9 May 2014

5QFY14 Results Update | Sector: Healthcare

Ranbaxy Labs

BSE SENSEX

22,994

Bloomberg

Equity Shares (m)

52-Week Range (INR)

1, 6, 12 Rel.Per (%)

S&P CNX

6,859

RBXY IN

422.9

505/254

-2/-1/-10

CMP: INR464

TP: INR580

Buy

M.Cap. (INR b) / (USD b) 197.1/3.3

Financials & Valuation (INR Billion)

Y/E MAR

Sales*

EBITDA*

Adj. PAT

Rep. EPS

Adj. EPS

EPS Gr. (%)

BV/Sh(INR)

RoE (%)

RoCE (%)

Payout (%)

Valuations

P/E (x)

P/BV (x)

EV/EBITDA

Div.Yld (%)

2014

133.8

10.9

3.9

-24.9

9.3

-53.8

69.2

-35.9

9.6

25.1

44.9

6.0

23.0

0.5

2015E 2016E

133.5 130.4

24.5

15.7

3.5

7.8

34.4

18.5

8.3

18.5

-11.3 123.7

97.7 110.5

35.2

16.7

22.8

12.8

70.8

31.6

50.6

4.3

18.8

1.2

22.6

3.8

13.9

1.2

*Estimates include upside from FTF

opportunities; FY14E figures are 15

months

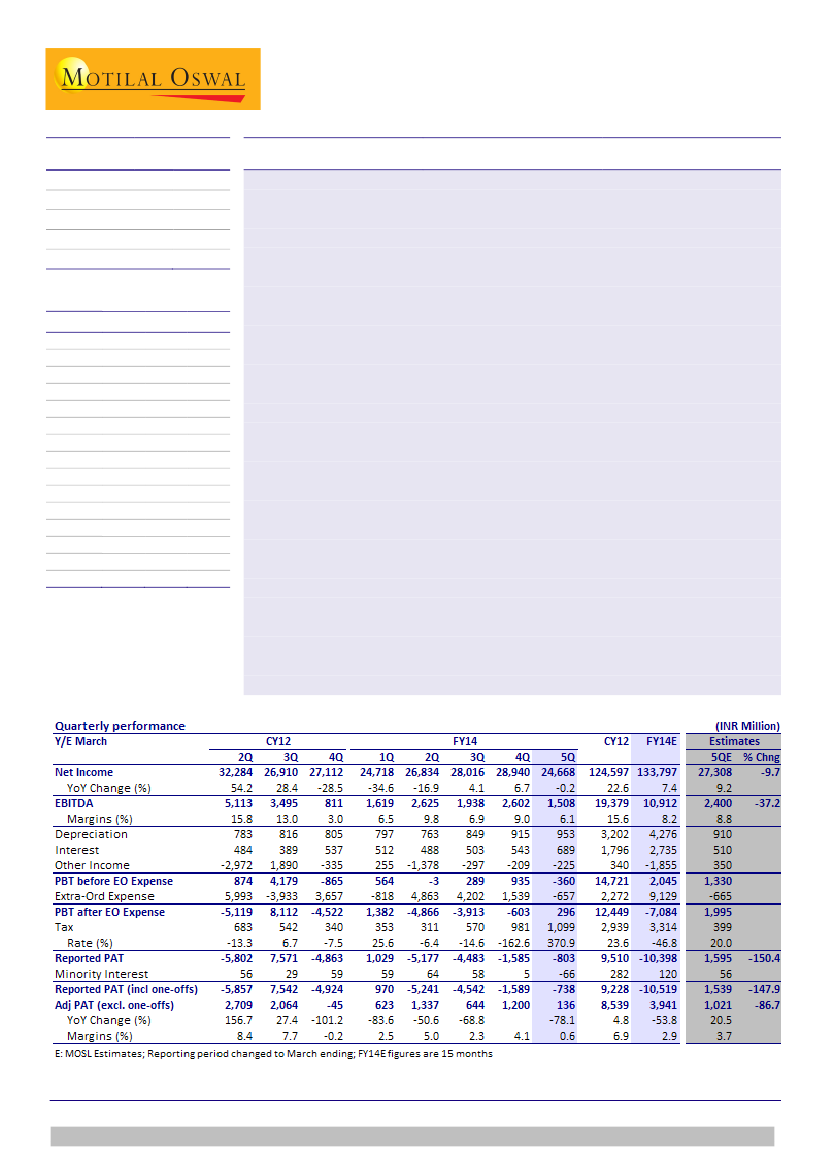

Ranbaxy's (RBXY) 5QFY14 results were below estimates. Revenue was flat YoY at

INR24.7b (v/s est. INR27.3b), while EBITDA declined 7% YoY to INR1.5b (v/s est.

INR2.4b), with EBITDA margin at 6.1% (v/s est. 8.8%). Reported loss stood at

INR738m (v/s est. PAT of INR1.5b).

Revenue growth was impacted by lower-than-expected performance across key

geographies of the US, India OTC, CIS, APAC and Africa. Pertinently, there was a

69% decline in APIs business which in turn was impacted by discontinuation of

Dewas and Taonsa operations.

EBITDA margin fell 40bp YoY, impacted by higher fixed overheads and remediation

costs incurred despite the slowdown in sales.

RBXY has reported exceptional items of INR903m towards inventory write-off on

Taonsa ban, goodwill impairment and diminution of value in a subsidiary.

Adjusted for one-off items and forex impact, company reported PAT of INR136m

(v/s est. INR1b), compared to PAT of INR623m in the corresponding quarter.

Key concall takeaways:

RBXY has refrained from giving guidance for FY15 and will

share it in subsequent quarters. Merger with SUNP will need approval of 75%

majority of total shareholders. Post which Sebi will approve the deal. Existing

business is showing healthy underlying growth across key geographies and is

expected to recover, going forward.

Post 5QFY14 results, we have lowered FY15E/16E core EPS estimates by 6%/2% to

reflect lower base business profitability. Over FY14-19E, we build core margin

expansion of 780bp to 18% based on synergy benefits highlighted by SUNP. This

assumes sales CAGR of 12% over the same period. We get a DCF value of INR559

for core business of RBXY. We add to this INR21/share from Para IVs which gives

us an SOTP-based target price of INR580. We maintain

Buy.

Key risks to our

arguments are integration challenges faced by SUNP and prolonged issues with

the US FDA.

Alok Dalal(Alok.Dalal@MotilalOswal.com);+91

22 3982 5584

Hardick Bora(Hardick.Bora@MotilalOswal.com);+91

22 3982 5423

Investors are advised to refer through disclosures made at the end of the Research Report.