Metals Weekly

7 October 2013

Metals Weekly

Valuations: Indian companies

Price

EV/EBITDA P/BV

(INR) FY14E FY15E FY14E

Steel

Tata Steel

288

SAIL

55

JSW Steel

774

JSPL

236

NMDC

124

Non-ferrous

Hindalco

118

Sesa-Sterlite 187

HZL

132

Nalco

33

Rain Industries 39

6.0

7.7

6.7

8.4

3.8

7.8

5.8

4.3

3.8

4.9

6.3

8.4

6.4

6.1

3.7

6.2

5.0

3.6

3.3

4.1

1.2

0.5

1.1

1.0

1.6

1.0

0.7

1.5

0.7

0.5

TMT- Mumbai (INR/ton)

HRC- Mumbai (INR/ton)

HRC (USD/ton) fob CIS

Metal Prices

CMP

7-Oct

34,600

38,219

543

%

-2

-3

-1

0

0

-1

-2

0

0

1

0

-3

0

-1

-1

-1

-1

-2

-2

-3

0

Week

30-Sep

35,300

39,457

550

20,300

25,000

133

245

351

1,789

111

5,375

1,880

116

1,024

Quarter

%

1-Jul

6 32,600

10 34,673

6

510

7 19,000

1 24,800

12

117

9

220

1

347

3

7

-1

0

6

-5

1,731

104

5,436

1,823

109

1,061

6,750

402

666

YTD FY13

% 1-Apr

-1 34,900

5 36,565

-4

565

3

3

-4

-9

-9

-5

9

3

-2

14

-13

-6

10

-8

1

-9

-3

-1

19,800

24,200

138

265

385

1,881

102

5,228

1,870

102

1,171

7,582

408

571

29,526

52,621

2,094

1.03

Sponge iron - Raipur (INR/ton)

20,300

Pig iron - Raipur (INR/ton)

25,000

Iron ore spot (USD/ton) cfr China

132

Coke (USD/ton) fob

240

Shred. scrap (USD/ton) Rotterdam

352

LME Spot (USD/ton)

Indian prices (INR ‘000/ton)

LME inventories (‘000 ton)

LME Spot (USD/ton)

Indian prices (INR ‘000/ton)

LME inventories (‘000 ton)

LME Spot (USD/ton)

Indian prices (INR ‘000/ton)

LME inventories (‘000 ton)

