18 February 2015

4QCY14 Results Update | Sector:

Cement

Ambuja Cements

BSE SENSEX

S&P CNX

29,320

8,869

Bloomberg

ACEM IN

Equity Shares (m)

1,549.8

M.Cap. (INR b) / (USD b) 417.7/6.7

52-Week Range (INR)

271/151

1, 6, 12 Rel. Per (%)

8/15/34

Avg Val (INRm)/Vol ‘000 458/2,136

Free float (%)

49.7

n

Financials & Valuation (INR Billion)

Y/E Dec

2014 2015E 2016E

Sales

EBITDA

NP

Adj. EPS (INR)

EPS Gr. (%)

BV/Sh. (INR)

RoE (%)

RoCE (%)

P/E (x)

P/BV (x)

EV/EBITDA (x)

EV/Ton (USD)

99.1 109.5 124.7

18.6 24.5 31.5

13.2 16.8 21.9

8.5

8.5 11.1

25.9 -0.8 30.9

65.6 95.9 101.4

13.4 11.5 11.2

18.7 16.9 16.3

22.4 22.6 17.3

2.9

2.0

1.9

12.5 14.8 11.4

126

197

189

CMP: INR270

n

TP: INR262 (-3%)

Neutral

EBITDA miss on lower volume and higher RM & employee cost; payout

improved to INR5/share; cutting CY15/16E EPS by 5-6%

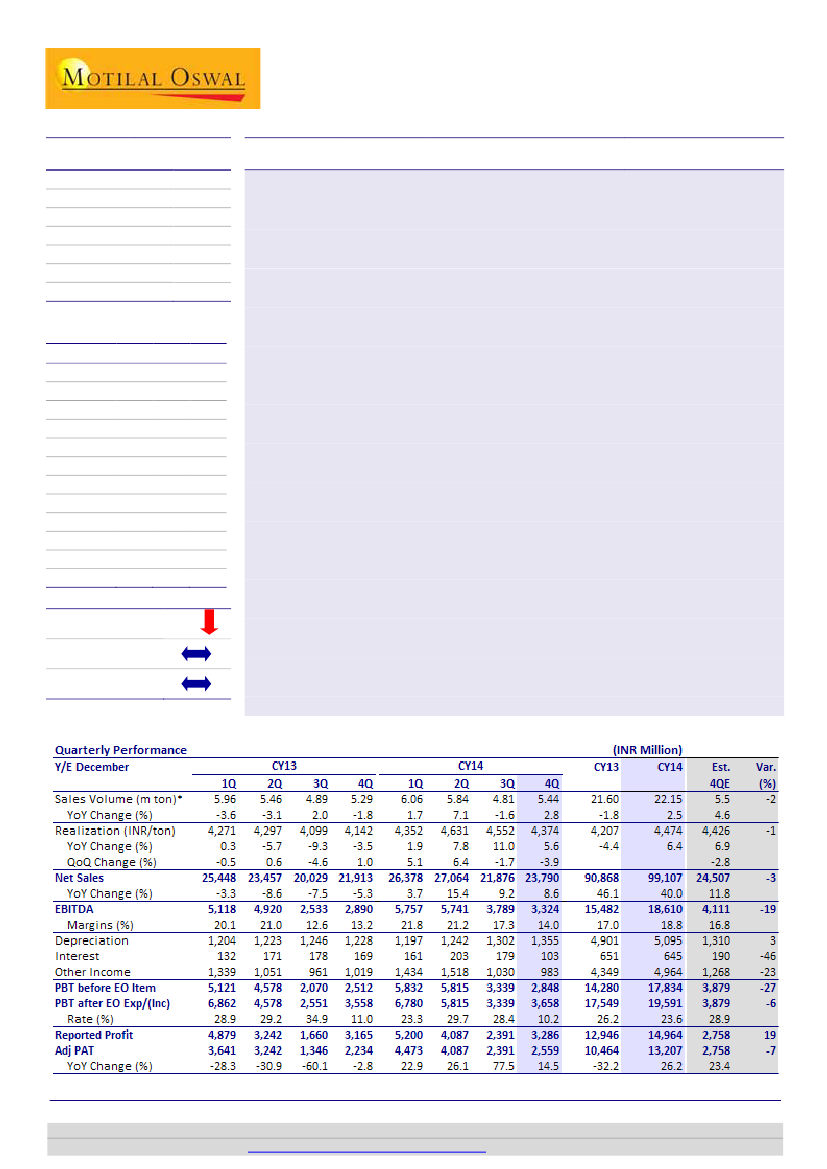

Revenue miss by 3% on lower volume:

ACEM’s 4QCY14 net sales grew by 8.6%

YoY (-4% QoQ) to INR23.8b (v/s est of INR24.7b), led by lower volume growth.

Cement volume stood at 5.44mt (v/s est 5.5mt), 2.8% YoY (+13% QoQ).

Realizations de-grew 3.9% QoQ (+5.6%YoY) to INR4,374/ton (v/s est of

INR4,426/ton). Annual volume grew 2.5% YoY to 22.15mt.

Higher RM & employee cost negate freight benefits:

EBITDA grew 15% YoY (-12%

QoQ) to ~INR3.3b (v/s est ~IN4.1b), translating into EBITDA margin of 14% (-3.3pp

QoQ and +0.8pp YoY) v/s est of 16.8%. Cost was flat QoQ (+INR167/ton YoY) as

against expectation of 2% QoQ decline on the back of lower input cost viz. coal

and diesel prices. While there has been 10%/4% QoQ drop in freight/energy cost,

higher employee and RM cost negated the benefits.

Tax write-back boosts PAT:

EBITDA/ton improved INR65 YoY (-INR371 QoQ) to

INR611 (v/s est ~INR742). PAT stood at INR3.3b (v/s est of INR2.8b), boosted by

prior period tax write back.

Higher payout of INR5/share; No major capacity addition in foreseeable future:

ACEM declared dividend of INR5/share (with interim of INR1.8/share and final of

INR3.2/share) v/s INR3.6/share in CY13. In the context of global merger between

Holcim and Lafarge, immediate capacity addition is limited barring Sankrail (West

Bengal) grinding unit of 0.8mt expected in 2015.

Revising CY15/16E EPS by 5-6%:

We are cutting EPS for CY15/CY16 by 5.6%/5% to

INR8.5/11.1 respectively, to factor in for higher raw material and employee cost

and minor tweak in below-EBITDA items. We factor in for 4%/5% YoY volume

growth and INR14/bag and INR20/bag YoY rise in realizations in CY15/16. These

translate into EBITDA of INR1,066/INR1,302 per ton for CY15/16. We value ACEM

at INR262 (at ~USD180/ton - 20% discount to Ultratech or implied EV/EBITDA

10.5x CY16E EV/EBITDA). It offers ~3% downside at CMP. Maintain

Neutral.

n

n

n

Estimate change

TP change

Rating change

5-6%

Jinesh Gandhi

(Jinesh@MotilalOswal.com); +91 22 3982 5416

Sandipan Pal

(Sandipan.Pal@MotilalOswal.com); +91 22 3982 5436

Investors are advised to refer through disclosures made at the end of the Research Report.

Motilal Oswal research is available on

www.motilaloswal.com/Institutional-Equities,

Bloomberg, Thomson Reuters, Factset and S&P Capital.