8 August 2016

Q1FY17 Results Update | Sector: Consumer

Marico

BSE SENSEX

28,183

S&P CNX

8,711

CMP: INR300

TP: INR305(2%)

Neutral

Motilal Oswal values your support in

the Asiamoney Brokers Poll 2016 for

India Research, Sales and Trading

team. We

request your ballot.

Lower input costs drive profitability

Bloomberg

Equity Shares (m)

M.Cap.(INRb)/(USDb)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

Avg Val, INRm/ Vol m

Free float (%)

MRCO IN

1,290.2

324.3 / 4.9

307 / 190

10/13/37

388

40.3

Financials & Valuations (INR b)

Y/E Mar

2016 2017E 2018E

Net Sales

60.1

63.0

75.3

EBITDA

10.4

11.8

14.3

PAT

7.2

8.3

10.2

EPS (INR)

5.6

6.4

7.9

Gr. (%)

26.1

14.6

22.8

BV/Sh (INR)

16.3

18.5

21.6

RoE (%)

36.9

37.0

39.3

RoCE (%)

31.4

32.2

34.3

P/E (x)

53.5

46.7

38.0

P/BV (x)

18.5

16.2

13.9

Estimate change

TP change

Rating change

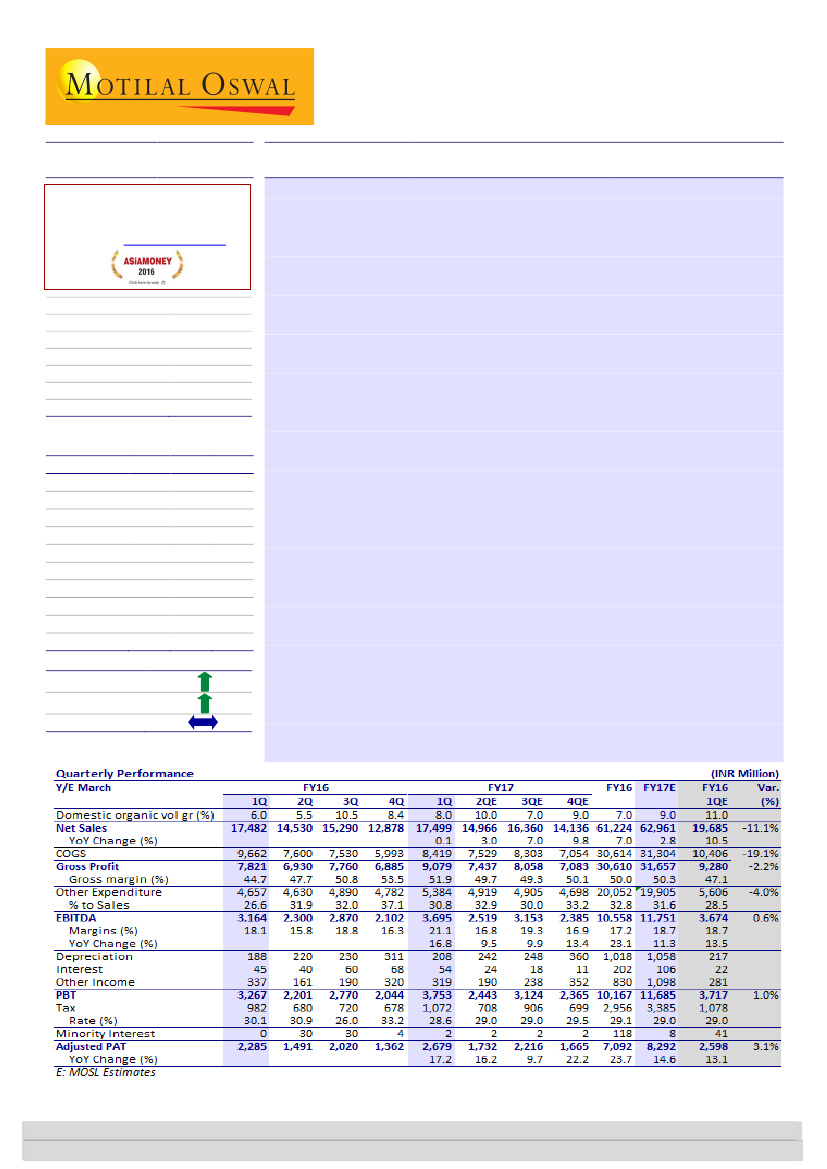

Sales below estimates; EBITDA and PAT exceed expectations:

Marico (MRCO)

posted flat consolidated net sales growth of 0.1% YoY (est. of +10.5% YoY) to

INR17.5b (Ind-AS), EBITDA growth of 16.8% YoY (est. of +13.5% YoY) to INR3.7b

and adjusted PAT growth of 17.2% YoY (est. of +13.1% YoY) to INR2.68b.

Volume growth was 8% for both the domestic (est. of 11%) and international

businesses. Domestic business reported flat revenue growth, with market

shares gained/maintained across all key segments – Parachute (7% volume and

-12% value growth), Saffola (11% volume and value growth) and VAHO (9%

volume and value growth).

Gross margins expanded 720bp YoY

to 51.9%, led by benign RM costs—copra

down 41% YoY (-7% QoQ), Liquid Paraffin down 19% YoY and HDPE down 9%

YoY. Despite higher ad spends (+220bp YoY) and other expenses (+160bp),

EBITDA margin expansion was impressive at 300bp YoY (est. of 50bp) to 21.1%.

PAT grew 17.2% YoY (est. of 13.1%) to INR2.68b.

Concall highlights:

(a) Volume growth guidance of 5-7% for the next three

quarters in Parachute. (b) Saffola volume growth guided at 10% in 2HFY17, and

sees a strong pipeline of products as well in that period (c) Guided for 8-10%

growth in VAHO volumes for the remainder of the year. (d) Monsoons will lead

to lower inflation and thus more spending power for consumers. DBT and 7th

Pay Commission implementation will also help rural demand.

Retain Neutral

:

Volume growth, although lower-than-anticipated, was healthy

across all domestic segments, which is a positive surprise when compared to

peers. Strong gross margin growth ensured EBITDA and PAT beat. While margin

gains may not be as high in the subsequent quarters with hardening input

costs, changes to our model have resulted in 2%/7% upgrade to our FY17/FY18

EPS forecasts. Consistently strong volume performance in an adverse

environment, healthy EPS growth, ROEs of close to 40% and high standards of

disclosures/corporate governance justify the valuation premium. Targeting

36xJune 2018 EPS, we get a TP of INR305. Maintaining

Neutral.

Krishnan Sambamoorthy

(Krishnan.Sambamoorthy@MotilalOswal.com); +91 22 3982 5428

Vishal Punmiya

(Vishal.Punmiya@MotilalOswal.com); +91 22 3980 4261

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.