January 1st , 2015

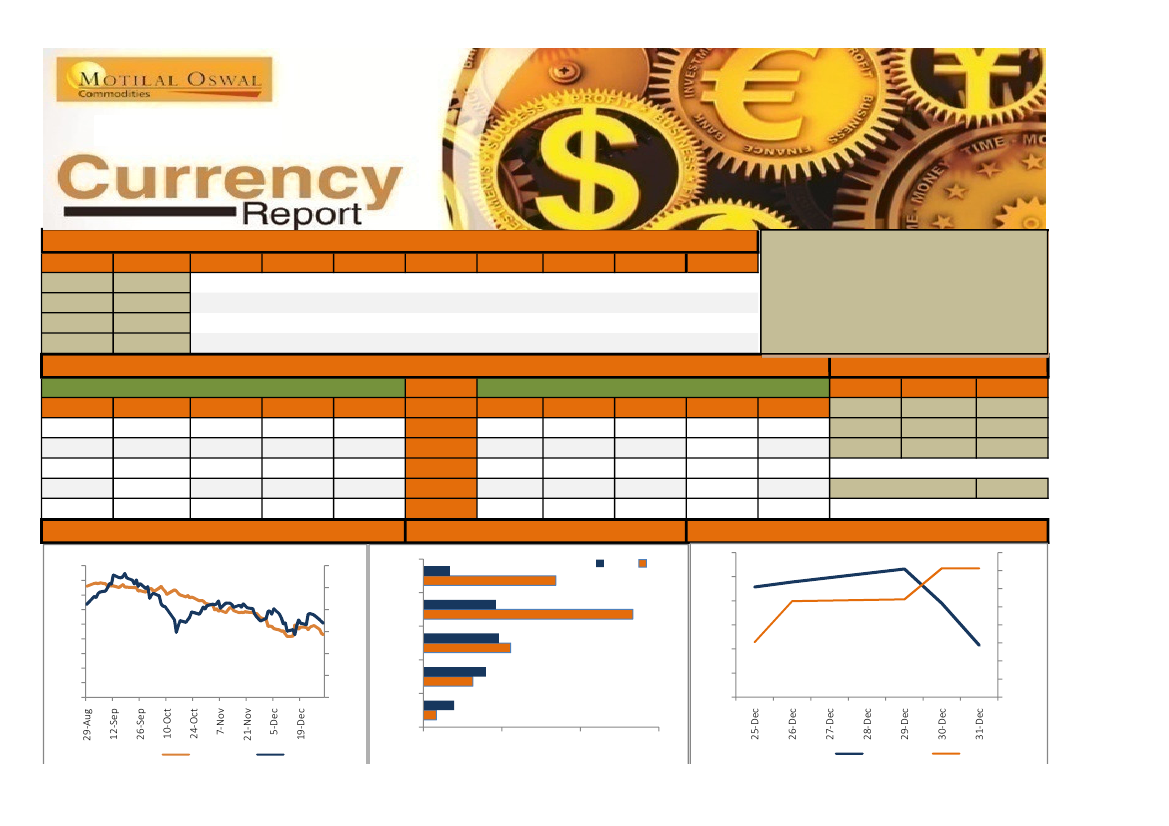

Currency Futures (NSE)

Currency

USDINR

EURINR

GBPINR

JPYINR

Expiry

January

January

January

January

Spot

63.0300

76.2410

98.1940

52.6600

Call

OI

16706

63120

111222

266819

168722

Open

63.6900

77.4650

99.0100

53.3550

High

63.7400

77.5150

99.2125

53.4550

Low

63.4250

77.0600

98.8125

53.0900

Strike Price

Close

63.4675

77.1300

98.9550

53.1925

% chg

-0.43%

-0.46%

0.01%

-0.16%

Trade Sheet:

OI

% Chg in OI

Sell 63.5 PE & 64.5 CE (JAN) at 0.53, SL

1339257

-1.3%

0.70, TGT 0.10

41157

2.4%

Sell 64.5 Call at 0.22, Sl 0.33, TGT 0.01

27300

-11.4%

Sell GBPINR at 99.16, SL 99.48, TGT 98.15

13065

Put

OI

39309

79792

96481

92334

33853

11.0%

Option Monitor

IV

5.99

5.56

5.68

6.16

6.67

% Chg in OI

1.15%

40.92%

20.54%

-4.21%

-0.59%

Volume

1063

28566

91075

123508

61178

Premium

1.0225

0.6300

0.3575

0.2025

0.1150

Premium

0.0825

0.2025

0.4300

0.7525

1.1850

Volume

16115

63743

82444

34487

1493

% Chg in OI

4.87%

6.02%

-6.65%

-6.44%

-1.15%

63.8

63.6

63.4

63.2

63.50

63.00

62.50

India

US (RHS)

FII Activity

IV

5.42

5.40

5.58

5.71

6.58

Action

BUY

SELL

NET

Days to Expriy

Rs. (Crs)

2348.86

1867.78

481.08

$ (Mil)

367.38

292.14

75.25

27

62.50

63.00

63.50

64.00

64.50

10 Yr Bonds Yields

8.8

8.6

8.4

8.2

8

7.8

7.6

7.4

7.2

7

2.7

2.5

2.3

2.1

1.9

1.7

1.5

64.50

64.00

Open Interest Distribution

Put

Call

Correlation Between Nifty v/s USDINR

8300

8280

8260

8240

8220

8200

8180

8160

8140

63

62.8

62.6

Source: Reuters

0

100000

200000

300000

Source: Reuters

USDINR

Nifty (RHS)