29 July 2014

1QFY15 Results Update | Sector:

Consumer

ITC

BSE SENSEX

25,991

Bloomberg

Equity Shares (m)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

S&P CNX

7,749

ITC IN

7,818.4

387/285

8/-17/-35

CMP: INR357

TP: INR400

Buy

M.Cap. (INR b)/(USD b) 2,789/46.4

Financials & Valuation (INR Billion)

Y/E MAR

Sales

EBITDA

Adj. PAT

Adj. EPS (INR)

EPS Gr. (%)

BV/Sh.(INR)

RoE (%)

RoCE (%)

P/E (x)

P/BV (x)

2015E 2016E 2017E

374.1 429.1 489.5

141.2 162.9 187.0

100.7 116.8 134.5

12.9

16.3

31.7

40.6

57.0

27.7

11.2

14.9

16.1

34.4

43.4

61.2

23.9

10.4

17.2

15.1

37.5

45.8

64.9

20.7

9.5

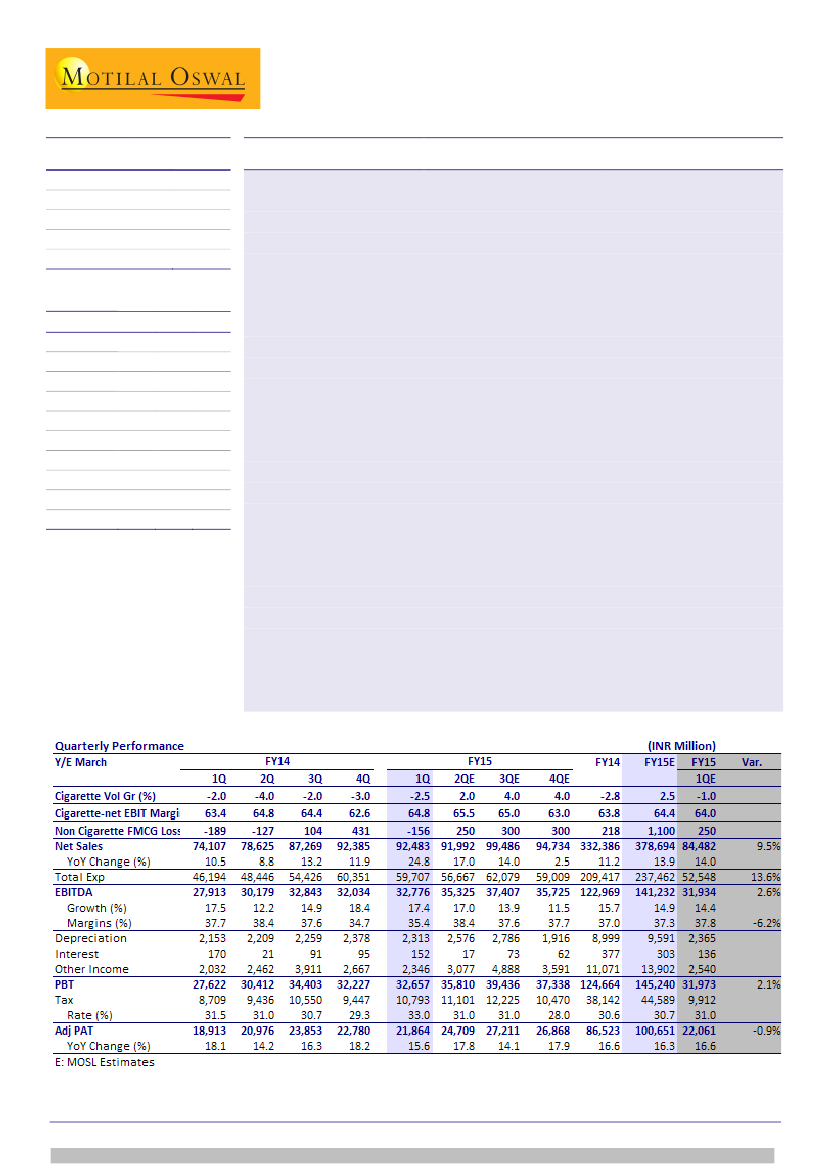

ITC’s 1QFY15 results were largely in-line though seasonality in Agri revenues

resulted in 9.5% beat on sales vs. our estimates. 1Q15 net sales, EBITDA and PAT

came in at INR92.5b (est. INR84.5b), INR32.8b (est. INR31.9b) and INR21.9b (est.

INR 22b), up 24.9%, 17.4% and 15.6%, respectively.

Cig volumes declined 2.5% with net sales growth of 18.8% to INR42b while Cig

EBIT grew robust 21.4% and posted 140bp net EBIT margin expansion to 64.8%.

ITC has discontinued sharing gross sales figures from this quarter.

EBITDA grew 17.4% to INR 32.8b; margins contracted 220bps to 35.4 due to mix

deterioration post higher growth in Agri sales and EBIT losses in Hotels division

due to higher depreciation expenses on revision of useful life.

Non-Cig FMCG posted 10.9% sales growth (lowest since 1QFY10) with mid single

digit volume growth; impacted by weak macros with moderation in Biscuits and

Noodles category (high single digit growth vs. high teens earlier). Lifestyle and

matches business have also witnessed sharp moderation. The segment reported a

loss of INR156m.

Agri revenues grew 50.6% YoY to INR32.9b on account of higher trading in non-

leaf tobacco portfolio. Leaf tobacco sales were impacted due to change in order

pattern and margins contracted 300bp due to mix deterioration. Hotels

continued to suffer with lower occupancies (shift in IPL out of India in 2014) and

lower beverage sales during elections and posted 0.5% revenue decline with

sharp 840bps EBIT margin contraction. Paper revenues grew 10.8% YoY to

INR12.8b with 30bp margin contraction to 21.3%.

Continued robust Cig EBIT growth and margin expansion are the key highlights of

the quarter. Given the unprecedented third consecutive year of ~20% excise hike

in cigarettes, we expect delayed volume recovery in Cig. Reiterate

Buy

with a

Target Price of INR400 (27x FY16E).

Gautam Duggad

(Gautam.Duggad@MotilalOswal.com); +91 22 3982 5404

Manish Poddar

(Manish.Poddar@MotilalOswal.com); +91 22 3027 8029

Investors are advised to refer through disclosures made at the end of the Research Report.