1 August 2012

1QFY13 Results Update | Sector: Oil & Gas

Petronet LNG

BSE SENSEX

S&P CNX

17,236

Bloomberg

Equity Shares (m)

52-Week Range (INR)

1,6,12 Rel. Perf. (%)

M.Cap. (INR b)

M.Cap. (USD b)

5,229

PLNG IN

750.0

186/122

3/-11/-10

109.7

2.0

CMP: INR146

TP: INR205

Buy

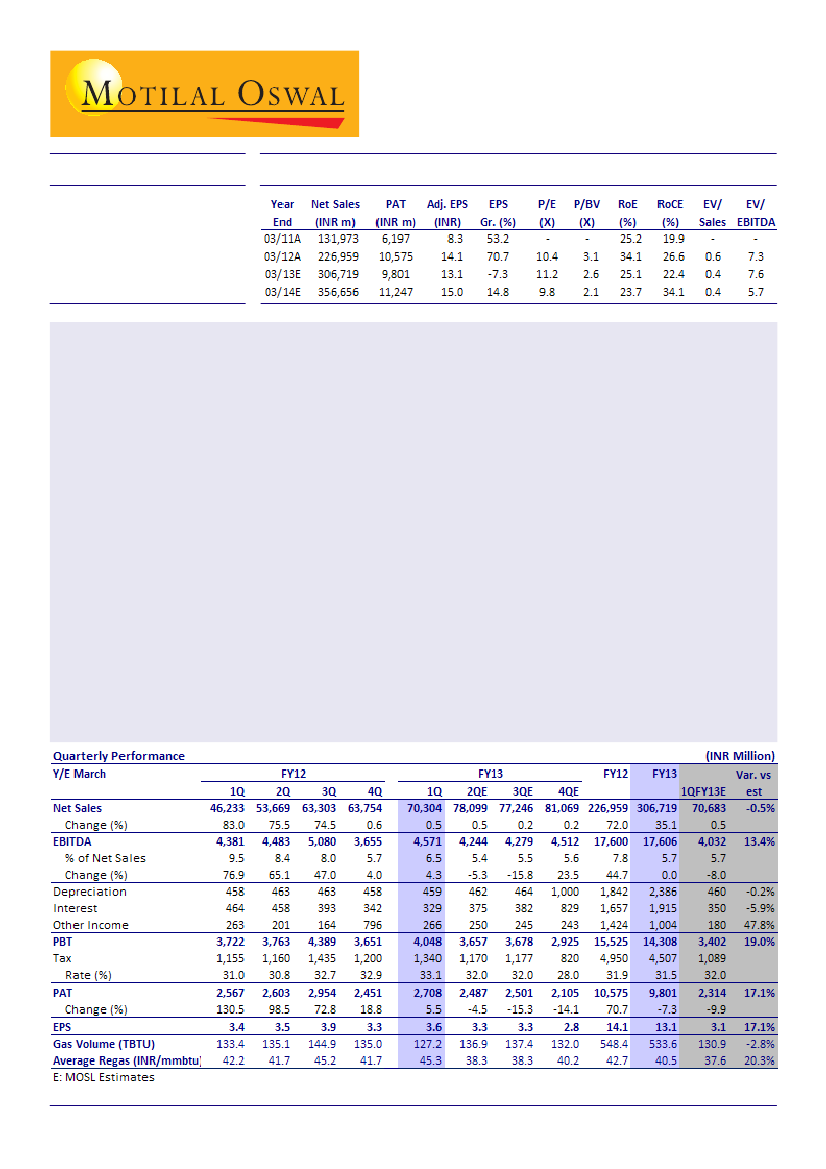

1QFY13 numbers ahead of estimates:

Petronet LNG's (PLNG) reported numbers for 1QFY13 were ahead of

consensus/our estimates. EBITDA was INR4.6b v/s our estimate of INR4b. PAT was up 5% YoY and 10% QoQ at

INR2.7b v/s our estimate of INR2.3b. Profitability was higher than we had expected despite lower volumes

(127tbtu v/s our estimate of 131tbtu) due to: (a) higher implied marketing margin of USD0.64/mmbtu (v/s our

estimate of USD0.28/mmbtu), and (b) INR200m savings on account of dry docking of one charter ship. Variation

(in percentage terms) is higher at the PAT level due to lower interest expense and higher other income.

Capacity expansion projects on track:

PLNG expects to commission its Kochi terminal by December 2012 and

also expects simultaneous completion of phase-I (44km) of its Kochi-Bangalore pipeline, through which it

will supply gas. Further, it expects to complete (a) its second jetty project at Dahej by 4QFY14 (additional

capacity of 3mmt), (b) Dahej expansion by the end of 2015 (taking overall capacity to 18mmt), and (c)

Gangavaram terminal by the end of 2016 and interim FSRU (floating storage and re-gasification unit) by the

end of 2014.

Valuation and view:

We expect PLNG to continue to benefit from India's large gas deficit through (a) higher

utilization (>100%) levels, and (b) higher marketing margins on spot volumes. FY13 earnings would be muted

- while the company would begin to account for Kochi terminal's depreciation in FY13, corresponding revenue

contribution would start only in FY14. PLNG's next earnings growth cycle would come post FY13, led by (1)

volume ramp-up at Kochi, and (2) commissioning of the second jetty at Dahej. We model Dahej volumes at

10.6/11.5mmt and Kochi volumes at 0.2/1.1mmt for FY13/14. The stock trades at 9.8x FY14E EPS of INR15. Our

target price of INR205 is based on the average of two valuation methodologies (1) P/E (13x FY14E EPS), and (2)

DCF (INR215). Maintain

Buy.

Harshad Borawake

(HarshadBorawake@MotilalOswal.com); +91 22 3982 5432

Deepak Dult

(Deepak.Dult@MotilalOswal.com); +91 22 3982 5445

Investors are advised to refer through disclosures made at the end of the Research Report.

1