3 June 2013

4QFY13 Results Update |

Sector: Real Estate

Phoenix Mills

BSE Sensex

19,760

Bloomberg

Equity Shares (m)

M.Cap. (INR b)/(USD b)

52-Week Range (INR)

1,6,12 Rel. Perf. (%)

S&P CNX

5,986

PHNX IN

144.8

40.5/0.7

293/155

2/33/25

CMP: INR279

TP: INR301

Buy

Financials & Valuation (INR b)

Y/E March

Net Sales

EBITDA

Adj PAT

EPS (INR)

EPS Gr. (%)

BV/Sh. (INR)

RoE (%)

RoCE (%)

Payout (%)

Valuations

P/E (x)

P/BV (x)

EV/EBITDA (x)

Div. Yield (%)

2013 2014E 2015E

4.7

2.6

0.8

5.8

-20.3

124.7

4.7

6.7

40.3

48.1

2.2

22.9

0.7

9.9

4.8

1.1

7.8

34.1

130.1

6.0

9.9

30.0

35.9

2.1

13.5

0.7

12.9

6.0

1.9

13.3

70.2

139.9

9.5

11.6

26.5

21.1

2.0

10.3

1.1

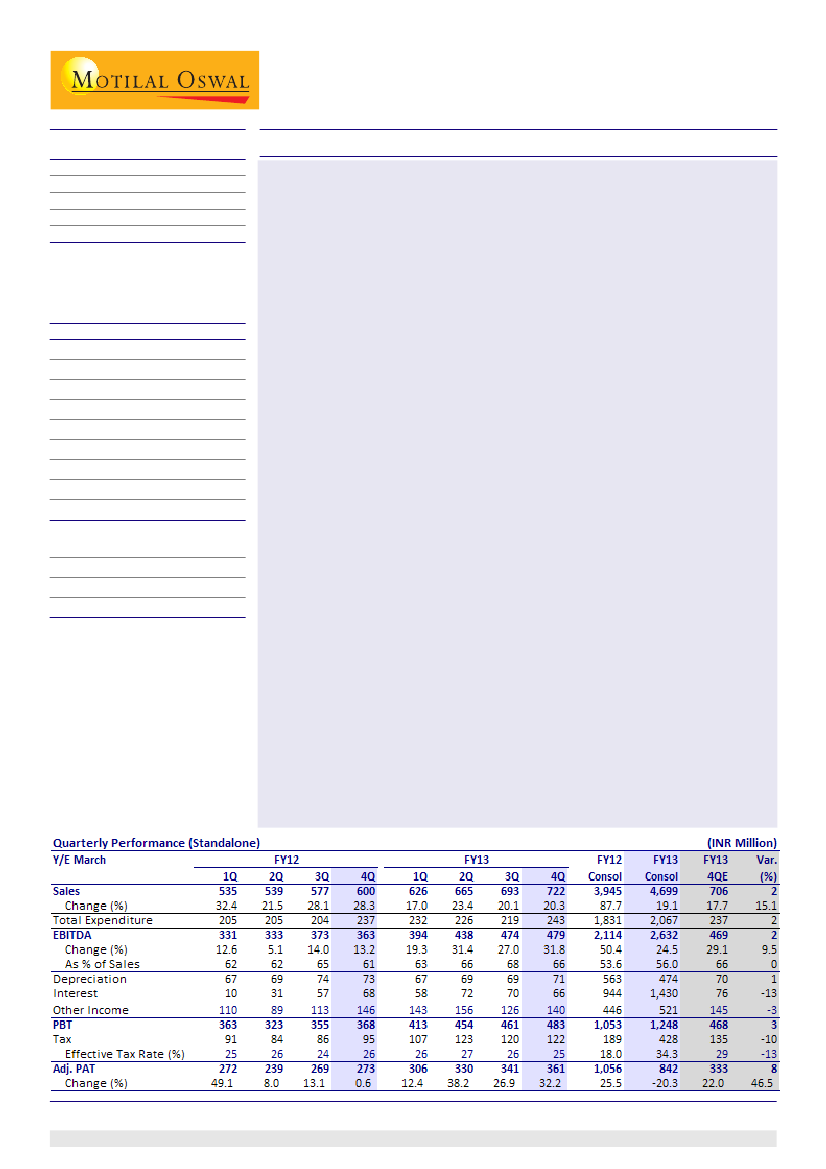

Phoenix Mills' 4QFY13 standalone EBITDA was in line with est. at INR469m

(+32%YoY, +1% QoQ). Revenue stood at INR722m (+20%YoY, +4%QoQ, v/s est.

of INR706m); EBITDA margin down by 2pp QoQ to 66%. PAT stood at INR361m

(v/s est of INR333m). FY13 consolidated revenue stood at INR4.7b (v/s est. of

INR4.5b), EBITDA of INR2.6b (in-line) and PAT of INR842m (v/s est of INR1b).

High street Phoenix (HSP) rentals grew +5%QoQ/+23%YoY to INR653m in

4QFY13, led by +17%YoY growth in consumption. Average rentals grew

+4%QoQ and +17% YoY to INR212/sf/m in 4QFY13. FY13 rental at HSP stood at

INR2.4b v/s our estimate of INR2.32b in FY13.

During 4QFY13, PHNX has witnessed moderation in ramp up progress across

its market city retails, barring Chennai. Chennai mall has shown strong ramp-

up progress as expected due to its very attractive locational advantage. In

terms of trading density, the mall has already surpassed other three market

city malls, which got operational almost 9-12 months ahead of it.

After a strong 1HFY13, the monetization pace in phase IIs of the market city

projects moderates in 3QFY13 and the trend continued in 4Q as well. PHNX

plans to launch 3-4msf of residential projects over next 12 months including

Bangalore East (1msf), Phase II of Bangalore West (2msf), Pune (0.3msf) and

last phase of Chennai (0.4msf).

Due to steady customer collections and negative working capital status in

One Bangalore West project, the SPV Palladium Constructions has bought

back INR781m worth of share, leading to an inflow of INR547m to PHNX in

4QFY13 (owing to its 70% stake in SPV).

The board has approved stake purchase of INR1.4b in various market city

projects over next 24 months. This comprises: (1)Purchase of Edelweiss

Property Fund portfolio in PML group projects for INR690m; (2) Purchase of

IL&FS 24% stake in Vamona Developers (Phoenix Market city, Pune) for

INR716m.

With these, PHNX would have overall capital commitment of INR1.9b for

raising stakes in various SPVs over FY14-15.

Consolidated net debt stood at INR17.7b (net DER 1x), up by INR3.4b QoQ on

account of consolidation of Bangalore East SPV in 4Q.

Sandipan Pal

(Sandipan.Pal@MotilalOswal.com); +91 22 3982 5436

Investors are advised to refer through disclosures made at the end of the Research Report.