12 January 2012

3QFY12 Results Update | Sector: Technology

Infosys Technologies

BSE SENSEX

S&P CNX

16,038

Bloomberg

Equity Shares (m)

1,6,12 Rel. Perf. (%)

M.Cap. (INR b)

M.Cap. (USD b)

4,831

INFO IN

571.4

-6/7/-5

1,479.1

28.6

CMP: INR2,589

TP: INR3,225

Buy

52-Week Range (INR) 3,388/2,169

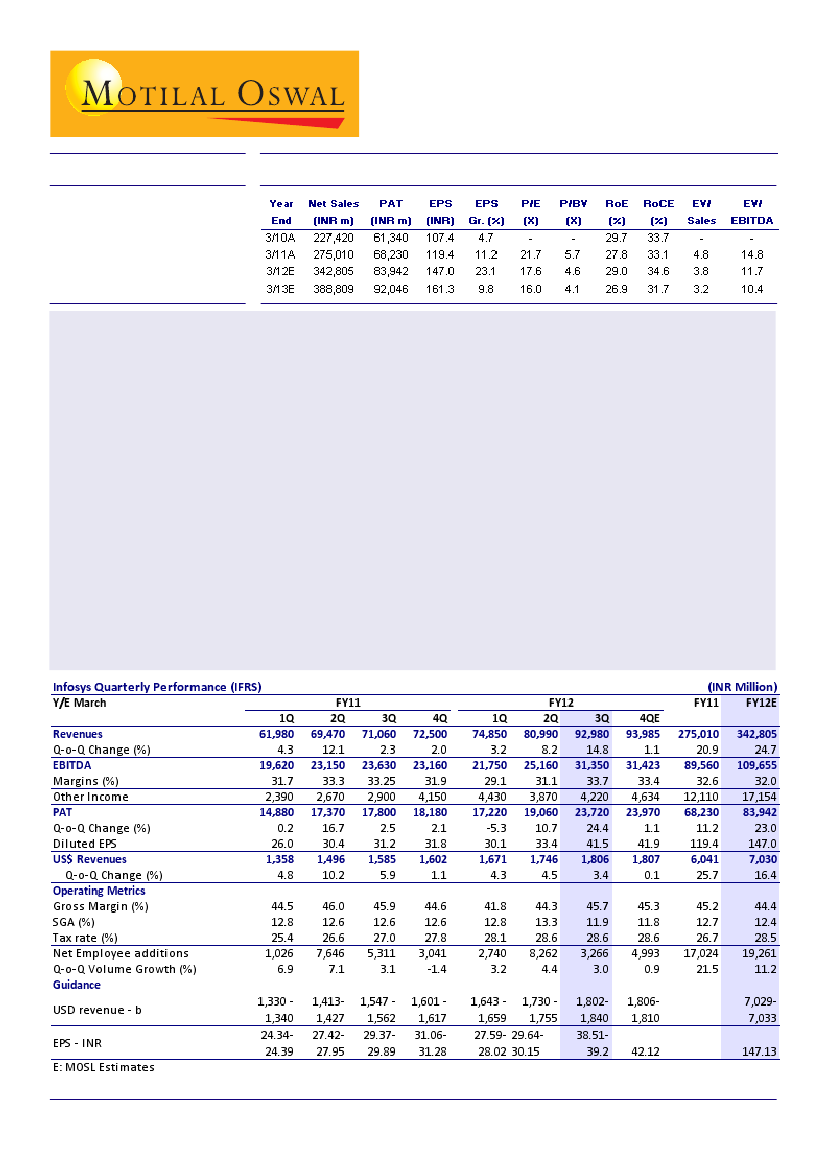

Infosys (INFO) reported a 3.1% volume growth in 3QFY12, lower than its implied volume growth guidance of

4.2-6.4% (our est. of 4% volume growth)

USD revenue growth of 3.4% and EBIT margin expansion of 300bp were ahead of street expectations (our

expectations of 260bp increase), largely driven by a higher INR realization v/s estimates (INR51.37/USD v/s

our estimate of INR50.5/USD). USD revenue growth guidance of 0-0.2% growth for 4Q implies a 0.5-0.7%

volume growth (guidance assumes a 50bp impact from cross currencies), which is disappointing.

Infosys' commentary during the quarter and 4Q guidance indicate rapid deterioration in the environment.

Key positives in 3Q are a 0.8% increase in revenue productivity in constant currency , 5 large deal wins with

2 deals having a TCV of over USD500m and 49 new client additions - the highest in many quarters. Post

conversations with offshore advisors we note that all vendors will report strong deal wins in the current

quarter, however client additions and deal wins from 4QFY12 onwards will be critical.

The currency trade is now over and the market will increase its focus on Infosys' core business fundamentals.

We cut our USD revenue growth estimates for FY13 to 10.5% from 13.6% earlier. We also increase our INR

assumption to INR50/USD from INR48/USD earlier. Our EPS estimates remain unchanged at INR161.3. Assuming

a worst case multiple of 16x FY13E, INR2,580/share is the worst case valuation for the stock.

We maintain our P/E multiple of 20x on the stock despite the deterioration as we will rollover our estimates

to FY14 next quarter. We reiterate our

Buy

rating with a target price of INR3,225.

Nitin Padmanabhan

(Nitin.Padmanabhan@MotilalOswal.com); Tel: +91 22 3982 5426

Ashish Chopra

(Ashish.Chopra@MotilalOswal.com); Tel: 3982 5424