Crystal

Ball gazing

2016

Quantitative Research

Crystal Ball Gazing: Past performance & Future Expectation

Nifty : 7946

1

st

January 2016

Nifty continues to oscillate

Sector

Media

Pharma

Small-Cap

Mid-Cap

FMCG

IT

Auto

Energy

Infra

Bank

Realty

Metals

YoY (%)

10.30

9.26

7.21

6.46

0.33

-0.03

-0.32

-0.66

-8.91

-9.68

-15.02

-31.35

Potential Outperformers

Dish TV, ZEE Ltd

Dr Reddy

Wonderla

Arvind

Jublfoods

Tata Elexi

Bosch

Petronet LNG, IGL

Cromp Greav

ICICI Bank

HDIL

JSW Steel

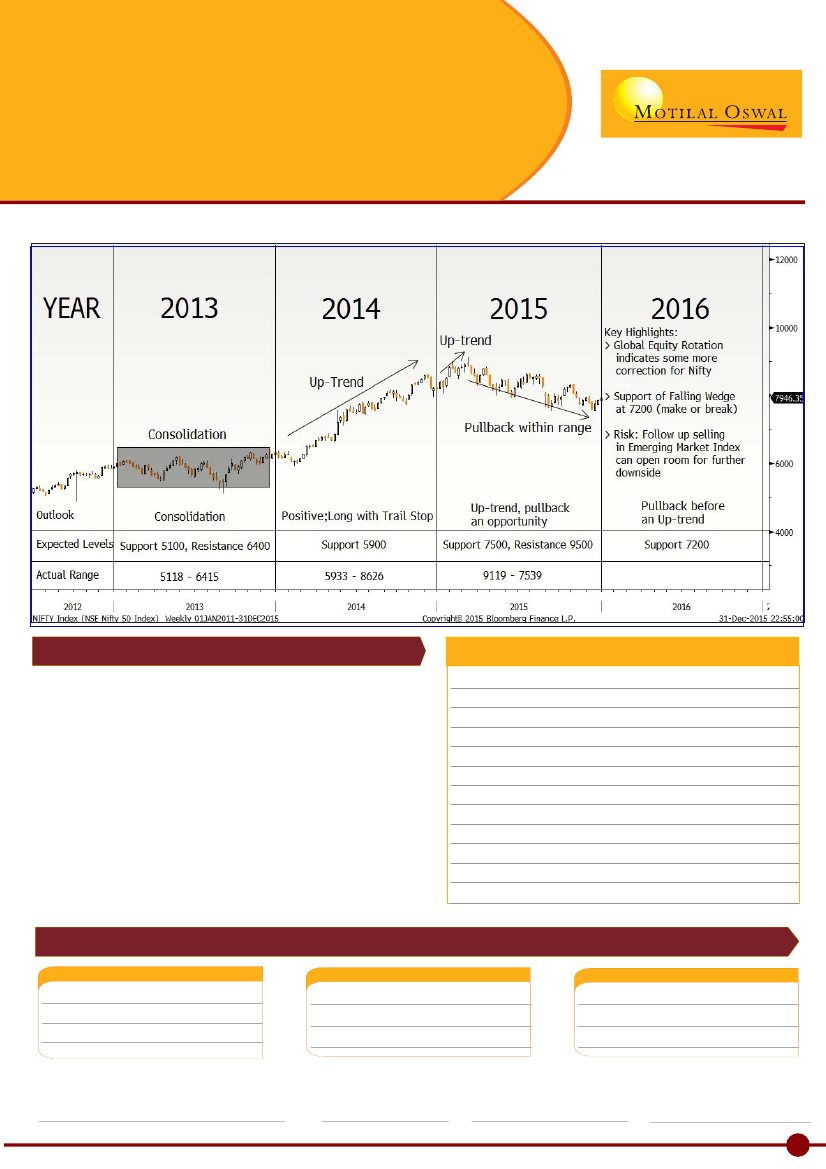

Nifty's Outlook

-

Nifty remains consolidating within the Falling

Wedge pattern with support at 7200 and breakout point being

8200. The range is expected to contract with time before a

directional move. 7200 remains a make or break point and

positions can be created once Index is around the same with a

stop marginally below it. Upside remains open and can be traded

with trailing stops later.

Key Risks

-

Follow up selling in Emerging Market Index (below

750) followed by a slide below 7200 can negate the outlook and

open more downside.

Top Picks - 2016

Stock Name

Arvind

Bajaj Fin

Bosch

CMP

358

6009

18647

Target

430

7400

23500

Stock Name

DishTV

Wonderla

TataElexi

CMP

101.5

397

2244

Target

140

490

2960

Stock Name

IGL

Petronet

PNB

CMP

529

256

116

Target

640

310

94

Shubham Agarwal, CMT, CFA, CQF

Head - Quantitative Research

Bhavin Desai

Head - Derivatives

Sacchitanand Uttekar

Technical Analyst

Pritika Poddar, CFA

Research Analyst

1

Note: To remain updated about the expected developments discussed in this Yearly report, please follow our MONTHLY QUANTITATIVE REPORT