Sector Update| 2 January 2017

Automobiles | Update

Automobiles

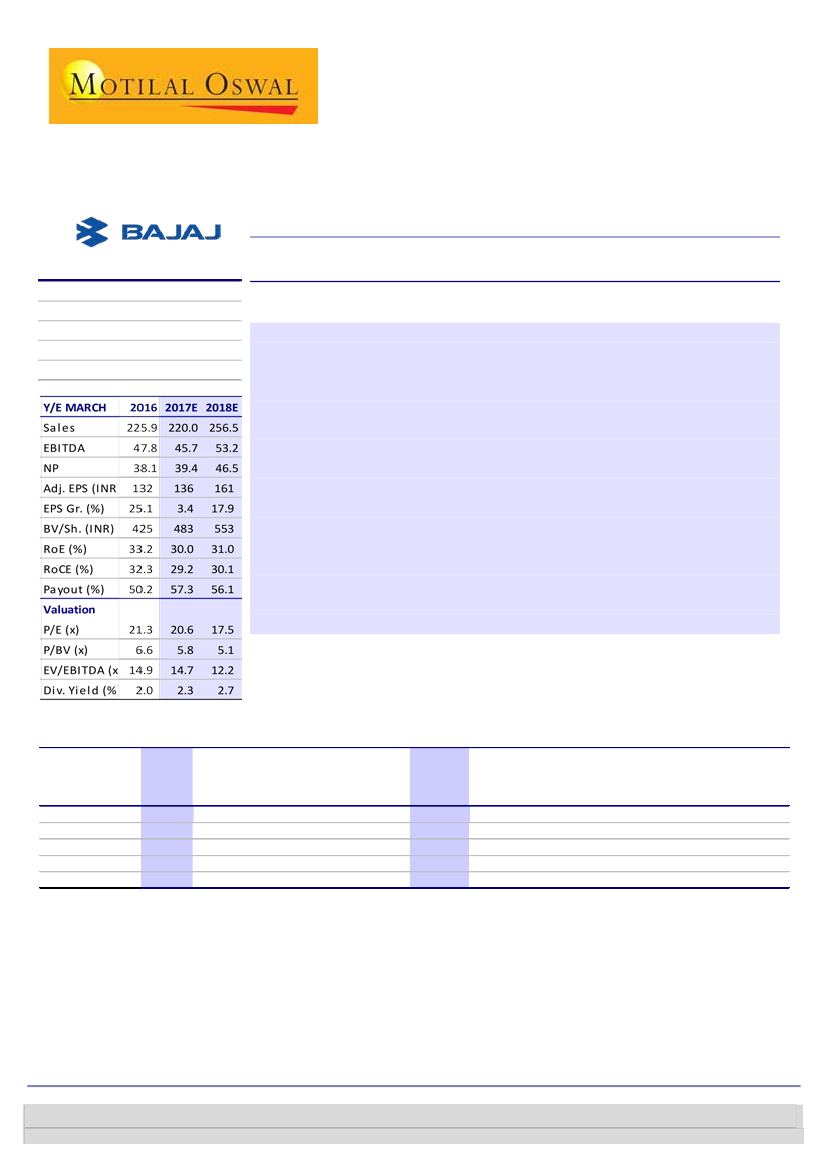

Bajaj Auto

CMP: INR2,809

Bloomberg

Equity Shares (m)

M.Cap. (INR b) / (USD b)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

BJAUT IN

289.4

812.8/11.9

3,122/2,173

2/-2/4

n

n

TP: INR3,432 (22% upside)

Buy

Jan-17 below est at 242k (v/s est 262k); decline of 18%YoY

Domestic vols decline 17% YoY on demonetization impact; Exports continue

to fall

n

n

n

n

BJAUT’s Jan-17 sales were below est, at 241,917 units (v/s est ~262,000), decline of

18% YoY. Domestic volumes declined by 16.5% YoY (+13% MoM) while exports

continued to decline with 19% YoY. Our FY17 estimates indicate a 5% decline implying

a residual growth of 3% or 297k units/month of run rate.

Domestic volumes at ~135.2k units (v/s est 147.5k units), declined by 17% YoY.

Motorcycle volumes declined by 16% YoY due to the impact of demonetization.

Domestic motorcycle sales were down 15% YoY (+12% MoM) to 119k units on account

of demonetization impact. While there was a MoM recovery, YoY still continues to be

under pressure. Motorcycle exports continued to fall, with a 18% YoY decline as

problems in export markets persisted.

3W volumes were the worst hit on demonetization impact. Domestic 3Ws declined by

27% YoY while 3W exports fell by 26% YoY. 3Ws were the worst hit in Bajaj’s portfolio.

Export volumes declined by 19% YoY (+1% MoM) as problems related to availability of

currency persited in key African markets. Besides, devaluation of currency has

impacted the purchasing power leading to slump in demand.

The stock trades at 17.5x/15.4x FY18E/19E EPS. Maintain Buy.

Snapshot of volumes for Jan-17

Jan-17

Total volume

Motorcycles

Three-Wheelers

Domestic

Exports

241,917

211,824

30,093

135,188

106,729

Jan-16

293,939

252,988

40,951

161,870

132,069

YoY (%)

-17.7

-16.3

-26.5

-16.5

-19.2

Dec-16

225,529

203,312

22,217

119,725

105,804

MoM (%)

7.3

4.2

35.5

12.9

0.9

FY17-YTD

3,120,154

2,730,739

389,415

1,926,229

1,193,925

FY16-YTD

Chg

(%)

FY17

estimate

Residual

YoY Resi-dual Gr.

Monthly

(%)

(%)

Run rate

2.9

4.7

-8.7

-6.8

21.0

297,384

261,494

35,890

176,146

121,238

3,315,062 -5.9 3,714,923 -4.6

2,858,721 -4.5 3,253,728 -3.1

456,341 -14.7

461,195 -13.8

1,775,911 8.5 2,278,522

5.8

1,539,151 -22.4 1,436,401 -17.4

Jinesh Gandhi

(Jinesh@MotilalOswal.com); +91 22 3982 5416

Aditya Vora

(Aditya.Vora@MotilalOswal.com); +91 22 3078 4701

2 January 2017

Investors are advised to refer through important disclosures made at the last page of the Research Report.

1

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.