6 November 2012

2QFY13 Results Update | Sector: Cement

India Cements

BSE SENSEX

S&P CNX

18,763

Bloomberg

Equity Shares (m)

52-Week Range (INR)

1,6,12 Rel. Perf. (%)

M.Cap. (INR b)

M.Cap. (USD b)

5,704

ICEM IN

307.2

119/65

6/3/15

30.0

0.5

CMP: INR98

TP: INR127

Buy

* Consolidated

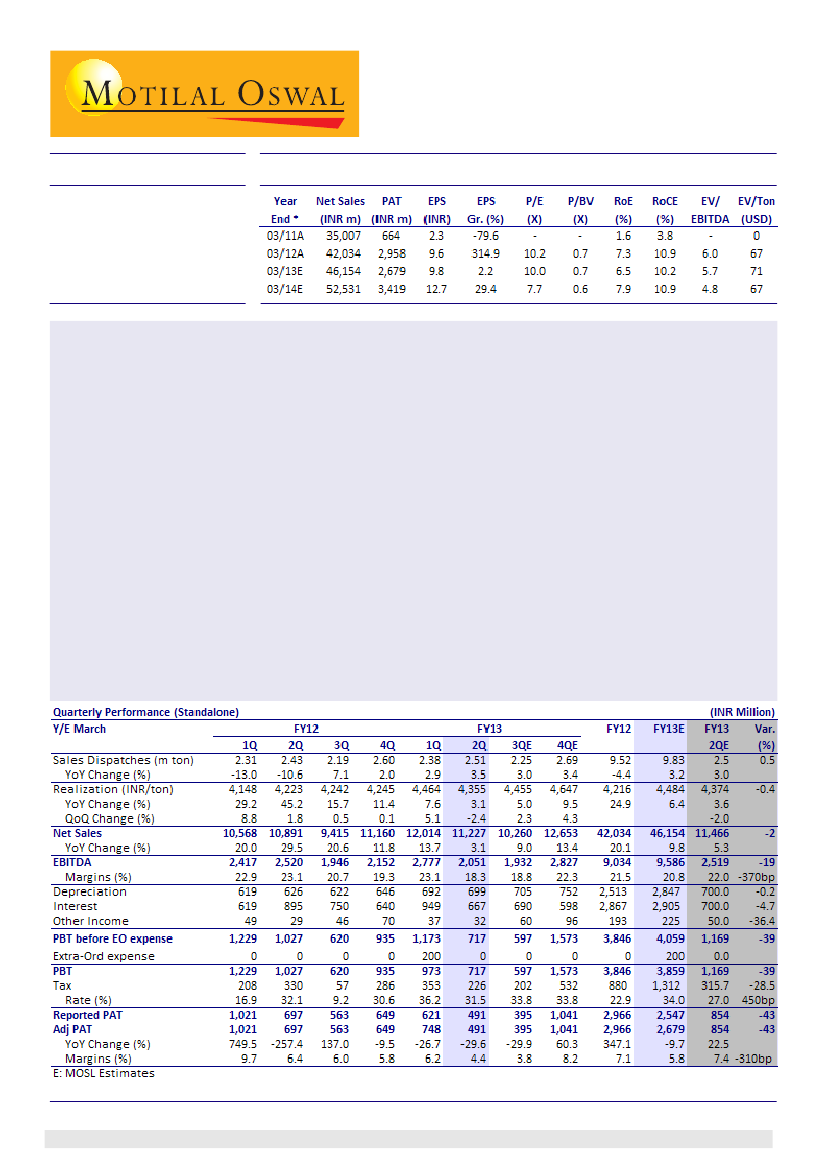

Cement volume, realization largely in-line:

India Cements' (ICEM) cement volume grew 3.5% YoY (5.5% QoQ)

to 2.51m tons (in-line), while realization declined 3.1% YoY (2.4% QoQ) to INR4,355/ton (v/s our estimate of

INR4,374/ton). Revenue grew 3.1% YoY (-6.6% QoQ) to INR11.2b (v/s our estimate of INR11.5b).

Higher energy cost impacts cement EBITDA:

Energy cost inflation of ~8% QoQ impacted performance. EBITDA

margin declined to 18.3% (v/s our estimate of 22%; down 380bp QoQ/YoY). Pure cement EBITDA/ton declined

to INR771 (v/s INR1,029/ton in 1QFY13 and our estimate of INR939/ton). Higher tax rate impacted PAT further

- down 30% YoY and 34% QoQ to INR491m.

Other takeaways:

(a) Demand remains lackluster in the key market of AP owing to major projects failing to

take off, (b) Indonesian captive coal mine has started mining activity, with 15-20,000 ton of coal already

mined (c) Prices in key southern market stable, except in AP; expects to pass-on cost push; Prices in AP have

recovered by INR30-35/bag, after declining by INR60-70/bag in September 2012; expects further recovery in

coming months, (d) Power situation in AP likely to improve only from 1QFY14, which will coincide with

commissioning of its 50MW CPP at its AP plant, (e) Expects part benefit of softening in imported coal prices

to reflect in 3QFY14 and balance in 4QFY14.

Downgrading estimates; maintain Buy:

We downgrade our consolidated EPS estimates for FY13/FY14 by

12%/14% to INR9.8/INR12.7, as we factor in higher energy cost and higher tax. The stock is valued at 7.7x FY14E

EPS (ex-treasury stock), 4.8x FY14E EBITDA and USD67/ton (at 15.1m ton capacity on pro-rata basis). Maintain

Buy

with a target price of INR127 (EV of ~5.5x FY14E EBITDA or USD80/ton).

Jinesh Gandhi

(Jinesh@MotilalOswal.com); +91 22 3982 5416

Sandipan Pal

(Sandipan.Pal@MotilalOswal.com); +9122 3982 5436

Investors are advised to refer through disclosures made at the end of the Research Report.

1