10 August 2012

1QFY13 Results Update | Sector: Automobiles

Tata Motors

BSE SENSEX

17,561

Bloomberg

Diluted Eq.Shares (m)

52-Week Range (INR

1,6,12 Rel. Perf. (%)

M.Cap. (INR b)

M.Cap. (USD b)

S&P CNX

5,323

TTMT IN

3,323.8

321/138

-3/-5/46

794.4

14.4

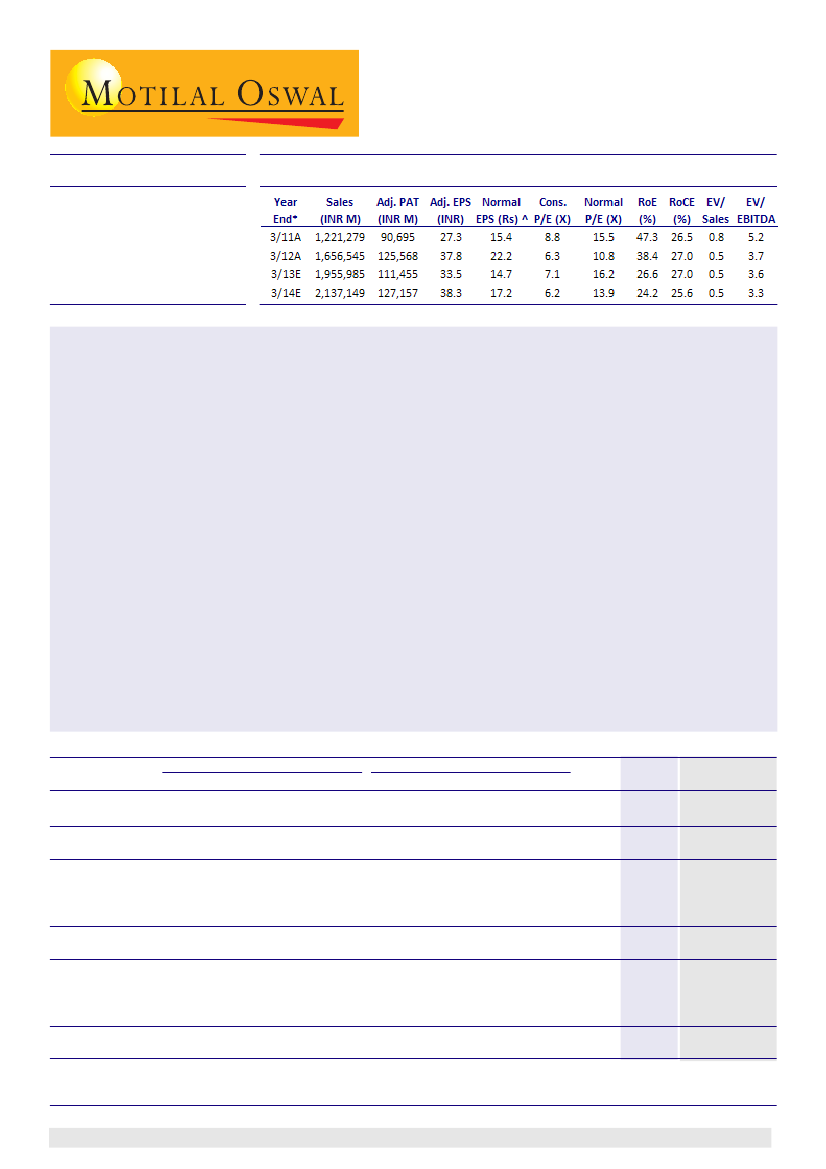

* Consolidated; ^ Normalized for capitalized expenses

CMP: INR239

TP: INR300

Buy

Tata Motors’ (TTMT) operating performance for 1QFY13 was better than we had expected. Margins in both the JLR

and standalone businesses were higher than our expectations. Consolidated EBITDA margin was 13.3% (v/s our

estimate of 12.2%) and adjusted PAT was INR25.6b (v/s our estimate of INR23.3b), driven by (a) favorable mix and

lower forex loss in JLR, (b) favorable mix, lower raw material cost and higher other income in standalone business,

(c) currency gains on JLR translation, (d) despite higher tax in JLR.

