20 May 2014

4QFY14 Results Update | Sector:

Oil & Gas

MRPL

BSE SENSEX

24,377

Bloomberg

Equity Shares (m)

M.Cap. (INR b) / (USD b)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

S&P CNX

7,276

MRPL IN

1,752.6

119.2/2.0

69/26

22/42/26

CMP: INR68

TP: INR72

Neutral

Financial & Valuations (INR b)

2014 2015E

Y/E MAR

Sales

EBITDA

Adj. PAT

Adj. EPS (INR)

EPS Gr. (%)

BV/Sh.(INR)

RoE (%)

RoCE (%)

Payout (%)

Valuation

P/E (x)

P/BV (x)

EV/EBITDA (x)

Div. Yield (%)

718.1

10.0

6.0

3.4

-175.0

40

8.9

4.4

0.0

19.7

1.7

9.9

0.0

755.3

29.1

10.4

5.9

72.4

45

13.9

13.9

23.7

11.4

1.5

6.3

1.8

2016E

784.6

34.9

13.6

7.8

31.3

51

16.3

18.8

24.1

8.7

1.3

5.0

2.4

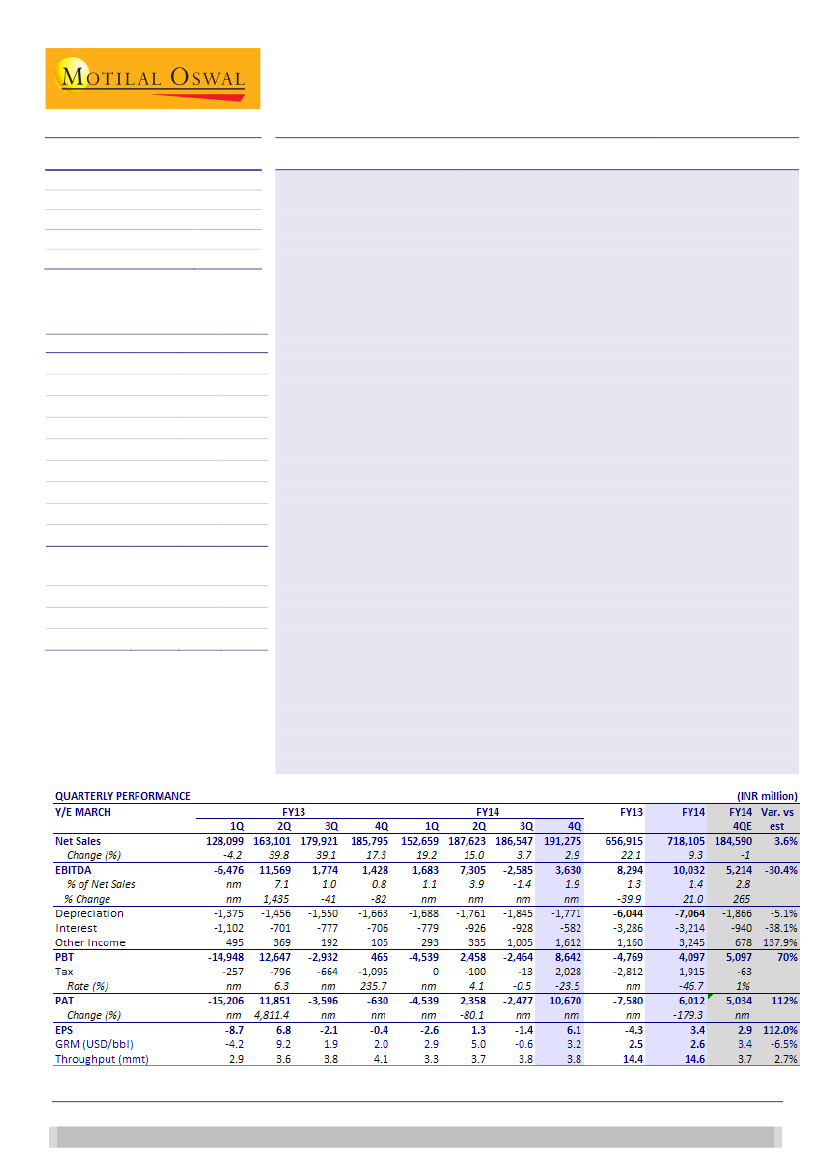

MRPL’s reported 4QFY14 EBITDA at INR3.6b (est INR5.2b) was below estimate led

by GRM of USD3.2/bbl (est USD3.4/bbl) and higher opex of USD1.1/bbl (est of

USD0.9/bbl). However, PAT was above estimate at INR10.7b (est INR5.0b) led by

(a) higher other income of INR1.6b (led by cash held for Iran’s prior period crude

purchases), (b) forex gain of INR5.75b and (c) INR2.8b gain from deferred tax

asset recognition.

GRM at USD3.2/bbl compared to Singapore GRM of USD6.2/bbl:

MRPL

reported GRM at USD3.2/bbl (v/s 4QFY13 GRM of USD2.0/bbl and USD-0.6/bbl

in 3QFY14) was lower than our estimate of USD3.4/bbl. Throughput for the

quarter was marginally above estimates at 3.84mmt (est. of 3.74mmt)

MRPL’s Phase III project (INR150b) progress stands at 99.68% v/s 99.5% as on

Jan 15, 2014. (a) DCU (Delayed Coker Unit) has been commissioned and has

started production, and (b) PFCCU (Petro Fluidised Catalytic Cracking unit) is

expected to be completed during 1HFY15 (v/s earlier expectation of 4QFY14).

Due to complexity in payment towards crude purchase from Iran, MRPL is yet to

make payments for prior period crude purchases. As on March 31, 2014, of its

balance sheet cash of INR107b; ~INR80b is towards payable for Iran crude.

Polypropylene project progress is 95.6% v/s 93.4% in 3QFY14, and

commissioning is expected by 2QFY15 (v/s earlier estimate of 1QFY15).

We believe, post commencement of full operations, the benefit of the project

and increased refinery complexity will be seen from 2HFY15.

GRM outlook rangebound:

While the near term GRM’s are expected to remain

range-bound, medium term outlook remains subdued due to refinery capacity

additions exceeding oil demand growth. We expect GRMs to be volatile

(occasional spurts) due to occasional bunching up of shutdowns.

Valuation and view

MRPL being a standalone refiner is highly sensitive to GRM. For variation of

USD1/bbl in GRM, FY14 EPS changes ~25%. The stock trades at FY16E P/E of

8.7x and EV/EBITDA of 5x.

Neutral.

Harshad Borawake

(HarshadBorawake@MotilalOswal.com); +91 22 3982 5432

Nitish Rathi

(Nitish.Rathi@MotilalOswal.com); +91 22 3982 5558

Investors are advised to refer through disclosures made at the end of the Research Report.