23 January 2012

3QFY12 Results Update | Sector: Metals

Sarda Energy

BSE SENSEX

16,739

S&P CNX

5,049

CMP: INR106

TP: INR120

Neutral

Bloomberg

Equity Shares (m)

52-Wk Range (INR)

1,6,12 Rel. Perf. (%)

M.Cap. (INR b)

M.Cap. (USD m)

SEML IN

34.0

326/72

31/-41/-52

3.6

71.6

Consolidated

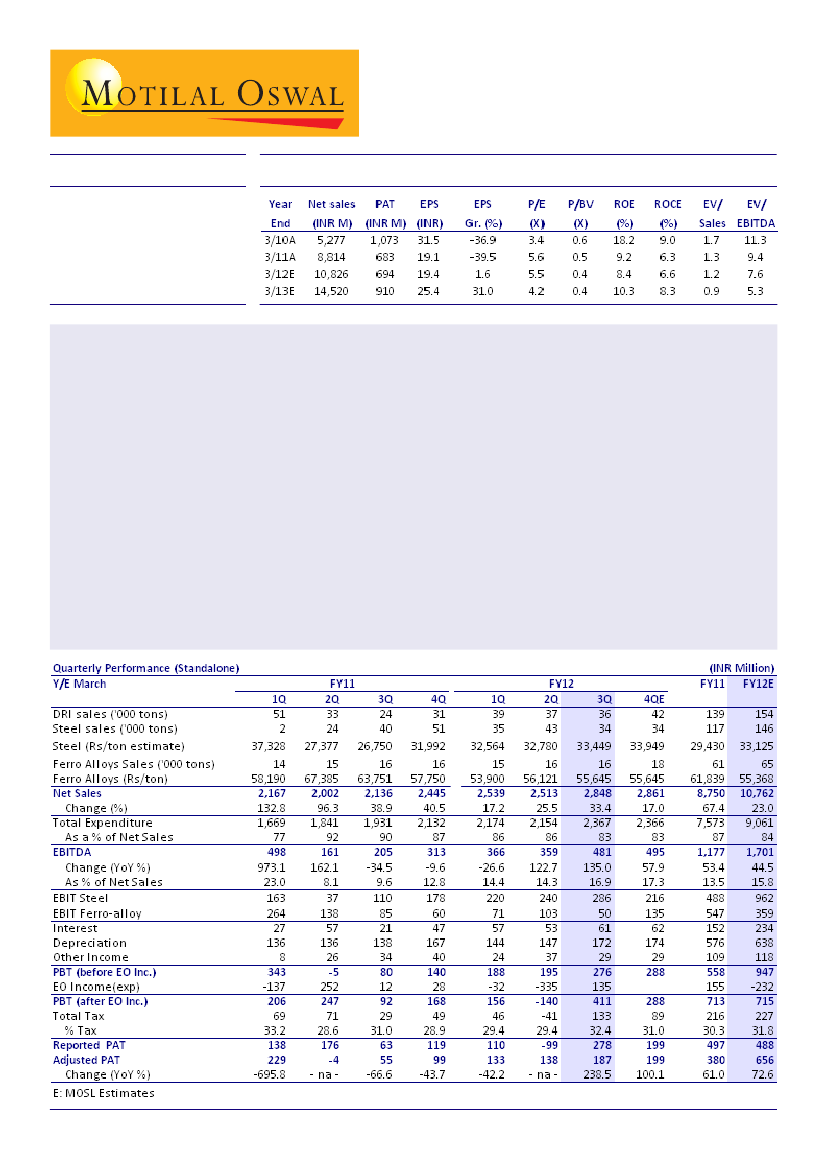

Sarda Energy and Mineral (SEML) posted standalone adjusted PAT of INR187m (up 35% QoQ) for 3QFY12.

Higher coal production, stabilization of pellet plant, and higher merchant power volumes and rates boosted

earnings.

Net sales increased 13% QoQ to INR2.8b (v/s our estimate of INR2.5b), driven by higher pellet and power

sales, and increase in sponge iron prices.

EBITDA increased 34% QoQ to INR481m, driven by increase in production of pellets and coal, higher power

generation, and higher sponge iron prices. Pellets are currently enjoying superior margins due to shortage of

DRI grade iron ore and strong sponge iron prices.

Reported standalone PAT was INR278m. This includes INR137m MTM impact of forex loss reversal, as SEML

has adopted new guidelines for amortization of forex loss over a longer period.

Valuation and view:

After a couple of quarters of subdued performance, the pellet plant has stabilized. The coal

washery, which was started in August 2011, is also ramping up well and mining production has increased. We are

increasing our earnings estimate for FY13 to factor in stabilization of the pellet plant and coal washery, and ramp-

up of coal mining. The stock trades at an EV of 5.3x FY12E EBITDA. Maintain

Neutral.

Sanjay Jain

(SanjayJain@MotilalOswal.com);Tel:+9122 39825412/

Pavas Pethia

(Pavas.Pethia@MotilalOswal.com); +9122 39825413