28 October 2015

3QCY15 Results Update | Sector: Cement

BSE SENSEX

27,226

Bloomberg

Equity Shares (m)

M.Cap. (INR b)/(USD b)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

Avg Val(INR m)

Free float (%)

S&P CNX

8,240

ACEM IN

1,983.2

323.5/5.0

287/192

-4/-11/-7

478

49.7

Ambuja Cements

CMP: INR209

TP: INR245 (+18%)

Upgrade to buy

Operations in line; valuation comfort improves; upgrade to Buy

Financials & Valuation (INR Billion)

Y/E Dec

2015 2016E 2017E

Sales

EBITDA

NP

94.9 108.3 127.5

15.3 21.7 30.4

9.5 14.9 21.0

7.5 10.6

22.6 41.2

96.6 102.9

10.1 10.6

14.1 15.1

57.6 40.3

16.6

1.3

12.2

134

11.8

1.2

8.4

123

Adj. EPS (INR)

6.1

EPS Gr. (%)

-28.3

BV/Sh. (INR)

66.1

RoE (%)

9.3

RoCE (%)

13.4

Payout (%)

92.4

Valuations

P/E (x)

34.1

P/BV (x)

3.2

EV/EBITDA (x) 17.9

EV/Ton (USD)

142

Estimate change

TP change

Rating change

-4-5%

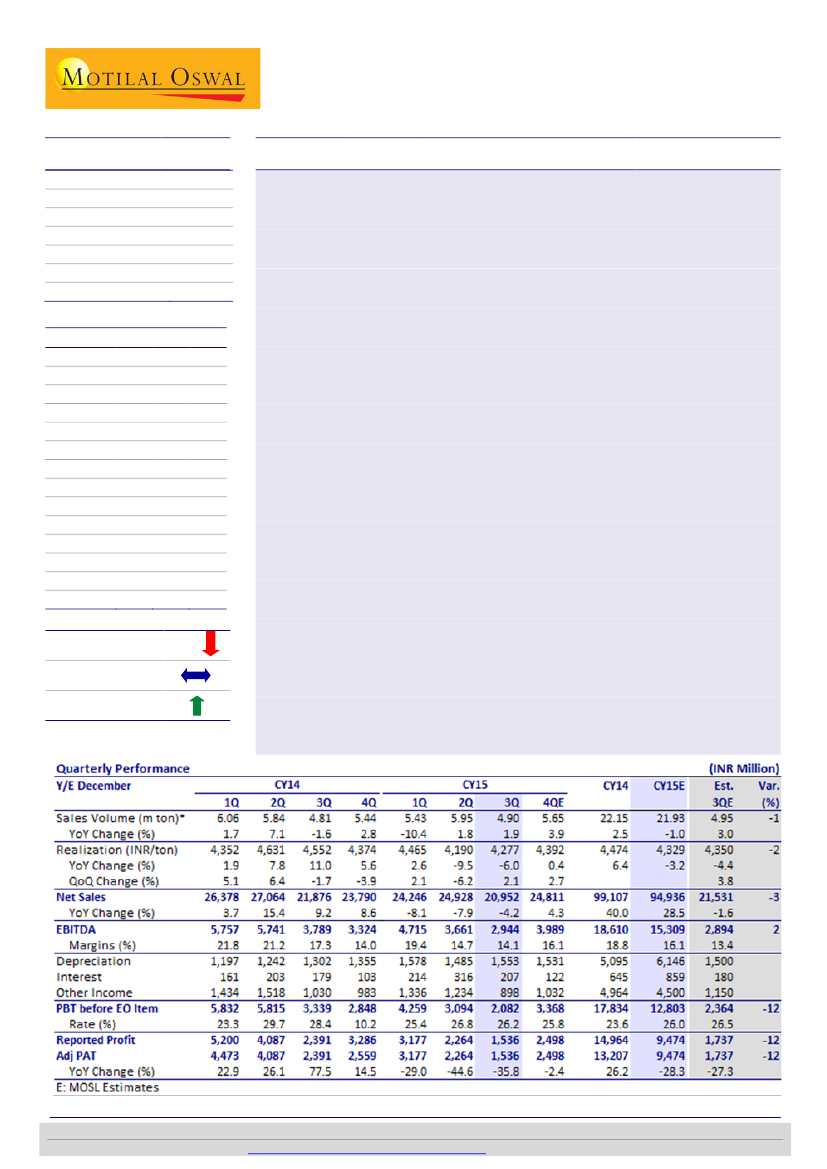

Volume growth dichotomy declined:

ACEM’s 3QCY15 revenue was marginally

below estimate at INR20.9b (-4.2% YoY). Volume growth was in line at 4.9mt

(+2% YoY v/s UTCEM at +4% YoY). Uptick in realizations (+2% QoQ) was below

expectation and was largely contributed by north and west.

Cost moderation boosts EBITDA (in line):

EBITDA de-grew 22% YoY to

~INR2.94b (in line), translating into EBITDA margin of 14.1% (-3.2pp QoQ and -

0.6pp YoY). Lower uptick in realizations was offset by cost savings in RM and

other expenses (decline in gypsum and packaging cost) and moderation in

freight cost (benefits of softening diesel price). PAT was down 35.8% YoY to

INR1.53b (v/s est. of INR1.73b), led by lower other income.

DMF-adjusted EBITDA up 7% QoQ:

EBITDA/ton stood at INR601 (v/s est. of

INR585). In 3QCY15, ACEM provided for DMF of INR82/ton (including prior

period impact of INR55/ton); adjusted for the same, EBITDA/ton stood at

INR656 (-17% YoY, +7% QoQ).

Valuation comfort improves; upgrade to Buy

ACEM corrected 27% from the peak versus average correction of 13% in large

caps, led by muted earnings (weak north and west) and elusive timeline over

corporate restructuring.

We expect ACEM to lag volume growth leaders due to limited expansion, but

profitability is likely to normalize on the back of better pricing and demand

outlook in north and west (Gujarat). While there is little clarity on timeline and

form of restructuring (with ACC and Lafarge) at present, ACEM will be

considered on its strength (strong B/S, cost leadership, and healthy capital

efficiency) once it is resolved.

Post the recent corrections, valuation comfort in ACEM is higher than peers.

ACEM at 10.9x 1-year forward EV/EBITDA is 12% below the 5-year average.

EV/ton basis is at USD130/ton—11% discount to 5-year average (only large cap

trading below the 5-year average EV/EBITDA). We value ACEM at USD160/ton

(10x CY17E EV/EBITDA) at INR245/share (18% upside). Upgrade to

Buy.

Sandipan Pal

(Sandipan.Pal@MotilalOswal.com); +91 22 3982 5436

Investors are advised to refer through disclosures made at the end of the Research Report.

Motilal Oswal research is available on

www.motilaloswal.com/Institutional-Equities,

Bloomberg, Thomson Reuters, Factset and S&P Capital.