10 February 2012

3QFY12 Results Update | Sector: Telecom

Tulip Telecom

BSE SENSEX

S&P CNX

17,831

Bloomberg

Equity Shares (m)

52-Week Range (INR)

1,6,12 Rel. Perf. (%)

M.Cap. (INR b)

M.Cap. (USD b)

5,412

TTSL IN

145.0

181/100

-10/-27/-28

16.7

0.3

CMP: INR115

TP: INR120

Neutral

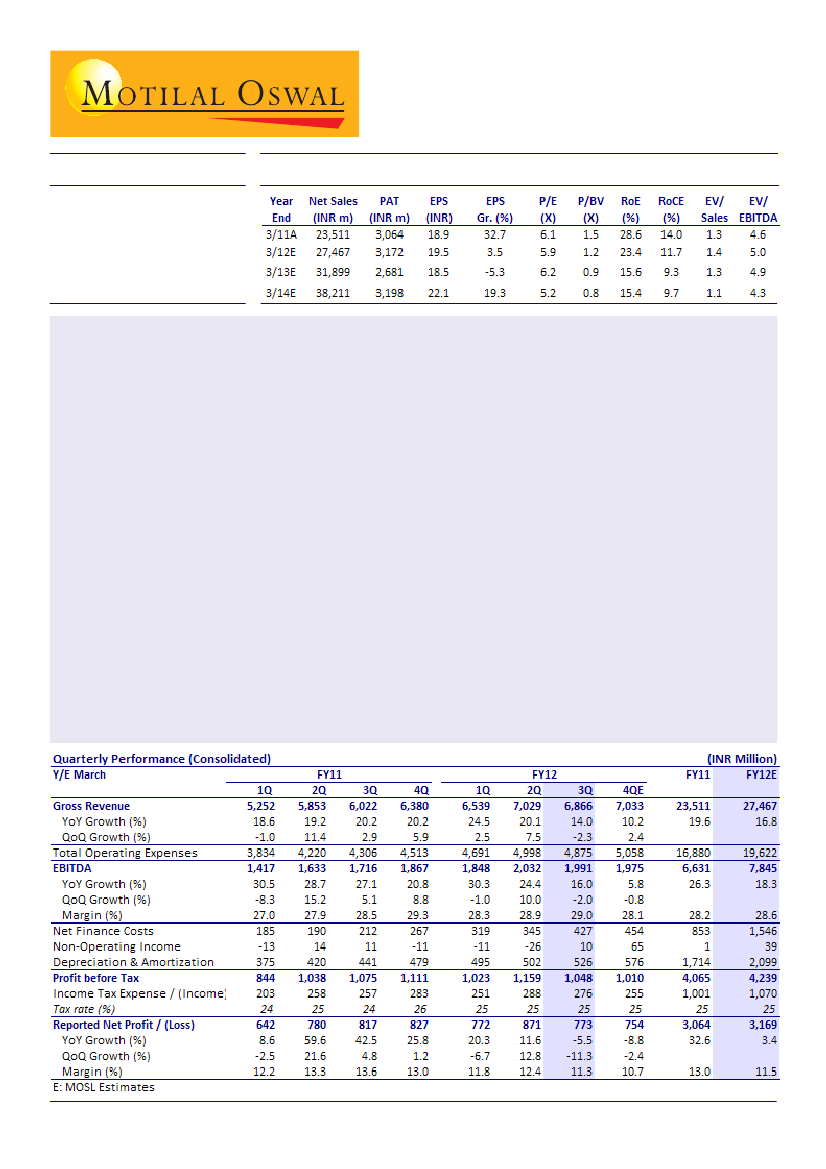

3QFY12 results below estimates:

Tulip Telecom (TTSL) posted a PAT of INR773m for 3QFY12, down 5% YoY and

11% QoQ. Revenue and EBITDA declined 2% QoQ v/s our expectation of 4% growth. EBITDA margin improved

50bp YoY but remained flat QoQ at 29%.

Macro headwinds impacting enterprise spends, data center booking:

The management now expects FY12

revenue growth to be 14-16% (v/s 20% earlier), implying flattish QoQ growth in 4QFY12. While TTSL has been

able to hold EBITDA margin at ~29%, slowdown in revenue growth can impact margins negatively. The data

center business (capital employed: INR3.5b) has not yet begun contributing revenue. While the visible funnel

for data center space has increased to 225,000sf, we note a reduction in target booking to 15-20% by the end

of FY12 v/s the last quarter guidance of 25%.

Leverage levels remain elevated:

During 9MFY12, TTSL added net debt of INR6.1b, including INR0.9b impact

of adverse exchange fluctuations on forex debt. This was the seventh consecutive quarter of increase in net

debt; reported net debt of INR21.4b does not include redemption premium of INR2.1b on FCCB due in August

2012. While the company has been considering various deleveraging options like monetization of stake in

Qualcomm JV, equity raising at parent/subsidiary level, etc, timing of these events remains uncertain.

Downgrade to Neutral:

3QFY12 earnings were 20% lower than we had estimated and leverage concerns

remain unaddressed. We cut our FY12/13/14 EBITDA estimates by 5/10/12% and EPS estimates by 12/18/23%.

We downgrade our stock recommendation to

Neutral,

with a revised target price of INR120. The stock trades

at 6.2x FY13E EPS and at an EV of 4.9x FY13E EBITDA. While valuations are supportive, re-rating would be

contingent on key concerns getting addressed. We would await more clarity on re-financing of upcoming

FCCB redemption, stake sale in Qualcomm BWA venture and revenue ramp-up of data center before taking a

constructive view on the stock.

Shobhit Khare

(Shobhit.Khare@MotilalOswal.com); Tel: +91 22 3982 5428