JLR’s realizations improved 3.2% QoQ (flat YoY) to GBP43,594 (v/s our estimate of GBP42,363), driven by

favorable mix. EBITDA margin declined 10bp QoQ (increased 110bp YoY) to 14.5% (v/s our estimate of 13.7%),

driven by higher capitalization (~120bp QoQ), which offset the impact of ~130bp QoQ higher cost. However,

higher tax at 29% (v/s our estimate of 19%) restricted JLR’s adjusted PAT.

S/A volumes declined 4% YoY (34% QoQ), impacted by decline in M&HCVs and PVs, despite growth in LCV

volumes. Realizations declined ~5% YoY (2% QoQ) to INR557k on adverse product mix, resulting in revenue

decline of 9% YoY (36% QoQ) to INR105b. EBITDA margin declined 220bp QoQ (150bp YoY) to 7.3% (v/s our

estimate of 5.5%), impacted by negative operating leverage.

While the management indicated that demand for Evoque remains healthy, it highlighted that JLR may not

remain isolated from the worsening macro environment in some key markets. However, it has maintained its

FY13 volume guidance of ~370,000 units and EBITDA margin of ~15%.

Valuation and view:

Our consolidated EPS estimate for FY13 has been downgraded by ~5% to INR33.5 (11%

downgrade in normalized EPS to INR14.7) due to increase in JLR’s tax rate, despite 9% upgrade in our EBITDA

estimate. The stock is trading at 7.1x FY13E and 6.2x FY14E consolidated EPS. Maintain

Buy.

Consolidated Quarterly Performance

Y/E March

1Q

Total Op Income

332,888

Growth (%)

23.0

EBITDA

42,358

EBITDA Margins (%)

12.7

Depreciation

11,432

Other Income

1,658

Interest Expenses

8,556

EO Exp/(Inc)

570

PBT after EO Exp

23,458

Tax rate (%)

15.0

PAT

19,939

Minority Interest

-39

Share

of Associates

96

Adj PAT

20,481

Growth (%)

(3.5)

E: MOSL Estimates

FY12

FY13

FY12

FY13E

2Q

3Q

4Q

1Q

2Q

3Q

4Q

361,975 452,603 509,079 433,236 463,481 479,878 579,390 1,656,545 1,955,985

26.9

44.0

44.3

30.1

28.0

6.0

13.8

35.6

18.1

45,039 68,270 67,445 57,548 60,716 58,545 75,971 223,112 252,781

12.4

15.1

13.2

13.3

13.1

12.2

13.1

13.5

12.9

13,308 16,159 15,354 15,659 16,000 16,500 21,179 56,254 69,338

608

1,675

1,586

2,386

1,250

1,500

1,700

6,618

6,836

5,251

7,204

7,721

8,044

7,000

7,000

7,831 29,822 29,875

4,390

1,643

1,713

4,405

0

0

0

8,315

4,405

22,700 44,938 44,243 31,826 38,966 36,545 48,661 135,339 155,999

16.0

23.8

-41.3

27.3

31.3

31.3

31.5

-0.3

30.5

19,069 34,227 62,504 23,138 26,789 25,125 33,321 135,739 108,373

-335

-210

-239

-276

-250

-175

22

-823

-679

40

22,461

6.4

38

35,307

43.9

75

44,403

79.2

-414

25,651

25.2

160

26,699

18.9

190

25,140

-28.8

764

249

700

34,107 125,568 111,455

-23.2

38.5

-11.2

(INR Million)

FY13

Var

1QE

(%)

430,668

1

28.28

52,542

10

12.2 110bp

16,500

-5

1,350

77

7,500

7

0

29,432

8

20.87 640bp

23,290

-1

-100

176

150

23,340

28.2

-376

10

Jinesh Gandhi

(Jinesh@MotilalOswal.com) + 91 22 3982 5416

Chirag Jain

(Chirag.Jain@MotilalOswal.com) + 91 22 3982 5418

Investors are advised to refer through disclosures made at the end of the Research Report.