1,789

111

5,360

1,831

116

1,013

7,148

447

526

Note: Detailed table on pg 23

Source: MOSL

Valuations: Global companies

Price

Mining

BHP

AUD 35.1

FMG

AUD 4.8

Rio Tinto AUD 60.5

Vale

USD 31.9

Teck Res. USD 27.1

Steel

A. Mittal EUR 10.4

Posco k KRW 312.5

US Steel USD 21.5

Nucor

USD 48.8

JFE

JPY 2422

Gerdau

BRL 16.9

Bao Steel CNY 4.2

Non-ferrous

Alcoa

USD 8.0

Norsk Hyd. NOK 24.9

Rusal

HKD 2.4

Detailed on pg 23

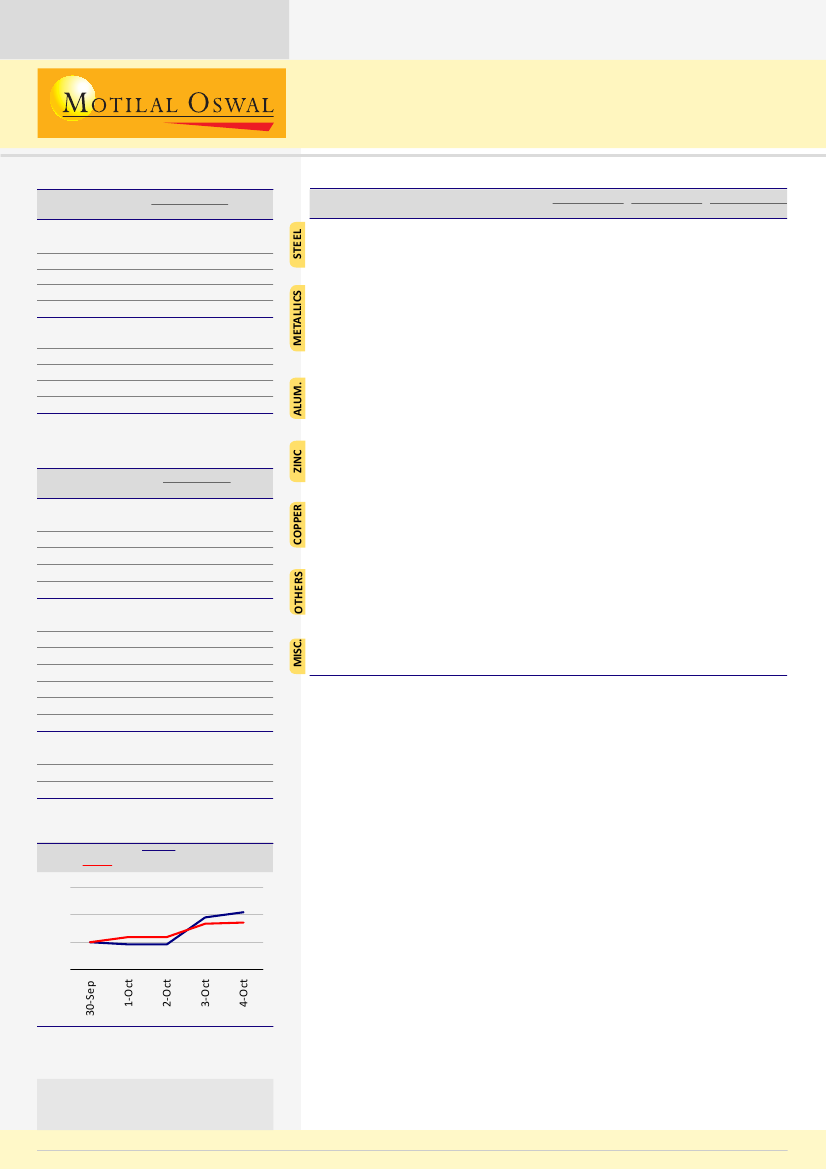

BSE Metals Index

Sensex

108

104

100

96

EV/EBITDA

CY13 CY14

6.4

4.4

6.5

5.0

6.8

6.5

5.4

8.6

12.2

7.5

9.2

6.8

6.0

4.2

5.9

5.0

6.3

5.5

4.9

5.5

7.6

6.7

7.3

6.1

P/BV

CY13

2.5

2.7

2.3

1.1

0.9

0.5

0.6

0.9

2.1

1.0

1.1

0.8

7,252

6

454 11

533 -21

30,186

48,800

2,083

1.01

Gold (INR/10gms)

29,728

Sliver (INR/1kg)

47,904

Lead Spot LME (USD/ton)

2,027

FC 6-8% C basis 60% Cr (USD/lb Cr) 1.01

INR/USD

BDI

15 25,778

19 40,408

-2 2,058

2

0.99

61.8 -1

62.5

4

59.6

13

54.5

2,084

4

2,003 78 1,171 129

910

Source: Metal Bulletin, Bloomberg, Steel Mint, MOSL

7.7

7.1

0.7

9.2

7.2

0.7

16.9 15.4

0.4

Source: Bloomberg

Indian Steel prices come off their recent highs; Global steel prices

marginally weak/flat

Indian long steel product prices e.g. TMT (Mumbai) declined 2% WoW to

BSE Metals Index v/s Sensex

INR34,600/t. Sponge iron prices were flat WoW at INR20,300, while Pellet

prices declined by INR50 to INR7,250/t.

Steel prices declined in CIS and Turkey by 1.4% and 2.4% WoW

respectively. Prices were flat WoW in Europe and N. America while

Chinese market was closed due to holiday.

Iron ore prices (63.5% Fe CFR China) decreased USD1/t WoW to

USD132/t, while Coking coal prices (Premium Low volatile, Fob Australia)

declined 3% WoW to USD149/t.

Base metals prices were weak with Copper, Lead and Zinc declining 1%,

Source: Bloomberg

Note: Indexed to 100 on 30 September 2013

Stock performance table on pg 24

Investors are advised to refer through

disclosures made at the end of the

Research Report.

3% and 3% WoW respectively. Aluminium prices were flat WoW.

Codelco will offer its European customers a premium of USD112/tonne

for copper cathode to be supplied in 2014 which is 32% higher than

Codelco's 2013 premium and USD7/tonne above Aurubis's offer for 2014.

Sanjay Jain

(SanjayJain@MotilalOswal.com); Tel:+91 22 3982 5412

7 October 2013

Pavas Pethia

(Pavas.Pethia@MotilalOswal.com); Tel:+91 22 3982 5413

1