Metals Weekly

19 December 2011

Metals Weekly

Valuations: Indian companies

Price

EV/EBITDA P/BV

(INR) FY12E FY13E FY12E

Steel

Tata Steel

SAIL

JSW Steel

JSPL

Sesa Goa

Non-ferrous

Sterlite Inds.

HZL

Nalco

Hindalco

365

75

510

516

162

6.3

6.6

6.6

9.2

5.3

4.6

6.4

5.7

8.2

5.2

1.5

0.9

0.8

2.7

0.9

Metal Prices

CMP

19-Dec

HRC Tube grade - Mumbai (INR/ton)3 6 , 2 6 5

HRC (USD/ton) fob CIS

583

HRC (USD/ton) fob China

667

Sponge iron - Raipur (INR/ton)

22,200

Pig iron - Raipur (INR/ton)

24,660

Iron ore spot (USD/ton) cfr China

142

Coke (USD/ton) fob

370

Shred. scrap (USD/ton) fob Rotterdam 4 0 3

LME inventories (‘000 ton)

3m LME (USD/ton)

Indian prices (INR ‘000/ton)

LME inventories (‘000 ton)

3m LME (USD/ton)

Indian prices (INR ‘000/ton)

LME inventories (‘000 ton)

3m LME (USD/ton)

Indian prices (INR ‘000/ton)

Gold (Rs/10gms)

Sliver (Rs/1kg)

Lead 3m LME (USD/ton)

FC 6-8% C 60%(USD/lb Cr)

INR/USD

BDI

4,823

2,004

106

759

1,868

99

381

7,345

388

27,390

52,250

1,960

1.09

52.5

1,888

%

0

0

0

0

0

-3

0

3

5

-3

-2

0

-7

-5

0

-5

-5

-5

-6

-7

0

0

-2

Week

12-Dec

Quarter

%

1-Oct

YTD CY11

%

1-Jan

7 33,998

-8

635

-12

757

1 4 19,400

1 7 21,124

-20

176

-5

390

-1

406

13

-19

-4

9

-19

-9

3

-21

-12

4,277

2,470

110

699

2,308

109

371

9,346

439

36,265

- 5 38,078

585 -19

718

667 -10

738

22,200

1 22,000

24,660

1 24,479

146 -21

179

370 -15

435

391

-7

434

4,589

2,065

108

759

2,003

104

6

-7

-2

-8

0

6

4,558

2,157

108

824

1,860

93

475

6,800

340

89

117

50

126

3.2

4.7

4.8

5.5

2.3

3.5

2.7

5.1

0.7

1.9

1.1

1.3

Mid-caps

Monnet Ispat

342

Godawari

97

Sarda Energy

84

Tata Sponge

271

Adhunik Metaliks 3 8

Bhushan Steel 3 0 4

Jai Balaji

35

Rain Comm.

28

Prakash Inds.

