metal prices weakened, as political uncertainty in Greece and Italy fueled

further concerns on the European debt crisis. Aluminum and copper spot

prices decl ined 5% and 3% WoW to USD2,118/ton and USD7,775/ton,

respectively. Zinc prices were up 0.2% WoW at USD1,912/ton.

Chinese spot iron ore CIF prices were up 1% WoW at USD133/ton while iron

swaps r ecovered much more sharply by 7-12% WoW.

Steel prices declined in China (down 1% WoW), Middle East (down 3% WoW),

North America (down 2% WoW) and Turkey (down 2% WoW) while prices

were flat WoW in Europe and Russia.

Demand outlook for Europe remains weak. Arcelor Mittal has recently guided

for a weaker 4QCY11 and has deferred some planned steel investments.

1

Note: Detailed table on pg 19 Source: Bloomberg

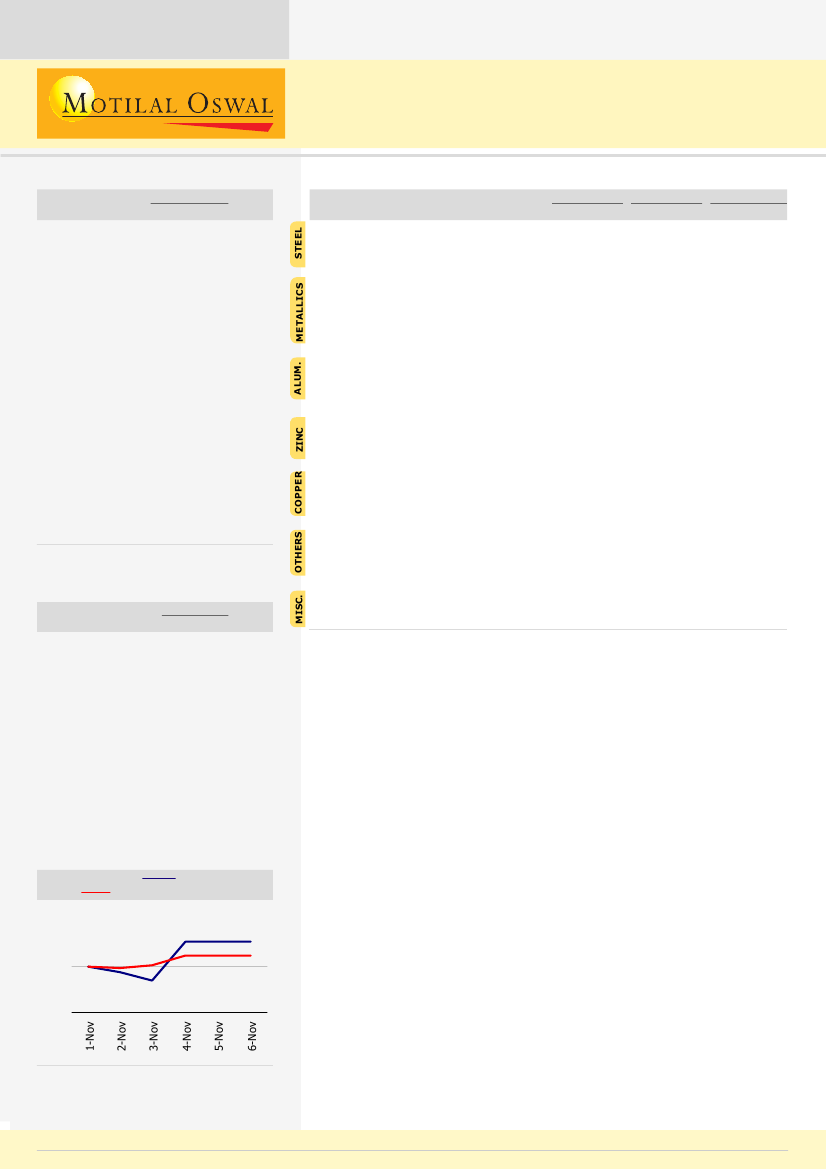

BSE Metals Index v/s Sensex

BSE Metals Index

Sensex

102

100

98

Source: Bloomberg

Note: Indexed to 100 on 1 November 2011

Individual stock performance table on pg 20

Sanjay Jain

(SanjayJain@MotilalOswal.com); Tel:+91 22 3982 5412

8 November 2011

Tushar Chaudhari

(Tushar.Chaudhari@MotilalOswal.com); Tel:+91 22 3982 5425