28 October 2013

2QFY14 Results Update | Sector:

Automobiles

Maruti Suzuki

BSE SENSEX

20,570

Bloomberg

Equity Shares (m)

M.Cap. (INR b) / (USD b)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

Financials & Valuation (INR b)

Y/E MAR

Sales

EBITDA

Adj. PAT

Con.adj.EPS

EPS Gr (%)

BV/Sh (INR)

RoE (%)

RoCE (%)

Con.P/E (x)

P/CE (x)

2013

435.9

42.3

23.9

80.2

37.8

615.0

12.9

15.5

18.9

10.7

2014E

439.6

52.4

28.7

96.3

20.1

697.2

13.6

17.4

15.7

9.1

2015E

504.0

59.1

32.6

108.0

12.1

791.2

13.6

17.3

14.0

8.0

S&P CNX

6,101

MSIL IN

302.1

457/7.4

1,773/1,217

6/-15/0

CMP: INR1,513

TP: INR1,702

Buy

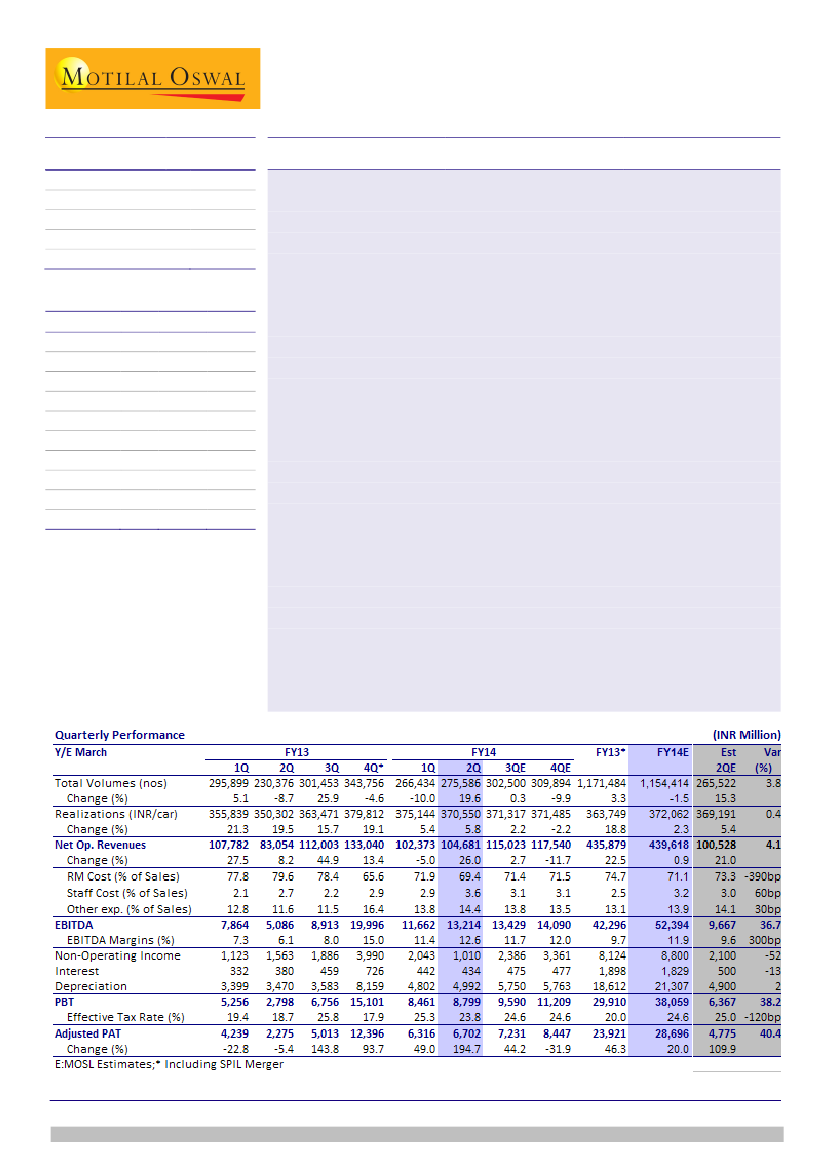

Above est with EBITDA margin at 12.6%; upgrade FY14E EPS by 22%

Current quarter’s performance is not comparable YoY due to merger of SPIL in

4QFY13. MSIL’s 2QFY14 performance was above estimates, with EBITDA margins

of 12.6% (up 120bp QoQ, est 9.7%) driven by favorable forex. Led by higher-than-

estimated EBITDA, PAT stood at INR6.7b (est. INR4.8b).

Earnings call highlights

RM cost fell 260bp QoQ led by 100bp favorable forex on vendors’ import

(quarter lag), higher export revenue (INR depreciation) and low cost inventory

of direct imports (timing mismatch, to reverse in 3Q).

Diesel share stood at 30% (v/s 34% in 1Q). Average discounts increased

sequentially by INR4,000 to INR17,500/unit in 2Q.

Festive sales so far have risen by 5-8%; seasonally, 2H expected to be better

by 10%. Rural grew by 24% during 1HFY14, contributing 31% to MSIL sales.

JPY/USD direct and indirect exposure fully hedged for 3Q and partially hedged

for direct exposure for 4Q. Royalty (payable in May-14) remains unhedged.

USD/INR exposure hedged for 3Q.

Import content to reduce 2-2.5% annually from 19.5% in Mar-13. Depending

on component/technology, ~10-20% cost savings can be expected.

Valuation and view

We upgrade FY14E/FY15E EPS by 22%/7% to ~INR96/108 respectively to

factor a) strong 2QFY14 performance, b) 2HFY14 fx hedges and c) benefit of

cost saving initiatives. We assume volume growth of -1.5%/12.8%, EBITDA of

11.9%/11.7% and JPY/INR of 0.617/0.625 in FY14E/FY15E.

The stock trades at 15.7x/14x FY14E/15E consol. EPS and 9.1x/8x FY14E/15E

cash EPS. Maintain

Buy

with a revised target price of INR1,702 (~9x FY15E

CEPS/16x FY15E con. EPS).

Jinesh Gandhi

(Jinesh@MotilalOswal.com); +91 22 3982 5416

Chirag Jain

(Chirag.Jain@MotilalOswal.com); +91 22 3982 5418

Investors are advised to refer through disclosures made at the end of the Research Report.