29 May 2015

4QFY15 Results Update | Sector:

Cement

The Ramco Cements

BSE SENSEX

27,828

Bloomberg

Equity Shares (m)

M.Cap. (INR b) / (USD b)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

Avg Val INRm/Vol ‘000

Free float (%)

S&P CNX

8,434

TRCL IN

238.0

76.9/1.2

380/256

3/-3/7

77/247

57.7

CMP: INR323

TP: INR416 (+29%)

Buy

Strong margin show despite dismal volume; cost moderates QoQ; demand

recovery in south and pricing strength to be the key catalysts

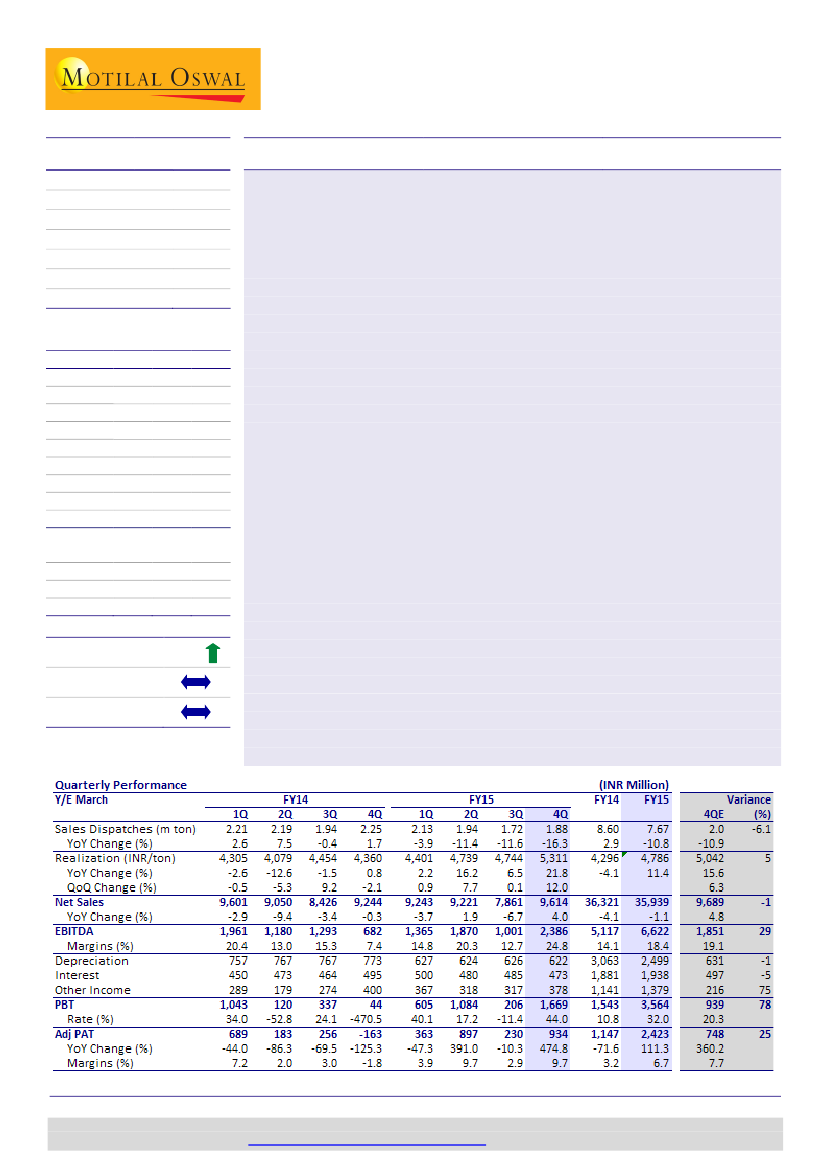

Pricing strength offset dismal volume:

Ramco Cement’s (TRCL) 4QFY15 revenue

stood at INR9.6b (in line)—up 4% YoY and 22% QoQ). Led by strong uptrend in

cement prices in south, TRCL posted 12% QoQ (+22% YoY) growth in realizations,

which more than offset volume trend that were weakest in five years. 4QFY15

volume de-grew 16.3% YoY (+9% QoQ) to 1.88mt.

Strong margin show, 10-Q high profitability:

EBITDA stood at INR2.3b (v/s INR1b

in 3QFY15 and INR682m in 4QFY14) v/s est. of INR1.8b, translating into EBITDA

margin of 24.8% (+12.1ppQoQ, +17.4pp YoY). EBITDA/ton stood at INR1,269

(+INR687 QoQ, +INR966 YoY) v/s est. of INR924. Cement EBITDA/ton stood at

INR1,300. However, higher tax due to change in surcharge on corporate tax

dented PAT, which stood at INR934m (v/s est. of INR748m).

Efficiency measures and fuel price reduction benefit cost:

TRCL posted 4% QoQ

moderation in blended cost/ton (INR3,845/ton). Besides all-round cost efficiency

measures, this was led by softening fuel prices and rise in pet coke mix (~14%).

This was, however, partially negated by increase in royalty on limestone (from

INR63/ton in 3Q to INR80/ton), higher rail freight (negated benefits of diesel price

reduction).

Other updates:

(a) 0.95mt grinding unit at Visakhapatnam, AP commissioned in

March-15, (b) Wind farm division recorded a fall of 5.6crore units in generation of

power compared with FY14, (c) dividend of INR1.5 per share on equity capital

declared (v/s INR1/share in FY14), (d) capex of INR3b-3.5b in FY16 toward

maintenance and clinker de-bottlenecking at Jayanthipuram (AP) plant, which

would augment capacity by ~0.5mt, (e) targets 50% pet coke mix over medium

term.

Valuation and view:

We raise FY16/17E EPS by 16%/8% to factor in for higher

realizations in FY16 (INR22/bag YoY v/s the earlier estimate of INR17/bag YoY) and

lower volume (2% YoY in FY16 v/s the earlier estimate of 5%). The stock trades at

13.2x FY17E EPS and 7.9x FY17E EV/EBITDA, and EV/ton of USD97. We maintain

Buy

with a TP of INR416, an upside of 29% (valuing cement business at EV/ton of

USD120). Demand recovery in south (particularly in AP and Tamil Nadu) with

pricing strength would be the key catalysts.

Financials & Valuation (INR b)

Y/E MAR

2015 2016E 2017E

Sales

35.9 40.5 47.2

EBITDA

6.6

9.3 11.9

NP

2.4

3.9

5.8

Adj EPS (INR) 10.2 16.3 24.4

EPS Gr. (%) 106.8 60.3 49.6

BV/Sh. (INR) 111.1 125.1 146.1

RoE (%)

9.5 13.8 18.0

RoCE (%)

10.2 14.3 19.4

Payout (%)

17.1 14.2 14.3

Valuations

P/E (x)

31.7 19.8 13.2

P/BV (x)

2.9

2.6

2.2

EV/EBITDA

(x) 15.5 10.6

7.9

103

97

EV/Ton (USD)

114

Estimate change

TP change

Rating change

8-16%

Sandipan Pal

(Sandipan.Pal@MotilalOswal.com); +91 22 3982 5436

Jinesh Gandhi

(Jinesh@MotilalOswal.com); +91 22 3982 5416

Investors are advised to refer through disclosures made at the end of the Research Report.

Motilal Oswal research is available on

www.motilaloswal.com/Institutional-Equities,

Bloomberg, Thomson Reuters, Factset and S&P Capital.