26 April 2016

1QCY16 Results Update | Sector: Capital Goods

ABB

BSE SENSEX

26,007

Bloomberg

Equity Shares (m)

M.Cap.(INRb)/(USDb)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

Avg Val, (INR m)

Free float (%)

S&P CNX

7,963

ABB IN

211.9

274.0 / 4.1

1,444/963

5/5/2

89

25.0

CMP: INR1,293 TP: INR1,220 (-6%)

Neutral

Financials & Valuations (INR b)

Y/E Dec

2015 2016E 2017E

Net Sales

81.4

87.0 100.7

EBITDA

7.5

8.8

11.1

PAT

3.3

4.2

5.5

EPS (INR)

15.8

19.6

26.1

Gr. (%)

22.8

24.6

32.8

BV/Sh (INR)

142.0 161.2 187.3

RoE (%)

11.1

12.2

13.9

RoCE (%)

10.6

12.8

14.5

P/E (x)

82.1

65.9

49.6

P/BV (x)

9.1

8.0

6.9

Estimate change

TP change

Rating change

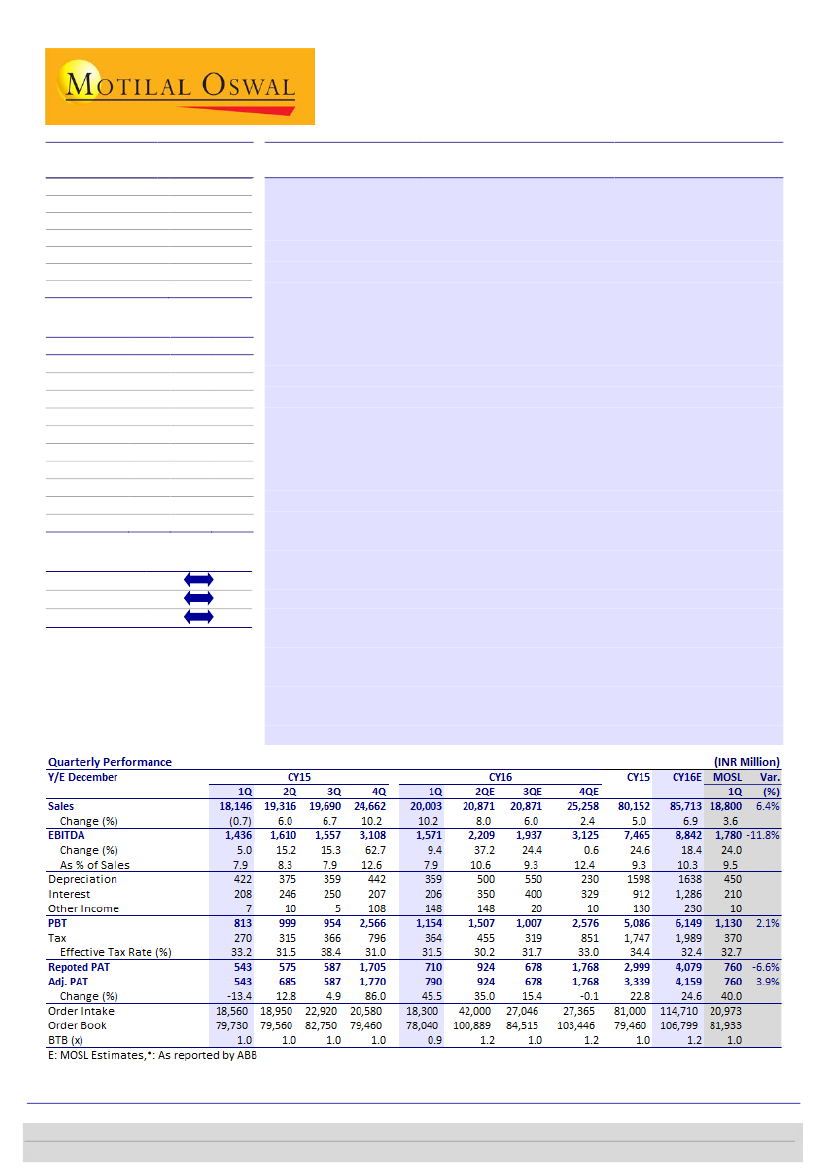

Execution remains strong; margin below estimate

Operational performance a mixed bag:

ABB’s 1QCY16 revenue at INR20b, up

10% YoY, was 6.4% higher than our estimate, while the adjusted EBIDTA

margin at 7.9%, flat YoY, was below our estimate of 9.5%. Key segments which

witnessed a strong performance were Discrete Automation with revenue at

INR7.7b (+32% YoY) and Electrification Products (+22.7% YoY). The decline in

Power Grid revenue to INR7.3b (-7.0%) was mainly a timing related issue, as

sales continued to be as per scheduled delivery. Adjusted PAT at INR790m was

marginally ahead of our estimate of INR760m on back of higher Other Income.

There was a forex loss of INR80m during the quarter.

Gross margin close to all time high:

Gross margin at 35.8% (+150bp) reflected

various initiatives taken over the last 3-4 years in terms of increased

localization, rationalization of supply chain, improving efficiency, better project

management capabilities, lower raw material prices and benefits of the EUR

depreciation. CY15 gross margin stood at 35% and management expects these

levels to sustain, going forward.

Order inflow stagnates due to weak finalization of orders:

Order inflow was

flat at INR18.3b (-1% YoY) on account of weak finalization of large orders.

Segments like Renewable, T&D, and Railways supported order inflow, though

ordering in traditional sectors such as Cement, Steel and Oil & Gas remained

muted due to underutilization of existing capacities.

Valuation and view:

Management is still cautiously optimistic on the demand

scenario and remains focused on margin expansion through improvement in

operational efficiencies and localization efforts. While segments such as

Transmission, Renewable and Transportation are witnessing traction, an

improvement in traditional sectors of Steel, Cement and Oil & Gas remains

elusive. Valuations stand at 65.9x/49.6x CY16/17E EPS of INR19.6/26.1.

Maintain

Neutral,

with a price target of INR1,220 (40x CY18 EPS of INR30.5).

Ankur Sharma

(Ankur.VSharma@MotilalOswal.com); +91 22 3982 5449

Amit Shah

(Amit.Shah@MotilalOswal.com); +91 22 3029 5126

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.