25 Oct 2012

Update |Sector: Utilities

CESC

CMP: INR

Acquisition of stake in Firstsource at INR4b for 49.5% stake,

Unrelated diversification – a cause of concern

-

CESC announced acquisition of minimum 49.5% stake in Firstsource (FSL) for

INR4b through its wholly owned subsidiary Spen Liq. This comprises of a 34.5%

stake acquired through fresh issue of shares by FSL and 15% through acquisition

from existing investors. It would also make a buyback offer to acquire 26% of

paid up capital at INR12.2/sh. Management believes that as 2/3rd of the holding

is with CESC group (49.5%) and existing investors (23% post offering), and

hangover of FCCB repayment/divestment of stake by existing investors are

behind, tendering in open offer would be limited. CESC is determined to hike

stake to at least 51% to allow full consolidation.

Funding for the same is through leveraged buy-out and would be met through

debt of 70% (INR2.8b) and 30% equity (INR1.2b). Given FSL’s profitability track

record, management perceives the investment to yield “favorable returns”,

while also provides “potential new growth business segment”. For FY13E,

management expects PAT accretion of INR750m (going by earlier PAT range of

INR1.5b, while FY12 PAT was INR620m) from FSL, which net off acquisition

interest of INR200m would be INR500-550m, on equity investment of INR1.2b.

Management is determined to stay with business and grow it.

FSL will use cash infusion, along with INR7.6b cash on books to repay INR13b

FCCB, due for repayment in Dec-12. FSL’s FY12 balance sheet is bit discomforting

given higher goodwill of INR24b on net worth of INR14b. Total debt on books is

also higher at INR21b, while cash is INR7.6b.

In our view, while CESC does not have any major cash flow crunch despite its

commitment to power projects (INR10b), Spencer (INR 3b), regulated business

(INR4b), given cash of INR13b and recurring cashflow from regulated business

(INR5b+ pa), unrelated diversification is a cause of concern. BUY.

-

-

-

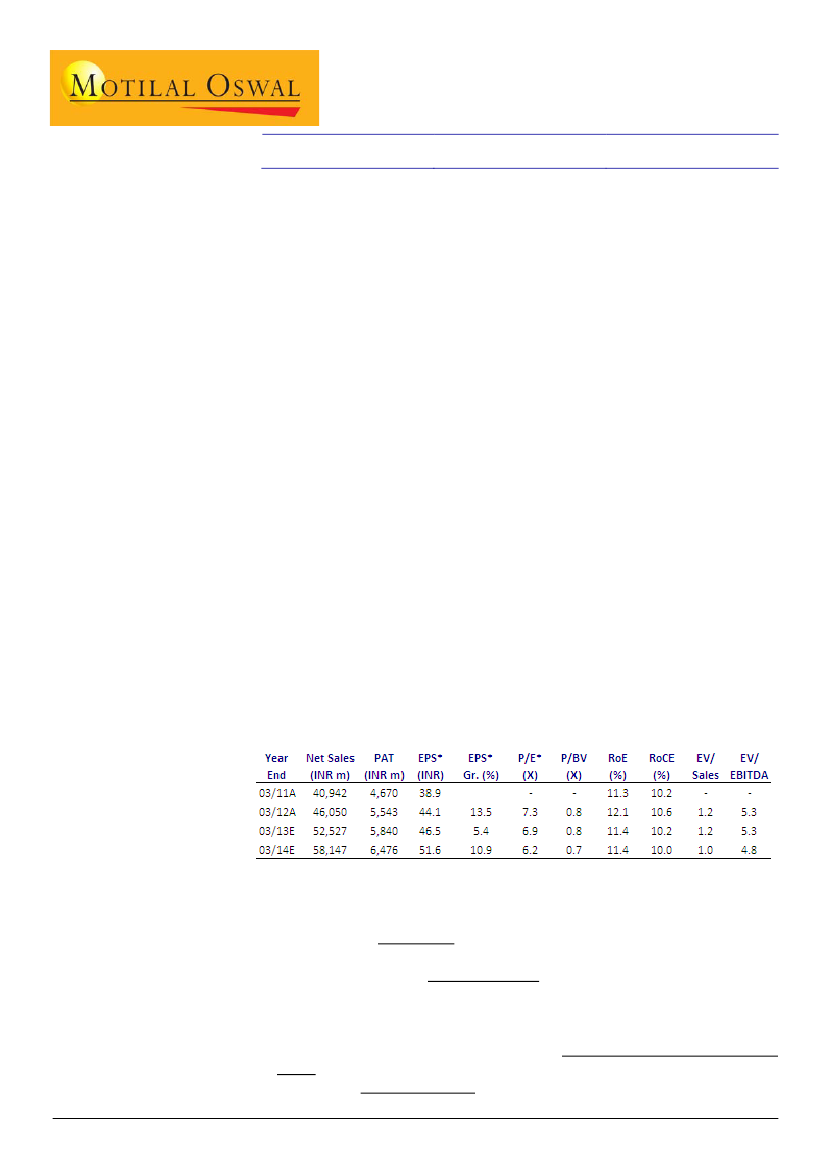

Financial summary

* Excl Spencers; fully diluted

Details of transaction

- CESC’s (CESC IN, Mkt Cap US$0.8b, CMP INR332/sh, BUY) 100% subsidiary, Spen

Liq, will acquire

34.5% stake

in Firstsource Limited (FSL) through a fresh issue of

shares by the company. This amounts to issue of 227m shares at a price of

INR12.1/sh, an outgo of

INR2.7b for CESC.

- Secondly, existing share holder’s stake would be reduced to the extent , viz. ICICI

Group stake would be 13% vs 19.9% earlier, Aranda Investement (Temasek

entity) stake at 12.3% vs 18.8% stake now and Metavante Investment stake at

11.9%, vs 18.2% stake now. CESC will buy

5% stake from each entity (15%

stake),

entailing 98.7m shares of the expanded capital of FSL at price of

INR12.2/sh –

an outgo INR1.2b.

1