17 January 2013

3QFY13 Results Update |

Sector: Automobiles

Bajaj Auto

BSE Sensex

19,987

Bloomberg

Equity Shares (m)

M.Cap. (INR b)/(USD b)

1,6,12 Rel.Perf.(%)

S&P CNX

6,057

BJAUT IN

289.4

601/11

-4/21/23

CMP: INR2,076

TP: INR2,250

Buy

52-Week Range (INR) 2,229/1,410

Financials & Valuation (INR b)

Y/E March

Sales

EBITDA

NP

EPS Gr. (%)

BV/Sh. (INR)

RoE (%)

RoCE (%)

Payout (%)

Valuations

P/E (x)

P/BV (x)

EV/EBITDA (x)

Div. Yield (%)

2013E 2014E 2015E

202.9

37.3

30.3

(2.5)

45.2

62.5

55.9

19.8

8.1

14.0

2.4

239.1

47.1

38.3

26.4

46.3

63.7

53.0

15.7

6.5

10.6

2.9

276.2

53.8

43.4

13.2

42.3

58.1

50.8

13.9

5.3

8.8

3.1

Adj. EPS (INR) 104.7 132.4 149.8

255.0 317.2 391.0

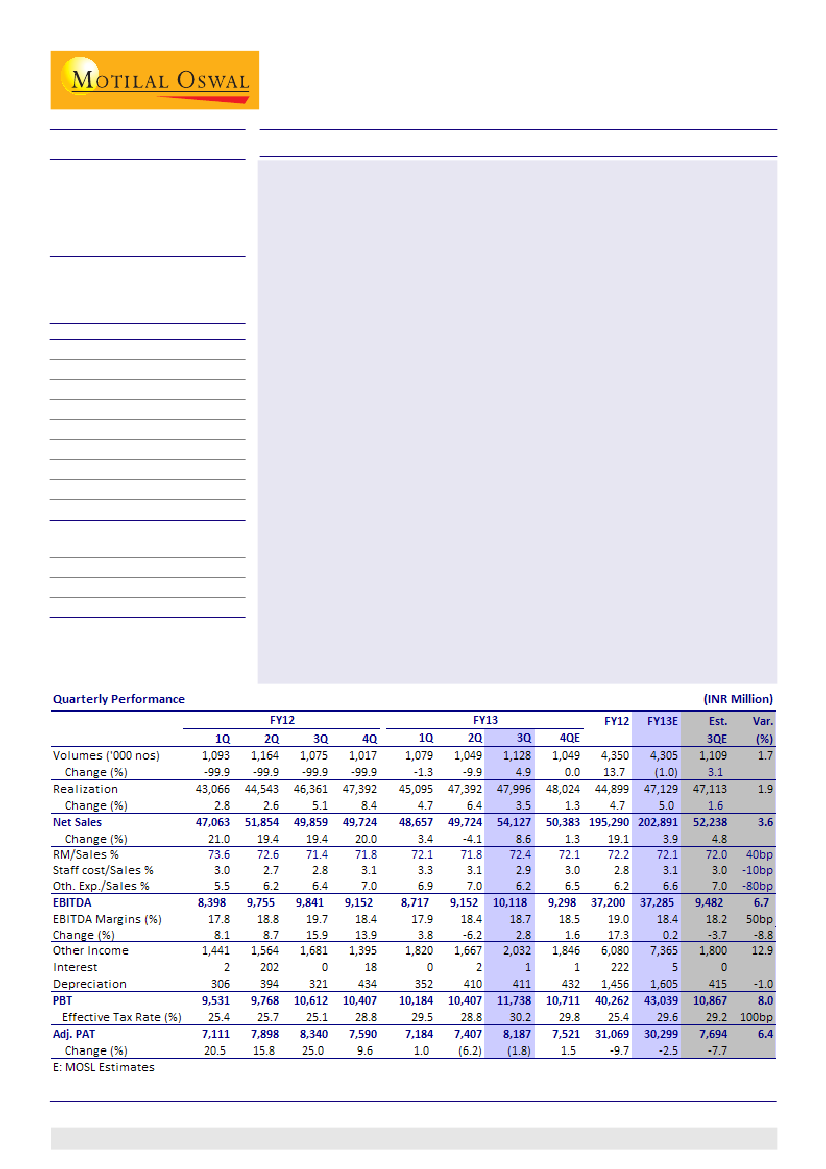

Bajaj Auto (BJAUT) posted above estimate results, with EBITDA margins at 18.7%

(v/s est 18.2%) and adj. PAT at INR8.2b (v/s est. INR7.7b), driven by richer product

mix and higher export realizations. New launches helped 5% volume growth.

Earnings call highlights

Management expects 4Q volumes to remain muted ; however, no discounts/

subventions being offered, even in 3Ws.

Expects domestic motorcycle growth to pick up in FY14 on better consumer

sentiments and new launches. Exports to grow by over 10% in FY14; expects

15-18% CAGR in exports over 3-5 years, led primarily by Africa.

FY14 export exposure of USD900m hedged at a base rate of 53 INR/USD

(average 54, v/s 49 in FY13); benefit of favorable currency could be passed on

to boost volumes.

Upgrade FY13E/FY14E EPS est by ~1.2%/2.9%

We upgrade FY13E/FY14E EPS by 1.2%/2.9% to factor higher export realizations

driven by INR depreciation. We model INR/USD rate of 49/54 for FY13E/FY14E.

Valuation and view

New launches and recovery in domestic two-wheeler industry to drive 13%

volume CAGR over FY13E-15E in domestic motorcycles. This coupled with a

recovery in export volumes and 3Ws (launch of a completely new range) to

drive 14.6% overall volume CAGR. Volume growth coupled with favorable

currency will drive 19.6% earnings CAGR over FY13E-15E.

The stock is valued at 15.7x FY14E EPS of INR132.4 and 13.9x FY15E EPS of

INR149.8. Our estimates could see upgrades for export realizations above 54

(every INR1 depreciation would boost margins by 65bp, EPS by 3.2% for FY14E/

15E). Maintain

Buy

with a target price of INR2,250 (15x FY15E EPS).

Jinesh Gandhi

(Jinesh@MotilalOswal.com) + 91 22 3982 5416

Chirag Jain

(Chirag.Jain@MotilalOswal.com) + 91 22 3982 5418

Investors are advised to refer through disclosures made at the end of the Research Report.

1