23 May 2014

4QFY14 Results Update | Sector:

Consumer

ITC

BSE SENSEX

24,693

Bloomberg

Equity Shares (m)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

S&P CNX

7,367

ITC IN

7,953.2

387/285

-11/-11/-23

CMP: INR342

TP: INR400

Buy

M.Cap.(INR b)/(USD b) 2,721.2/46.6

Financials & Valuations (INR b)

Y/E MAR

Net Sales

EBITDA

Adj PAT

AdjEPS(INR)

Gr. (%)

BV/Sh (INR)

RoE (%)

RoCE (%)

P/E (x)

P/BV (x)

2014 2015E 2016E

328.8

123.0

86.5

11.1

16.6

28.9

38.8

53.4

30.9

11.8

377.1

141.3

100.7

12.9

16.4

31.7

40.6

57.0

26.6

10.8

432.5

161.4

115.8

14.8

15.0

34.4

43.0

60.7

23.1

9.9

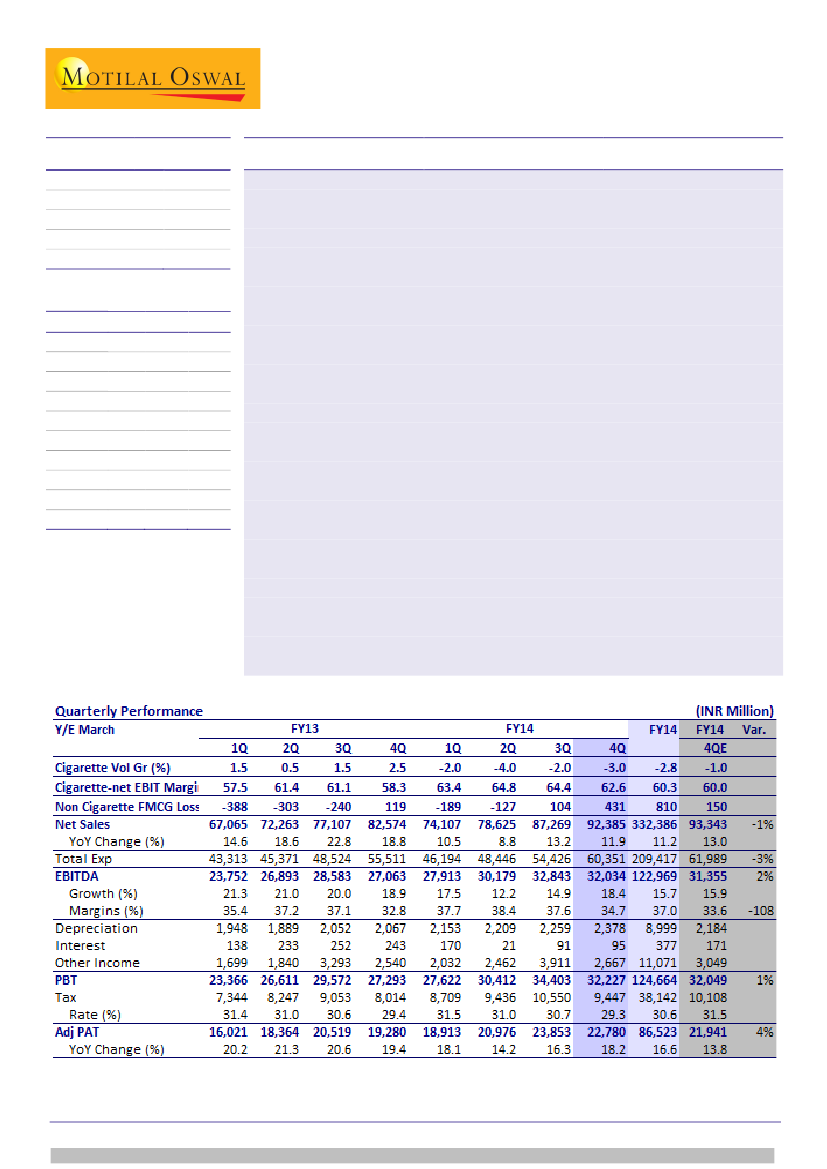

ITC’s 4QFY14 performance was tad ahead of our expectations with 4% beat on

PAT. Revenues grew 11.9% to INR 92.4b (est INR 93.4b); EBITDA grew 18.4% YoY

to INR32.0b (est. INR 31.3b), while Adj. PAT grew 18.2% to INR 22.8b (est.

INR21.9b).

Cig volumes declined ~3% while Cigarette EBIT grew robust 21% and posted

280bps margin expansion to 34.3% (13th consecutive quarter of margin exp).

64mm portfolio continues to perform well and now crossed 10% salience.

EBITDA margins expanded 190bp to 34.7% (est. 33.6%) led by 280bp expansion in

Cigarettes, 130bp in FMCG – Others, 580bp in Hotels, 40bp in Agri.

Non-Cig FMCG posted 13.7% sales growth (lowest since 1Q10) due to high base

(26% growth in base) and overall consumption slowdown. Segment EBIT went up

3.6x YoY and posted higher ever EBIT of INR431m. On a full year basis, ITC

reported EBIT of INR 218m, maiden annual profit.

Agri revenues grew 8.1% driven by leaf tobacco exports while margins expanded

40bp. Hotels continued to suffer from weak macros – 1.6% revenue growth, but

material ebit margin expansion of 580bps led by Chennai property. Paper segment

revenue grew 19.3% while EBIT remained flat (290bps margin decline) due to cost

inflation in Wood pulp.

Continued robust Cig EBIT growth and margin expansion coupled with positive

segment EBIT in non-Cig FMCG are the key highlights of the quarter. Within our

overall cautious stance on the sector, we believe ITC offers best risk reward

profile given the earnings visibility. ITC closed FY14 with profit growth of healthy

16.6%. Recovery in Cig volumes remain key concern. Excise duty changes in the

forthcoming budget will be near term trigger for the stock. Maintain our top

sector pick and reiterate

Buy

with a 12 month forward TP of INR 400 (27x FY16E

EPS), an upside of 17%.

Gautam Duggad

(Gautam.Duggad@MotilalOswal.com); +91 22 3982 5404

Manish Poddar

(Manish.Poddar@MotilalOswal.com); +91 22 3027 8029

Investors are advised to refer through disclosures made at the end of the Research Report.