25 January 2017

3QFY17 Results Update | Sector: Technology

Wipro

BSE SENSEX

27,708

Bloomberg

Equity Shares (m)

M.Cap.(INRb)/(USDb)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

Avg Val, INRm

Free float (%)

S&P CNX

8,603

WPRO IN

India/ME and Healthcare headwinds cast shadow over near term

2,431

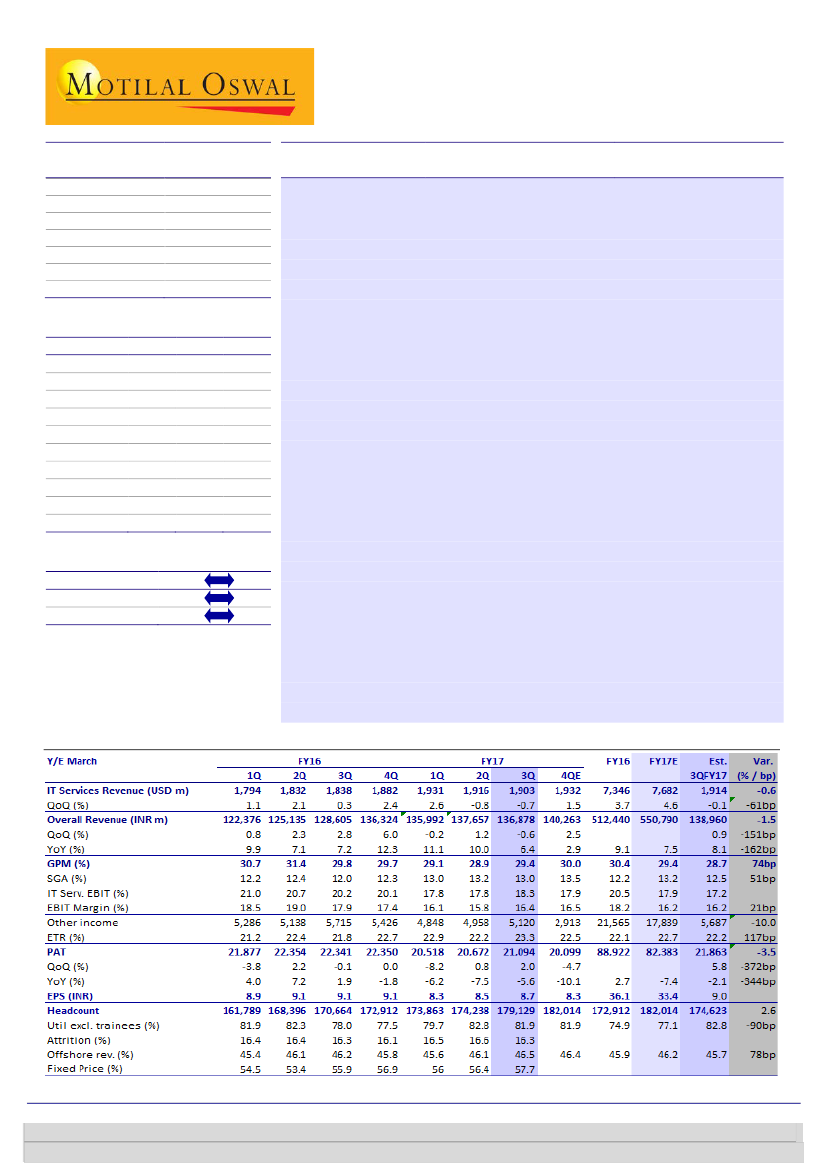

Organic revenue declines QoQ CC:

WPRO’s 3QFY17 CC revenue growth of

1,150.9 / 16.9

0.6% QoQ was marginally below our estimate of +1.3% QoQ, and in the

607 / 410

lower half of the company’s guided band of 0-2%. Five weeks of revenue

-3/-13/-27

from the Appirio integration (~1.1% contribution) meant that organic

845

26.8

revenue declined 0.5% QoQ CC. Energy & Natural Resources grew 2.1% QoQ

CMP: INR474

TP: INR540(+14%)

Neutral

Financials & Valuations (INR b)

2016 2017E

Y/E Mar

512.4

550.8

Net Sales

108.1

109.6

EBITDA

88.9

82.4

PAT

36.1

33.4

EPS (INR)

2.9

-7.4

Gr. (%)

189.7

204.5

BV/Sh (INR)

20.3

17.0

RoE (%)

16.7

13.7

RoCE (%)

13.1

14.2

P/E (x)

2.5

2.3

P/BV (x)

2018E

595.8

124.6

90.1

37.2

11.1

229.4

17.0

14.4

12.7

2.1

Estimate change

TP change

Rating change

CC, while all other verticals grew below 1%. In terms of geographies, India &

ME declined 4.2% QoQ CC, while other geographies grew between 1-2%.

Strong execution aids margin beat:

IT Services EBIT margin was 18.3%

(+50bp QoQ), above our estimate of 17.2%, led by strong execution despite

headwinds from lower working days. Overall EBIT margin was 16.4%, in line

with our estimate of 16.2%, implying continued losses in products segment.

PAT grew 2.0% QoQ to INR21b, marginally below our estimate of INR21.9b.

Headwinds to India/ME and Healthcare mar guidance:

For 4QFY17, WPRO

guided for growth of 1-2% QoQ CC. However, excluding ~7 weeks of

expected Appirio revenues (~1.5%), the guidance for organic revenue is

-0.5% to +0.5% QoQ CC, or flat at the midpoint. WPRO’s restructuring in

India/ME business is expected to complete in a few quarters, and Healthcare

is reeling from uncertainty around the future of Affordable Care Act under

the new US President. These segments together contribute 26% of WPRO’s

revenues assuming no overlap.

Valuation view:

We cut forward revenue estimates by 2.4-2.9% and

earnings estimates by 5.4-5.9%, factoring in fresh concerns around

Healthcare in addition to ongoing India restructuring. Over FY16-19, we

expect USD revenue/EPS CAGR of 5%/6%. While valuations at 12.7x FY18E

appear inexpensive, multiple re-rating will elude as long as portfolio issues

drag growth. Our TP of INR540 discounts FY19E earnings by 13x.

Neutral.

Quarterly Performance (Consolidated)

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

Ashish Chopra

(Ashish.Chopra@MotilalOswal.com); +91 22 6129 1530

Sagar Lele

(Sagar.Lele@MotilalOswal.com); +91 22 6129 1531