31 May 2012

Update

Financials

Sharp rise in slippages, large corporate restructuring leading to higher stress

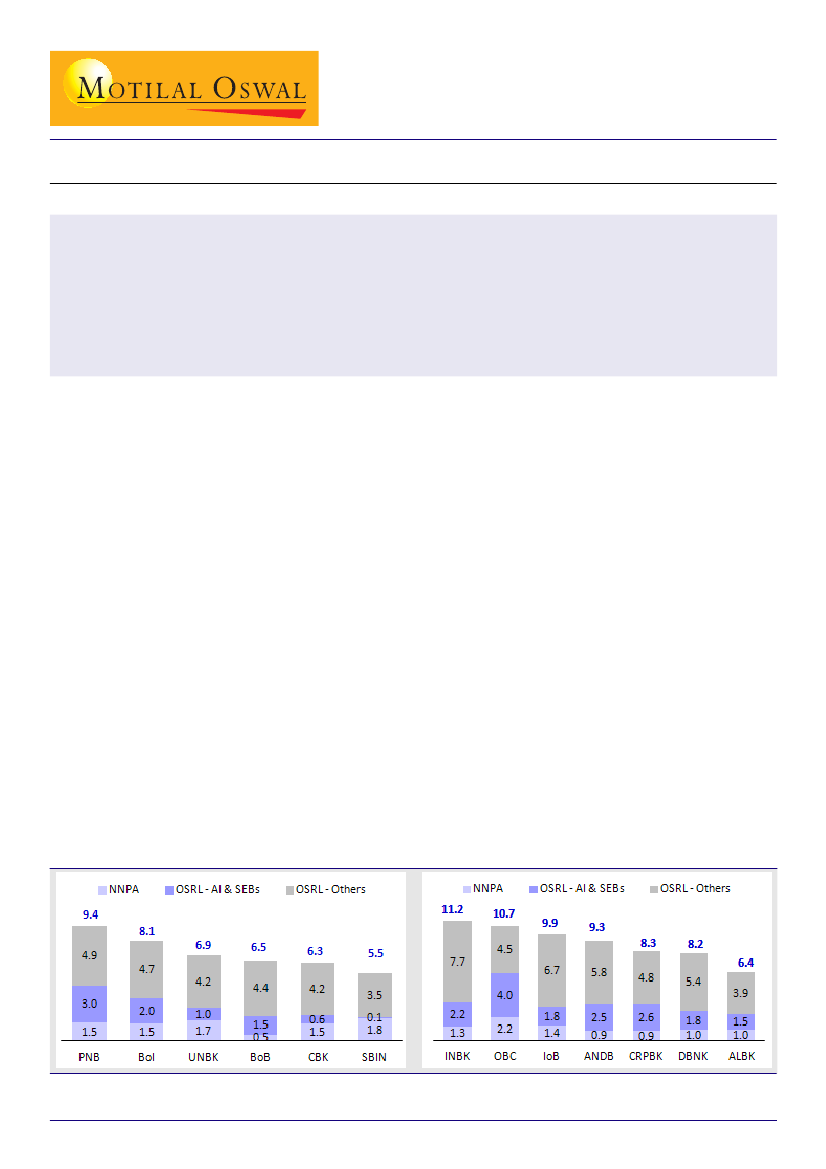

SBIN relatively better than peers; other large PSBs' net stress loans (ex Air India and SEBs) up 75-140bp

Overall net stress loans (NSL, defined as NNPA + outstanding standard restructured loans) for our universe of PSBs (public

sector banks) have increased to 7.3% (5.9% ex Air India and SEBs) v/s 5.1% in FY11. Excluding State Bank of India (SBIN), NSL

for PSBs are up 323bp to 8.13%. AI (Air India) and SEB have contributed bulk of increase in restructured loans, both

combined accounting for 195bp out of 323bp increase.

SBIN has the lowest proportion of NSL on the balance sheet at 5.5% (NNPA of 1.82% and OSRL of 3.65%). Also, it is the only

large PSB where NSL have remained flat YoY.

Ex AI and SEB, large PSBs have reported 75-140bp increase in NSLs, whereas midcap PSBs have reported 100-250bp rise.

PNB and OBC has one of the highest total NSLs; however, ex SEB and AI, their NSL are just 50-100bp higher than peers.

Stress loans increase led by restructuring of state

government entities

Over last one year, NNPA for PSBs are up ~35bp to 1.45%

and OSRL by ~190bp to 5.9% (up ~50bp to 4.5% ex AI and

SEB). Thus, overall NSL for PSBs have increased to 7.3%

(5.9% ex AI and SEB) v/s 5.1% in FY11. FY10 through

1HFY12, OSRL for PSBs remained relatively constant at

~4%. However, sharp increase in restructuring in 2HFY12

led to significant increase of OSRL as a proportion of

outstanding loan. Over past two quarters, OSRL has

increased from 4% to 5.9% in FY12.

Stress Loan rise significantly for large PSBs

Ex SBIN, stress loans among large PSBs increased 170-

450bp (75-140bp excluding AI and SEB). Among large

banks, PNB has the highest proportion of NSL on its

balance sheet at 9.4% (1.9x of FY11), of which ~300bp is

contributed by SEB and AI. Higher contribution of SEB

and AI (400bp of loans) is also leading to significantly

higher NSL for OBC (10.7% of loans). BOB's NSL is

relatively better than peers at ~5% (ex SEB and AI); but

this should also be viewed in the context of strong loan

CAGR of 28% over FY10-12.

Restructuring to increase further; asset quality to drive

valuation:

Challenging macroeconomic environment is

moderating growth and raising NSL in the system. While

GNPAs have peaked, further stress on account of SEB

restructuring (INR122b, 50bp of the outstanding loans)

and higher CDR cases will keep asset quality and

valuations under pressure. We like banks with strong

liability franchise, superior capitalization, and stability

at the top management level (specifically for PSBs). Top

picks:

SBIN, PNB, ICICIBC, YES

and

UNBK.

Smaller banks' NSL in the range of 6-11%

SBIN's NSL performance better than peers

Although SBIN faced higher challenges in terms of

significant increase in net slippages over past two years

(average of INR126b over FY11/12 v/s average of ~INR43b

over FY07-10), 16pp improvement in PCR (+9%

improvement in last one year) and the bank's

conservative restructuring policy led to 50bp decline in

NSL to 5.5% during the same period. Even excluding

restructuring of AI and SEB, SBIN's NSL remains the

lowest among PSBs at 5.3%.

NSL: PNB highest among large PSBs; SBIN much better

NSL:

Net Stressed Loans |OSRL: Outstanding Standard Restructured Loans

Alpesh Mehta

(Alpesh.Mehta@MotilalOswal.com) + 91 22 3982 5415

Sohail Halai

(Sohail.Halai@MotilalOswal.com) /

Umang Shah

(Umang.Shah@MotilalOswal.com)