27 October 2015

2QFY16 Results Update | Sector:

Entertainment

BSE SENSEX

27,253

Bloomberg

Equity Shares (m)

M.Cap. (INR b) / (USD b)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

Avg Val (INR m)

Free float (%)

S&P CNX

8,233

WONH IN

56.5

17.8/0.3

349/242

3/12/-2

55

29.0

CMP: INR315

TP: INR360 (+15%)

Wonderla Holidays

Buy

Financials & Valuation (INR Billion)

Y/E MAR

Sales

EBITDA

NP

EPS (INR)

Gr. (%)

BV/Sh. (INR)

RoE (%)

RoCE (%)

P/E (x)

P/BV (x)

2015 2016E 2017E

1.8

0.8

0.5

9.0

-5.7

63.1

20.0

27.4

35.2

5.0

2.1

0.9

0.6

10.7

19.4

71.4

15.9

22.6

29.5

4.4

3.2

1.3

0.8

13.9

30.0

82.4

18.1

25.6

22.7

3.8

Estimate change

TP change

Rating change

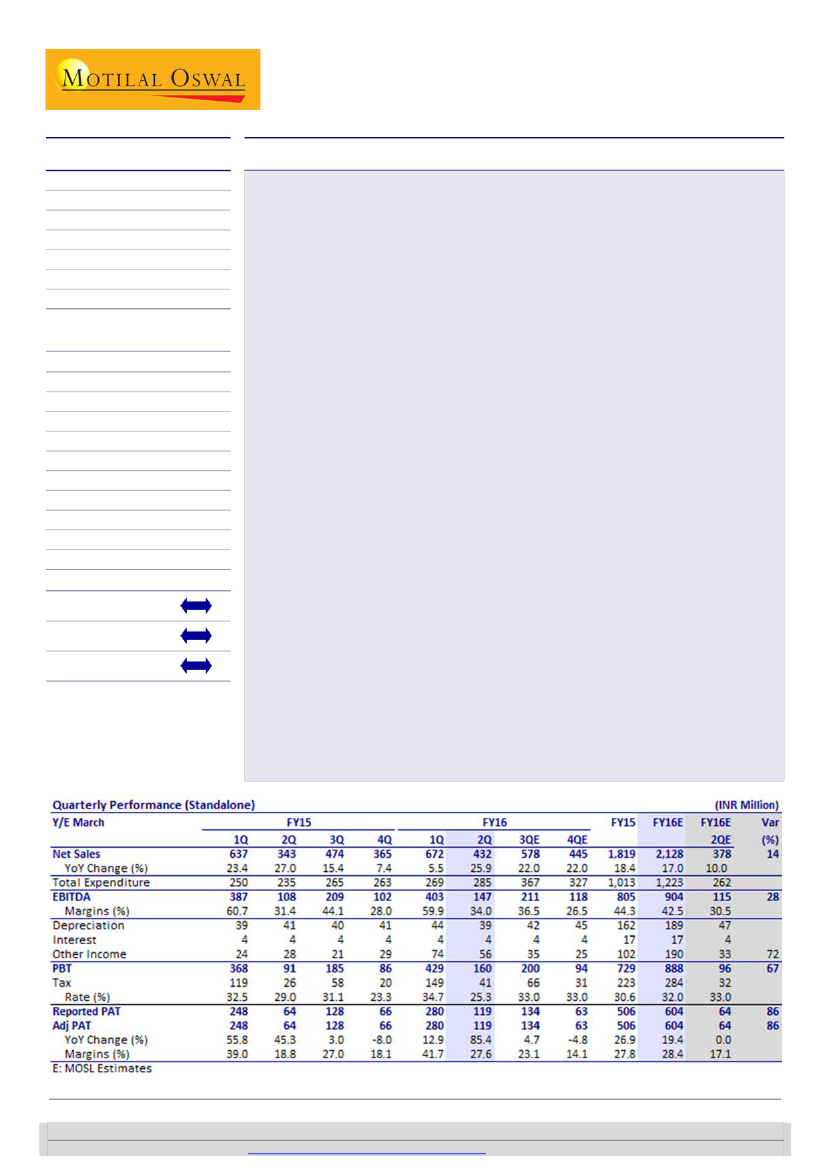

Strong footfall growth of 7% YoY and realization growth of 17% YoY leads to all-

round beat:

Wonderla Holidays saw 2QFY16 revenue grow 25.9% YoY to INR432m

(est. of INR378m) v/s INR343m in 2QFY15. Footfalls grew 7% YoY to 469.6k in

2QFY16 while average revenue per visitor grew 17% YoY to INR955. The company

effectively took two price hikes—one in 1QFY16 of ~10% and second of ~5% in

2QFY16—to cushion the effect of contingent provisions toward service tax.

Management maintained its guidance of ~3-4% footfall growth in FY16.

Margins higher than estimates; provision for disputed service tax drags margins:

EBITDA grew 37% YoY in 2QFY16 to INR147m (est. of INR115m); EBITDA margins

stood at 34% (est. of 30.5%) v/s 31.4% in 2QFY15, an expansion of 260bp YoY.

Other expenses increased 770bp, mainly on account of INR30m of provision for

disputed service tax liability. Management highlighted that post filing an appeal

against levy of service tax in Kochi and Bangalore High Courts, the company has

received a stay order from the Kochi court and has accordingly discontinued

charging and recovering service tax from July 1 in the city. Though the case is still

pending in Bangalore, Wonderla has discontinued charging and recovering service

tax in the city from August 12, 2015. PAT for 2QFY16 stood at INR119m (est. of

INR64m), a YoY growth of 85.4%.

2HFY16 footfall growth to be significantly stronger than 1HFY16:

Seasonally, 1Q

and 3Q are the strongest quarters for amusement parks. Given the focus on

promotional campaigns, coupled with revival in demand from schools, we believe

footfall growth should revive from -2% in 1HFY16 to +8% in 2HFY16. However, we

believe continued provisioning for disputed service tax and higher advertising

spends (deferred from 2Q to 3Q due to delayed festive season) will result in flat

EBITDA growth in 2HFY16.

Valuation and view:

We expect WONH’s revenue to clock 33% CAGR and 24%

PAT CAGR over FY15-17. We upgrade our FY16/FY17 EPS estimates by 11%/4%,

given the strong earnings beat in 2QFY16 and footfall growth revival expected in

2HFY16. We believe WONH is on track to be a pan-India player over the long run

and will be a major beneficiary of the amusement park industry’s development.

The stock trades at 29.5x FY16E and 22.7x FY17E earnings; we value WONH at 26x

FY17E EPS, with a target price of INR360. Maintain

Buy.

Results beat expectations; footfall growth revival expected in 2HFY16

Niket Shah

(Niket.Shah@MotilalOswal.com); +91 22 3982 5426

Atul Mehra

(Atul.Mehra@MotilalOswal.com); +91 22 3982 5417

Investors are advised to refer through disclosures made at the end of the Research Report.

Motilal Oswal research is available on

www.motilaloswal.com/Institutional-Equities,

Bloomberg, Thomson Reuters, Factset and S&P Capital.