Wednesday, June 11, 2014

Market Overview (Economy)

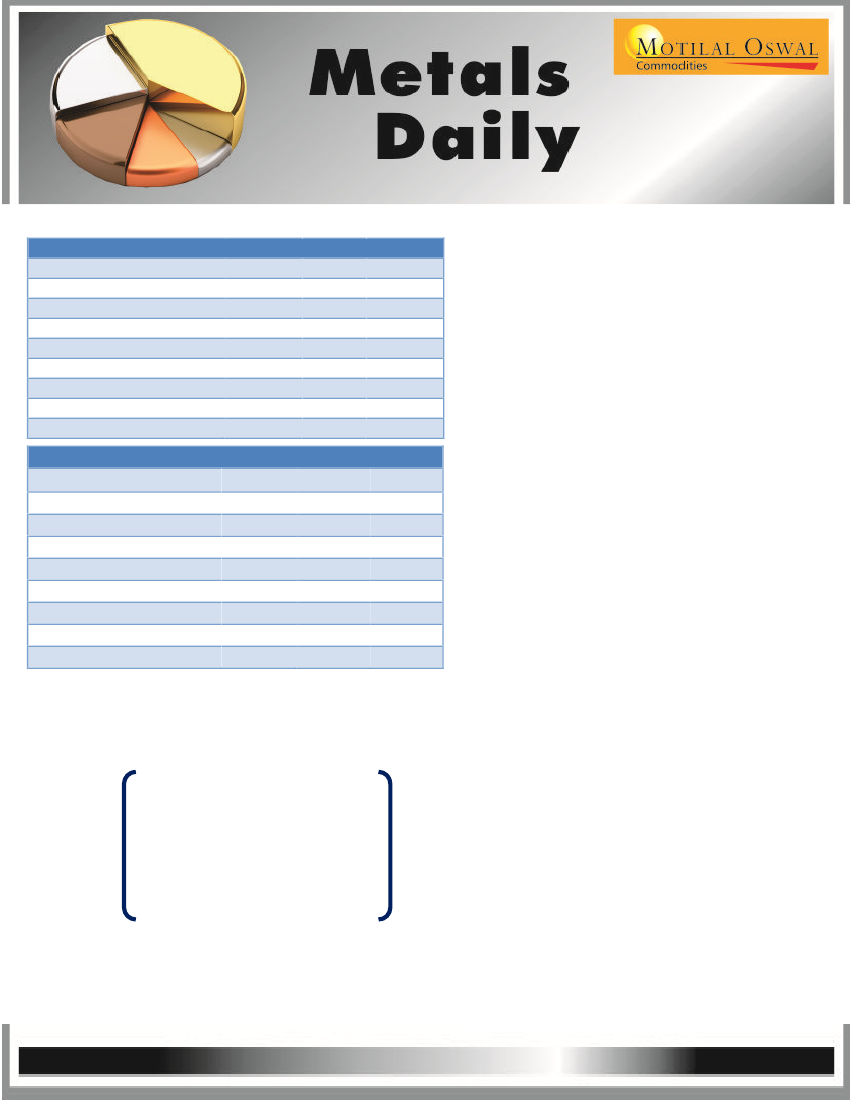

Commodity

Gold / USD Spot

Silver / USD Spot

Crude oil $ Spot

COMEX Copper $

LME Copper (3M)

LME Aluminum (3M)

LME Nickel (3M)

LME Lead (3M)

LME Zinc (3M)

Last

1260.49

19.12

105.02

343.5

6705

1900.75

18644

2147.25

2141.25

Chg

8.91

0.1

-0.07

-1.9

8

4.75

-56

5.25

8.25

% Chg

0.71%

0.53%

-0.07%

-0.55%

0.12%

0.25%

-0.30%

0.25%

0.39%

Asian markets are mixed in early trade

and consolidating recent gains even as

the euro is under increasing pressure on

expectations of more easing measures.

Overall, positive US data is supporting

the dollar strength across the board

which might weigh on commodities.

Looking ahead, the main focus of the

markets will be the FOMC meet next

week which will give hints about the Fed’s

interest rate policy going ahead.

Equity

BSE Sensex Index

S&P CNX NIFTY

Hang Seng Index

Shanghai Index

Nikkei 225 Index

DAX Index

CAC 40 Index

Dow Jones

NASDAQ 100 Index

Last

25583.7

7656.4

23315.7

2052.5

14994.8

10028.8

4595.0

16945.9

3800.9

Chg

3.5

1.8

198.3

22.0

-129.2

20.2

5.9

2.8

5.1

% Chg

0.01%

0.02%

0.86%

1.08%

-0.85%

0.20%

0.13%

0.02%

0.13%

Precious Metals

Precious metals are trading flat but signs

of a more accommodative stance from the

ECB may underpin prices in the short

term.

There have been no economic triggers

this week and the focus will be the Fed

meet in the next week which will provide

direction to precious metals.

In supply side data, Russian gold

production rose by 29.7% in the first four

months of 2014 compared with the same

period a year earlier.

MCX Gold (Aug contract) achieved our

expected level of Rs.26170 and closed

near the same. Price at present is in a

pullback mode and as long as sustains

above Rs.26000, bias remains sideways

to positive.

Silver is also in a pullback mode and is

trading close to the crucial resistance near

Rs.40650 level. Rise above the same

could target Rs.41050 level on the upside.

There have been no economic triggers this

week and the focus will be the Fed meet in

the next week which will provide direction

to precious metals.

1

Please refer to disclaimer at the end of the report.