24 February 2016

4QCY15 Results Update | Sector: Lubricants

BSE SENSEX

23,089

Bloomberg

Equity Shares (m)

M.Cap. (INR b) / (USD b)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

Avg Val (INR m)

Free float (%)

S&P CNX

7,019

CSTRL IN

494.6

201/2.9

518 / 370

3/3/6

128

29.0

Castrol India

CMP: INR407

TP: INR474 (+16%)

Neutral

EBITDA miss due to lower volumes and higher other expenses; await

volume growth revival

Financials & Valuation (INR Billion)

Y/E Dec

Sales

EBITDA

Adj. PAT

Adj. EPS (INR)

EPS Gr. (%)

BV/Sh.(INR)

RoE (%)

RoCE (%)

P/E (x)

P/BV (x)

Estimate change

TP change

Rating change

2015

32.9

8.8

6.0

12.0

24.5

12.0

76.6

107.8

33.9

34.0

2016E

34.3

9.7

6.7

13.5

12.5

13.9

109.2

154.7

30.2

29.4

4-7%

7%

2017E

36.2

10.6

7.3

14.8

9.2

15.8

104.7

144.3

27.6

25.8

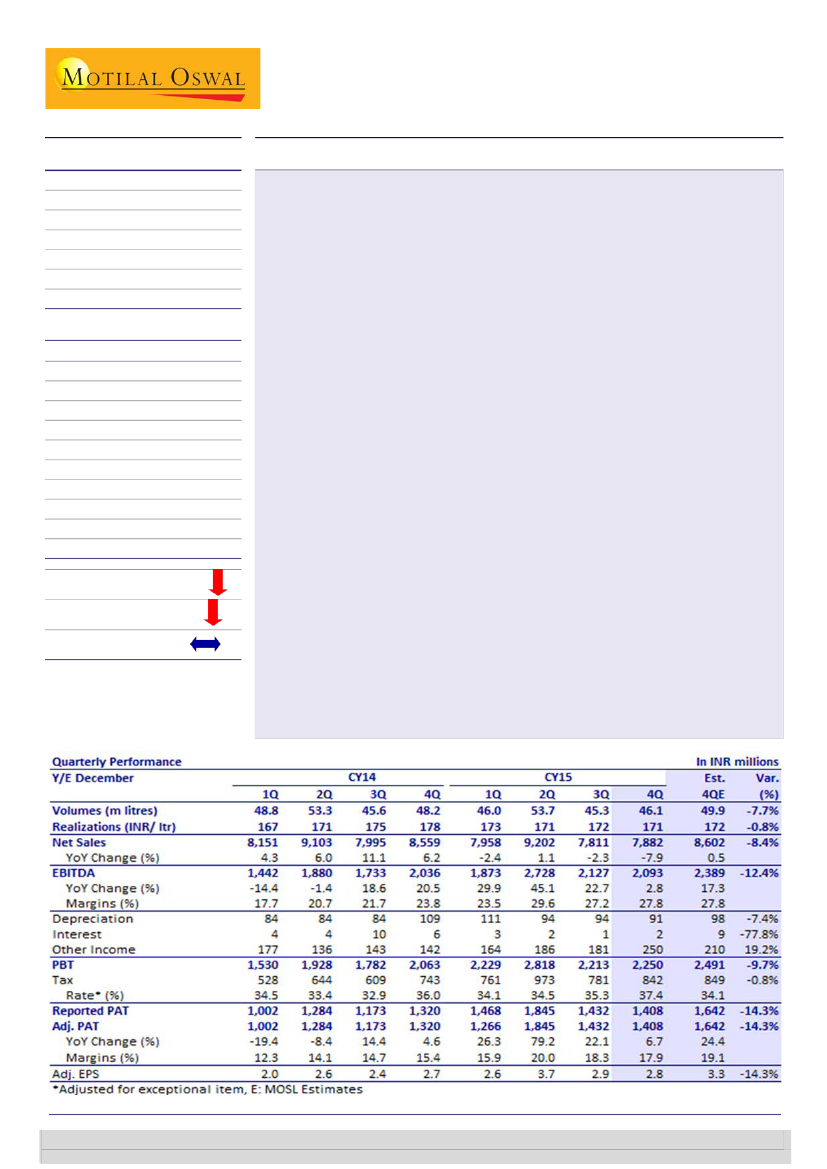

Castrol India’s 4QCY15 EBITDA of INR2.1b (+3% YoY, -2% QoQ) was below our

est. of INR2.4b led by (a) lower–than-expected volumes; (b) higher other

operating expenses due to INR100m of CSR expenses. Reported PAT was below

expectations at INR1.4b (+7% YoY, -2% QoQ)—led by higher than expected tax

rate of 37.4% (est. of 34%).

Revenue stood at INR7.9b (est. of INR8.6b; -7.9% YoY, -0.9% QoQ) impacted by

(a) lower volumes and (b) lower realizations

Realization stood at INR171/ltr (-4% YoY, flat QoQ) while sales volume stood at

46.1m ltr (-4% YoY, +2% QoQ). QoQ volume increase was primarily due to

seasonality. Automotive volumes increased 2% QoQ. While overall automotive

market has declined, personal mobility market volumes have increased. Poor

monsoons have impacted rural demand and in particular in agriculture segment.

Gross margin INR90/lt (+15% YoY, +2% QoQ); the QoQ increase was due to lower

RM costs at INR80.8/ltr (-18% YoY, -4% QoQ).

EBITDA margin 26.6% (v/s 23.8% in 4QCY14 and 27.2% in 3QCY15) —EBITDA

margin was lower QoQ despite higher gross margins due to CSR expenses of

INR100m. Adj. EBITDA margin stands at 27.8%.

Castrol declared a final dividend of INR5/share (full year stands at INR9/share).

Outlook:

Lubricant business volume recovery continues to be delayed led by

subdued economic activity. Industrial segment will continue to see a drag and is

expected to show uptick with the likely economic pick-up toward end CY16.

INR/USD volatility is a concern. Expect volume uptick in 1QCY16 due to increased

discounts being offered by the company.

Valuation and view:

We reduce our earnings CY16/CY17 EPS by 7%/4% due to

delay in the volume uptick versus our earlier expectations. Earlier than expected

economic uptick is an upside risk to our estimates. Our fair value stands at

INR474 at 35x CY16E EPS. CSTRL trades at 30.2x/27.6 CY16E/CY17E EPS of

INR13.5/14.8.

Neutral.

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

Harshad Borawake

(HarshadBorawake@MotilalOswal.com); +91 22 3982 5432

Rajat Agarwal

(Rajat.Agarwal@MotilalOswal.com); +91 22 3982 5558