30

10.6

3.8

8.9

1.8

5.1

8.9

10.7

2.8

3.0

8.1

4.2

5.9

0.9

3.4

8.4

6.9

2.9

2.0

1.0

0.5

0.4

0.8

0.5

1.0

0.3

0.5

0.2

383 -20

7,710

8

410 14

28,930

55,450

2,106

1.09

52.6

1,930

Note: Detailed table on pg 20

Source: MOSL

5 26,077

2 51,100

0

1,961

-5

1.15

7

0

49.2

1,886

3 3 20,575

1 3 46,065

-23

2,550

-17

1.32

17

6

44.7

1,773

Valuations: Global companies

Price

Steel

A.Mittal

US Steel

Nucor

Gerdau

Bao Steel

EV/EBITDA

CY11 CY12

5.4

5.3

7.2

7.4

6.9

5.8

6.0

4.3

4.6

4.3

4.0

5.2

4.8

4.9

6.2

6.0

5.3

5.6

4.1

4.2

4.0

3.9

P/BV

CY11

0.4

0.8

0.9

1.7

0.9

0.7

0.7

1.1

1.0

2.5

1.7

Source: MMR/LME/Metal Bulletin/SteelPricesIndia/MOSL

EUR 13.2

USD 25.9

USD 38.9

BRL 13.9

CNY 4.7

P o s c o k KRW 386.5

Non-ferrous

Alcoa

USD 8.81

Teck Res. USD 33.86

Xstrata

BHP

Rio Tinto

GBP 9.7

AUD 35.19

AUD 61.8

Note: Detailed table on pg 20 Source: Bloomberg

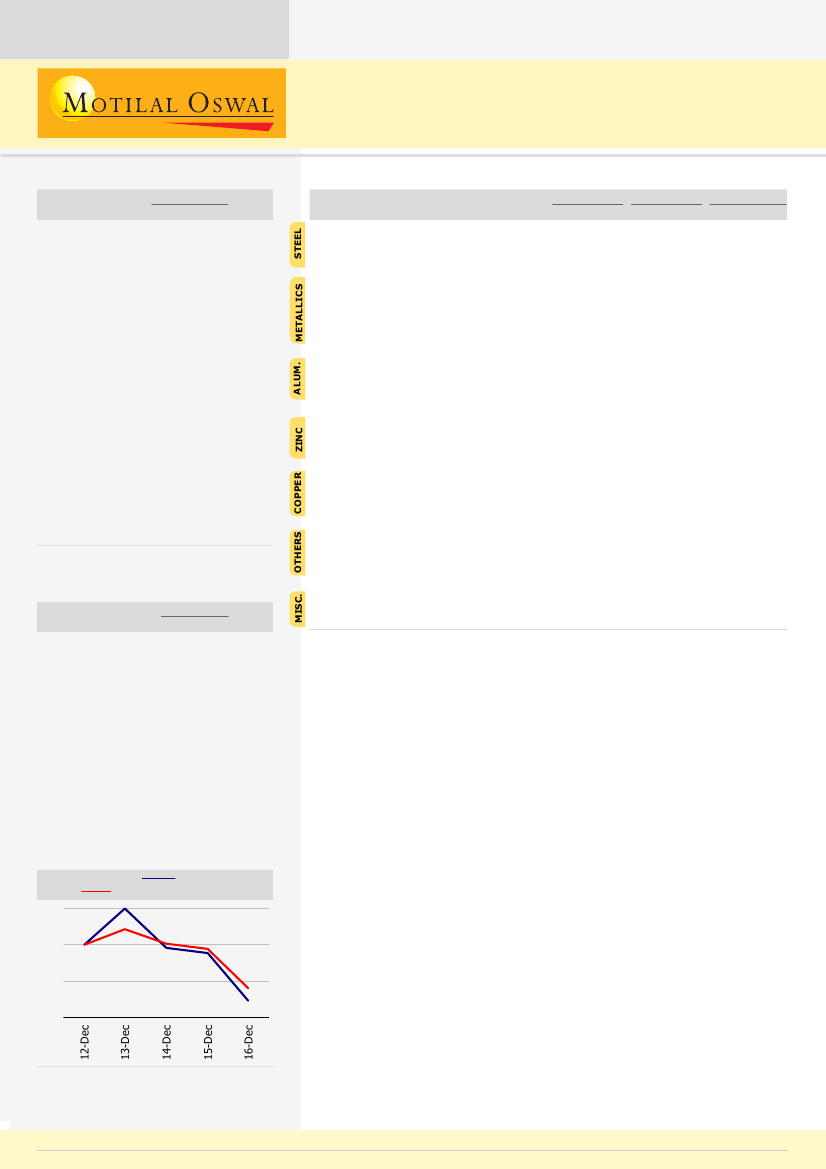

BSE Metals Index v/s Sensex

BSE Metals Index

Sensex

102

100

98

96

Rupee depreciation continues to provide cushion to domestic prices

amidst global commodity downturn

Average LME prices for aluminum, copper and zinc have declined 12%, 16%

and 14% QoQ, respectively, while average domestic prices have corrected

just 3%, 8% and 5% QoQ, respectively. Similarly, average steel prices have

declined QoQ in China (13%), Europe (6%), Russia (7%) and North America

(5%), but steel prices in India continue to find support due to a depreciating

rupee. Average long product steel prices have increased 5% QoQ and flat

product steel prices have increased 2% QoQ in India.

Domestic flat product prices have increased 0.5% WoW, while long product

prices have increased ~2% WoW. Steel prices declined in Russia (4% WoW)

and the Middle East (3% WoW), but increased in North America (2% WoW).

Prices showed a mixed trend/were flat in China, Europe and Turkey.

Benchmark copper treatment and refining charges (TC/RCs) for 2012 have

been set at USc63.5/6.35 per pound, higher than the spot market TC/RCs of

USc20-30/2-3 per pound, and 13.4% higher than the 2011 annual benchmark.

The European Union has approved levying an anti-dumping duty on imports

of China-origin seamless stainless steel pipes and tubes into the region.

Metal demand in China may grow at a slower pace in 2012 and prices may

be lower, according to Mr Wang Huajun, Deputy Secretary General of the

China Nonferrous Metals Industry Association. He further added that demand

for copper, aluminum, lead and zinc may increase 6%, 8%, 7% and 5%,

respectively.

1

Source: Bloomberg

Note: Indexed to 100 on 12 December 2011

Individual stock performance table on pg 21

Sanjay Jain

(SanjayJain@MotilalOswal.com); Tel:+91 22 3982 5412

19 December

Tel:+91 22 3982 5425

Tushar Chaudhari

(Tushar.Chaudhari@MotilalOswal.com);

2011