17 Sep 2012

Update |Sector: Technology

Infosys

BUY

CMP: INR2631

TP: INR 2815

No comeback in discretionary and BFSI spends; Pricing pressure

in pockets of BFSI continues; Confident of meeting FY13

guidance

We interacted with the management at Infosys (INFO IN, CMP INR2631, MCAP USD

28b, Buy) to get an insight on 2QFY13 and the overall demand environment. Key

takeaways:

- There has been no change in the environment in the last couple of months; the

company is not seeing any turnaround in troubled areas, especially discretionary

spends and BFSI. The component of budget under-spends thus far in the

calendar year is high.

- It is not expecting budget flush towards the end of the CY12, so growth may be

evenly spread across quarters. With wage hikes absent, and utilization moving

within a tight band across quarters, margins are expected to be stable, rather

than witness quarterly seasonality. Expect pricing decline on the back of some

more price cuts in troubled pockets in BFSI and residual impact of cuts in

1QFY13. But reported realization may not see a significant change as base of

USD15m revenue reversal in 1Q will push the realization metric up.

- The company continues to actively scout for acquisitions in the Products,

Platforms and Services segment (PPS). After Lodestone, Consulting may not see

an acquisition any time soon. The Board believes 30% payout ratio is optimal

given inorganic growth plans.

- Infosys reiterated its focus on Business Operations segment, stating that if it

qualified a deal as important, it will be flexible and aggressive on pricing in

chasing the same. However, peer-matching / leading growth rates remain a

function of resurgence in discretionary spends.

Valuation and View: Near-term triggers missing, but reassurance in meeting the

guidance limits downside

- Given continued cautiousness in its outlook, upside in the stock could be

restricted in the near term, despite increasing confidence and visibility in

meeting 5% FY13 USD revenue growth guidance. We expect pricing concerns to

be behind the company post 2QFY13, and greater aggression should help deliver

on a non-worrying volume growth guidance.

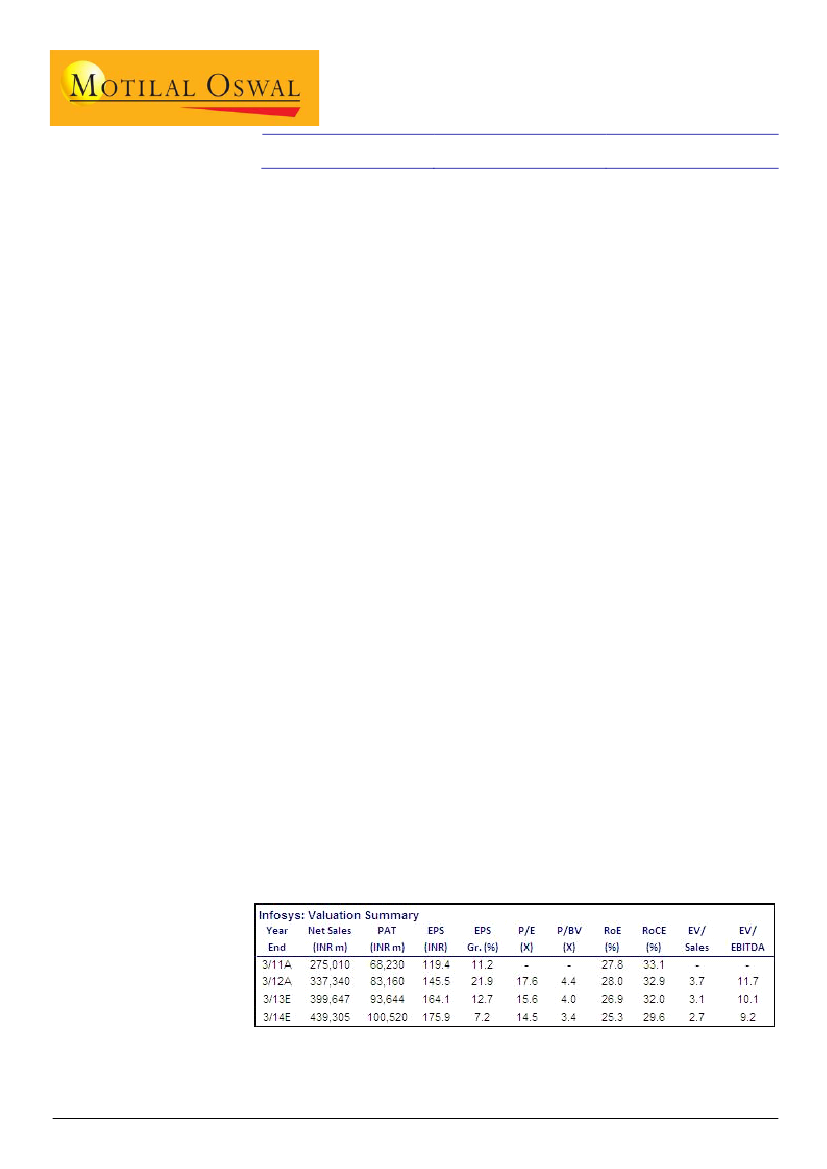

- We expect Infosys’ USD revenues CAGR of 10% over FY12-14 and EPS CAGR of

12%. The stock trades at 15.6x FY13E and 14.5x FY14E. Maintain

Buy,

with a

target price of INR2,815.

1