Aurobindo Pharma

BSE SENSEX

23,759

Bloomberg

Equity Shares (m)

M.Cap.(INRb)/(USDb)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

Avg Val, INRm/ Vol m

Free float (%)

S&P CNX

7,216

ARBP IN

584.8

404.5 / 6.0

892/491

-14/8/50

1,689.1 / 1.7

46.1

10 February 2016

Q3FY16 Results Update | Sector: Healthcare

CMP: INR692

TP: INR1,100 (+59%)

Buy

Financials & Valuations (INR b)

Y/E Mar

2016E 2017E 2018E

Sales

138.2 163.1 192.4

EBITDA

31.9

39.2

48.7

NP

20.1

25.4

32.1

EPS (Rs)

34.5

43.5

55.0

EPS Gr (%)

24.4

26.3

26.5

BV/Sh (Rs)

119.7 160.7 213.3

RoE (%)

33.1

31.0

29.4

RoCE (%)

29.2

30.6

32.0

P/E (x)

20.1

15.9

12.6

P/BV (x)

5.8

4.3

3.2

Estimate change

TP change

Rating change

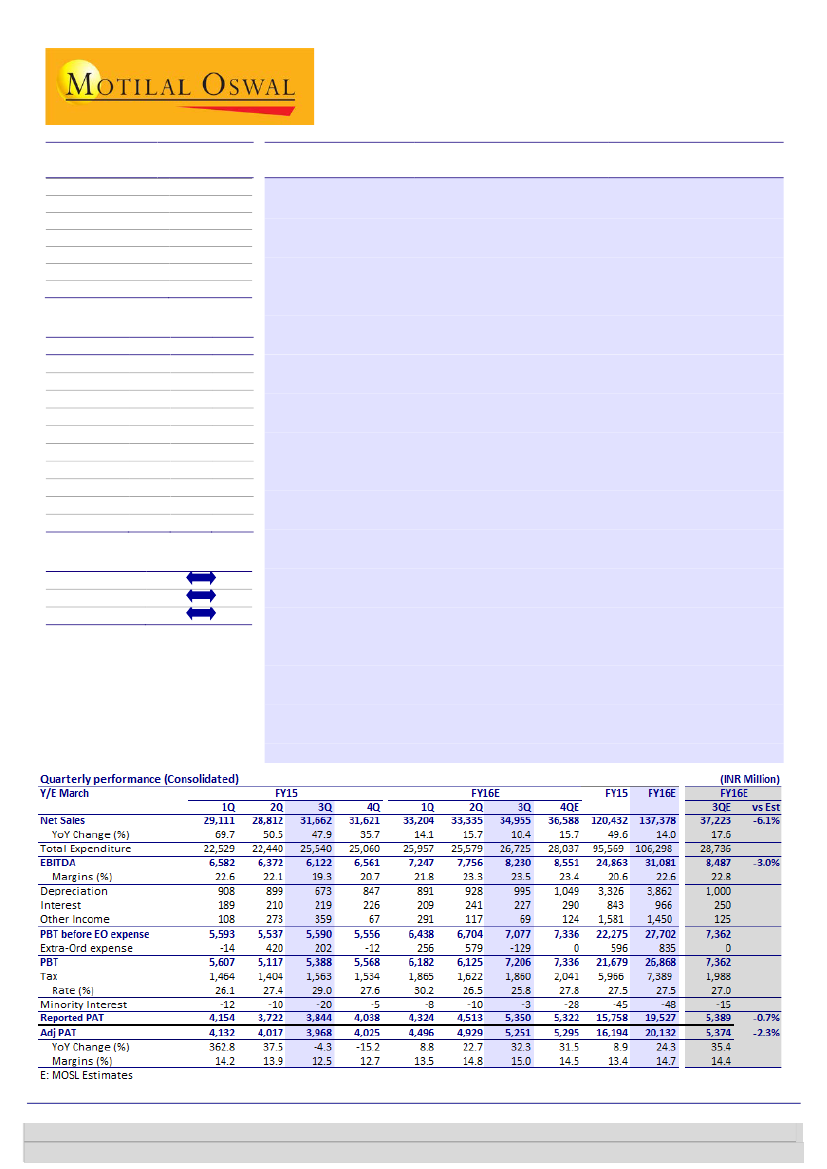

ARBP reported 3QFY16 results with net sales at INR 34.96b, driven by strong US

numbers (up 31% YoY growth) partially offset by weak Europe (down 9.6% YoY due

to currency depreciation). EBITDA came in at INR8.2m, up 34% YoY (~3% miss)

with PAT at INR5.35b, up 39% YoY (in-line with est). We believe strong pace of

approvals in the US and improving profitability of EU business is likely to drive

overall margins and earnings growth for the company.

EBITDA margins continue to expand:

EBITDA margin at 23.5% (up >400bps YoY),

improved for the fourth quarter in a row on the back of strong US sales and cost

efficiency achieved in Europe. We expect EBITDA margin to increase to 25.3% in

FY18E from 20.6% in FY15, on the back of a) strong launch pipeline in US, and (b)

cost efficiency in EU (Margins expected to be in high single digit by FY18).

Strong momentum in US sales to continue:

US sales came in at USD240m (vs USD

228m in 2Q). We expect US sales to grow at this robust pace in coming quarters on

the back of ramp-up of existing launches including (Integrilin, Isosulfan, etc) and

upcoming launches like Meropenem, Valgancyclovir, Angiomax, and Nexium etc.

Debt reduction continues:

The company reported debt reduction of USD50m QoQ

in 3Q (USD70m YTD). Going forward, we expect FCF generation momentum to

pick-up further (greater than USD300m between FY17 & FY18) on the back of US

sales ramp-up and margin improvement in EU.

Regulatory concerns unwarranted- Buy on weakness:

ARBP stock has corrected

~18% in last one month primarily due to concerns related to observations raised by

US FDA at Unit VII plant. We believe that concerns related to 483 observations at

unit VII are unwarranted as there are no data integrity issues and most importantly

company has received two approvals (on 2

nd

& 5

th

Feb) from this facility post the

inspection. At CMP, ARBP trades at 15.9x FY17E and 12.6x FY18E— at ~20%

discount to peers. Going ahead, valuation gap is expected to narrow down on the

back of increasing profitability and strong free cash flows generation. ARBP

remains one of our top pick in the sector with a target price of INR1,100 @ 20x

FY18E PER (vs INR1,050 @ 20x 1H FY18E PER).

In line result; FCF generation bodes well

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

Kumar Saurabh

(Kumar.Saurabh@MotilalOswal.com); +91 22 3982 5584

Amey Chalke

(amey.chalke@motilaloswal.com); +91 22 39825423