12 January 2017

3QFY17 Results Update | Sector: Technology

TCS

BSE SENSEX

27,247

Bloomberg

Equity Shares (m)

M.Cap.(INRb)/(USDb)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

Avg Val, INRm

Free float (%)

S&P CNX

8,407

TCS IN

Set for new innings under Rajesh Gopinathan…

1,970

4,577.4 / 67.0

…Amid background of marginal 3Q beat and positive outlook

2740 / 2055

CFO Rajesh to succeed as the CEO:

With Mr. Natarajan Chandrasekaran set

3/-2/-10

to be the chairman of Tata Sons starting February 21, CFO Mr. Rajesh

2840

Gopinathan will take charge as the CEO of TCS. He started his professional

26.7

CMP: INR2,323 TP: INR2,550(+10%)

Neutral

Financials & Valuations (INR b)

2016

2017E

Y/E Mar

1,086.5 1,188.1

Net Sales

306.8

327.6

EBITDA

242.1

266.4

PAT

123.2

135.2

EPS (INR)

11.2

9.8

Gr. (%)

371.4

427.6

BV/Sh (INR)

37.1

33.8

RoE (%)

36.8

32.7

RoCE (%)

18.9

17.2

P/E (x)

6.3

5.4

P/BV (x)

2018E

1,345.0

367.8

286.2

145.3

7.4

505.5

31.1

29.4

16.0

4.6

Estimate change

TP change

Rating change

career with TCS in 2001. He was appointed as the CFO in February 2013, and

has also worked in roles of Strategy and Business Finance in the past. TCS

also announced N G Subramaniam as the COO of the company.

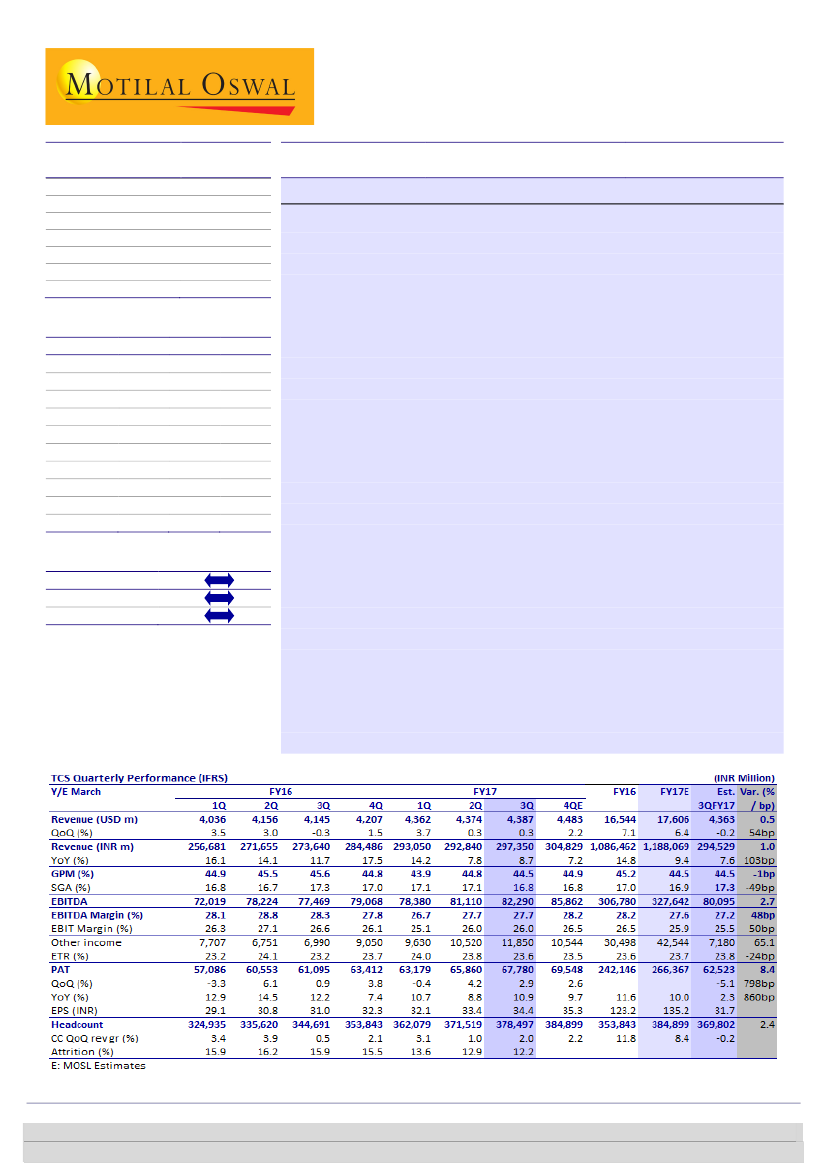

Marginal 3QFY17 beat:

TCS’ 3QFY17 CC revenue growth of 2.0% QoQ and

EBIT margin of 26% (flat QoQ) were both 50bp ahead of our estimates. India

(+10.3% QoQ), IMS (+9.5% QoQ CC) and Asset Leveraged solution (+21%

QoQ CC) drove growth, with BFSI and Retail seeing some recovery to grow at

company average. PAT was INR67.8b, +2.9% QoQ compared to our estimate

of INR62.5b aided by operating beat and higher other income.

Positive outlook - undeterred by visa implications:

TCS expects momentum

to sustain in 4Q, which drives our estimate of 2.2% QoQ CC growth next

quarter. Commentary was positive on all fronts: [1] Commitment to EBIT

margin band of 26-28% for now, despite the potential hike in wages for visa

employees, [2] Positive momentum in BFSI as clients shift from cost takeout

to growth, [3] Opportunity in traditional business from consolidation.

Valuation & View:

For the industry in last couple of years, topmost level

changes have understandably been accompanied with a round of flux ( more

recently at INFO, WPRO, MTCL), and one will have to be watchful of a

potentially similar shuffle at TCS. We tread cautiously as a result of this

uncertainty and ascribe a target multiple of 16x (v/s 17x earlier). Over FY16-

19, we expect TCS to grow its CC revenue/USD revenue/Earnings at CAGR of

10.1% / 8.3% / 8.8%. Our price target of INR2,550 implies 9% upside. Neutral

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

Ashish Chopra

(Ashish.Chopra@MotilalOswal.com); +91 22 6129 1530

Sagar Lele

(Sagar.Lele@MotilalOswal.com); +91 22 6129 1531