9 May 2012

4QFY12 Results Update | Sector: Utilities

CESC

BSE SENSEX

16,546

Bloomberg

Equity Shares (m)

52-Week Range (INR)

1,6,12 Rel. Perf. (%)

M.Cap. (INR b)

M.Cap. (USD b)

S&P CNX

5,000

CESC IN

125.6

364/186

0/-1/2

33.2

0.6

* Excl Spencers; fully diluted

CMP: INR262

TP: INR439

Buy

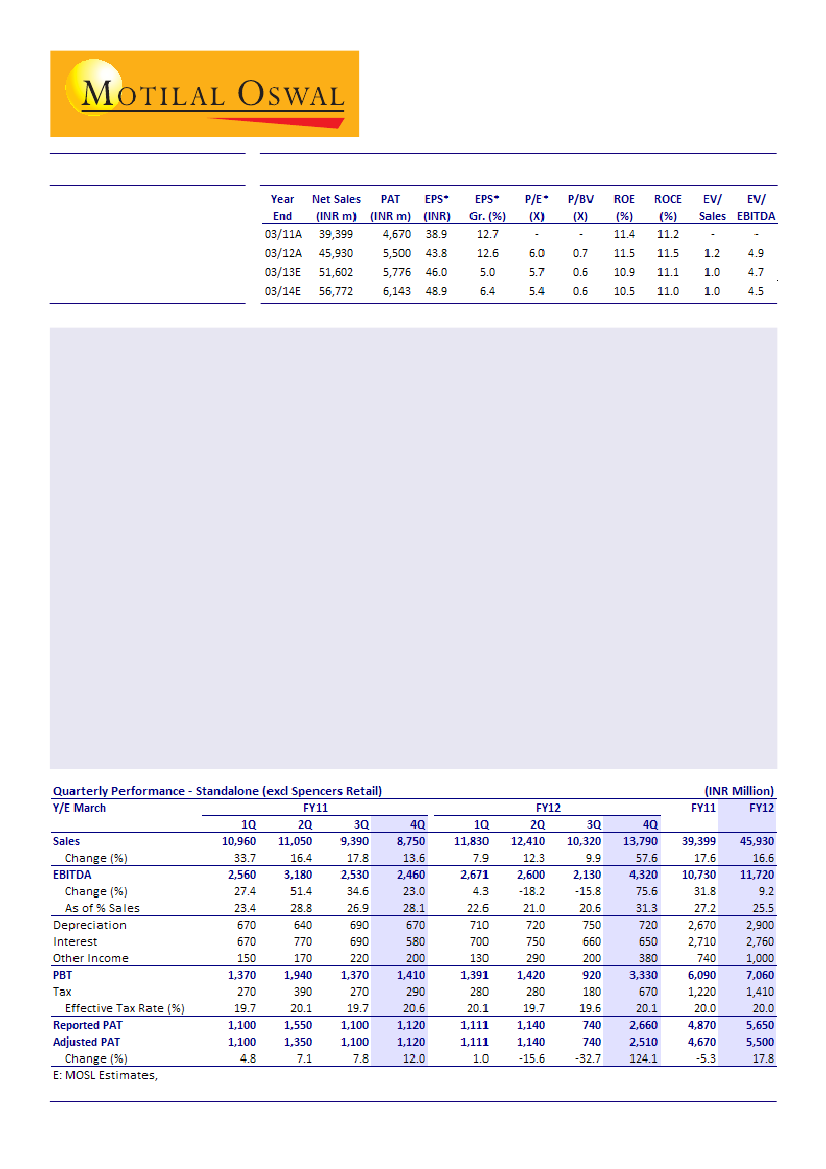

4QFY12 operating results in-line, adjusted PAT boosted by higher other income:

CESC reported 4QFY12 PAT of

INR2.7b and PAT adjusted for sale of scrap of INR150m stood at INR2.5b v/s our estimate of INR2.1b. PAT during

the quarter boosted by other income and arrears recovery. Other income (including operating other income)

stood at INR690m for 4QFY12, ~INR400m higher than our estimate. Also, the tariff order approval led to

increase in core earnings for CESC by ~INR400m.

Steady state operating performance:

During the quarter power generation stood at 2BUs, up 9% YoY while

sales stood at 1.8BUs units (up 3% YoY). Average PLF for the plant stood at 77% v/s 68% YoY. For FY12 PLF for

Budge Budge stands at 90% (vs 83% YoY), Titagarh at 81% (vs 89% YoY), and Southern project at 87% (vs 92%

YoY). CESC purchased ~206MUs in 4Q to meet the power demand for the Kolkatta region and power demand

grew by 3.3% YoY to 2.1BUs.

Tariff order approval improves visibility on core profits, entails higher RoEs:

CESC has got the tariff order

approved for FY12-14E with average capex of INR6b for its distribution business. As a result, its RoE improved

150bp for both its generation and distribution businesses. This has meaningfully improved the core profitability

for the company. We expect CESC's RAB (i.e. regulated equity) to grow from INR25b in FY12 to INR29b in FY14

and core profit to grow from INR3.9b in FY12 to INR4.5b in FY14.

Spencer: Consolidation continues, focus on improving sales, operating profits:

In FY12, Spencer continued to

improve its operating performance with focus on higher sales, consolidation and cost control/efficiencies.

During the year, Spencer closed 35 Small Express Stores, opened 5 Hyper/2 Super Stores and average revenue

grew 11% YoY to INR1,060/sft/month, while same store sales grew 14% to INR1,147/sft/month.

Valuation and view:

We expect CESC to report standalone PAT of INR5.8b in FY13 (up 5% YoY) and INR6.1b in

FY14 (up 6% YoY). Stock trades at P/E of 6x FY13E standalone. Maintain

Buy

with SOTP based TP of INR439/sh.

Nalin Bhatt

(NalinBhatt@MotilalOswal.com) +91 22 3982 5429

Satyam Agarwal

(AgarwalS@MotilalOswal.com)

/

Vishal Periwal

(Vishal.Periwal@MotilalOswal.com)