WEEK IN A NUTSHELL

WIN-dow to the week that was

Week in a Nutshell (WIN)

Week

ended

th

16 Jan

2015

Key WIN-dicators

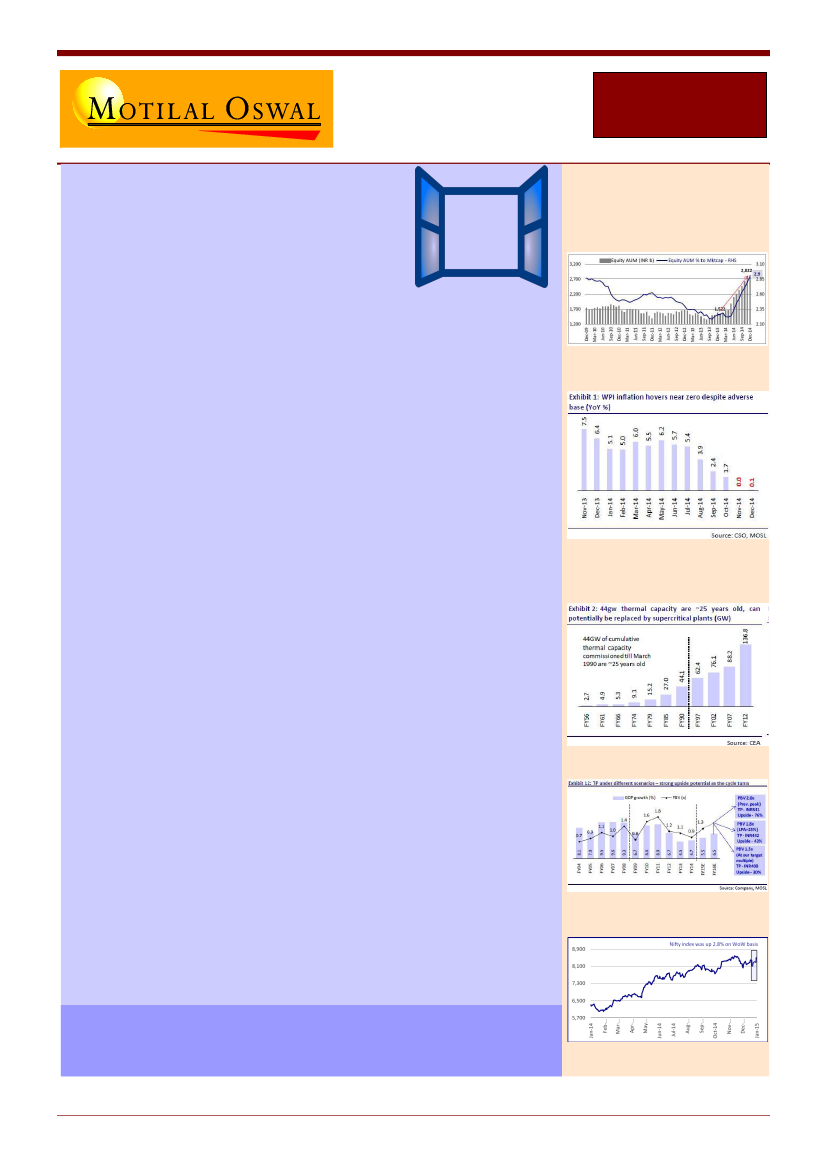

Trend in Domestic MF equity AUM

and % of Indian market cap

WPI inflation announced at the beginning of the week prompted RBI to

cut REPO rate by 25 bps between policy reviews, The markets rejoiced the

unexpected move and ended up 2.8% for the week, this was the highest

weekly gain by Nifty since October. Realty was the biggest gainer of the

week posting returns of 5.7%. But surprisingly FMCG sector (up 4.1%)

outperformed the banks index (up 3.2%), this outperformance was on

back of HUVR which gained another 27% for the week on back of slew of

analyst upgrades. Oil and Gas (down 0.9%) and Metals (down 4.1%) were

the only two sectoral indices to close in the red for the week on back of

sliding commodity prices.

After a stellar set of numbers posted by INFO, TCS was not able to stand up

to market expectations. TCS’s 3Q numbers came in as a disappointment for

the market on back of its lower than expected CC revenue growth of 40

bps.

Private banks (AXSB and YES) continued to post decent set of number

backed by stable asset quality and growth. Markets also drew comfort from

the trade deficit number announced during the week. Year till Jan FY15

Trade deficit stood at 5.2% of GDP Vs 7.4% for FY14.

Bajaj Auto reported their highest-ever EBITDA despite weakening domestic

market share. The companies focus on profitability and global markets

gives us confidence in Bajaj Auto. Trading at a reasonable 16x FY16, we

remain positive on the stock.

Markets got a bit shaken up post the large appreciation the CHF saw post

the move by SCB, but strong FII inflows made sure that Nifty outperformed

most of the global equity indices for the week.

Some of the highlights of this edition:

ECOSCOPE: RATE CUT CYCLE BEGINS

3QFY15 results – TCS, IIB, Bajaj Auto

Detailed reports – SBI, BHEL, L&T

WPI Inflation near

adverse base (YoY %)

zero

despite

44GW Thermal capacity are ~25 years

old, can potentially be replaced by

supercritical plants (GW)

SBI target price under 3 scenarios

Nifty (2.8%) WoW

WWW – WIN Weekend Wisdom

The stock market will always do whatever makes the greatest number

of people look foolish.

Read

WIN – Week In a Nutshell

more:

http://www.benzinga.com/life/entrepreneurship/11/05/1064754/words-

Jan 16

th

2015

of-wisdom-famous-trading-investing-and-money-sayings-part-