8 May 2017

Corporate performance

4QFY17: Expectations v/s delivery

Today’s top research idea

Eicher Motors: In-line; RE margin stable, VECV big positive surprise

v

RE's EBITDA margin expanded ~180bp YoY to 31.4% (est. of ~32%), led by

higher other expenses. Further, lower other income restricted adj. PAT growth

to 8.5% YoY (to INR4.1b v/s est. of ~INR5.5b).

v

EBITDA margin expanded 370bp YoY (+130bp QoQ) to 8.2% (est. of 6.4%) led

by positive operating leverage. Adj. PAT was ~INR1.16b (est. of ~INR674m).

v

Waiting period for Classic 350 stable at ~2 months, with order booking in Top-

20 cities growing at over 15%. RE's producible capacity at ~825k for FY18 and

~960k for FY19. Declared a dividend of ~INR100/share for FY17 (flat YoY).

v

We have upgraded consol. EPS for FY18E/19E by 4%/8% to factor in better-

than-estimated VECV performance. Maintain

Buy

with a TP of INR30,402.

(no of

companies)

Sales

EBIDTA

PAT

Growth (YoY, %)

MOSL

Nifty

Sensex

(55)

(17)

(9)

14.7

16.8

17.5

7.5

10.1

4.4

9.7

2.1

7.7

Research covered

Cos/Sector

Financials

Cement

Cyient

Eicher Motors

Dr Reddy's

P&G Hygiene

Sanofi India

Equitas Holdings

Tata Comm

L&T Infotech

Orient Cement

NIIT Tech.

Results Expectation

Key Highlights

Making RBI captain of the ship

ACC-Ambuja: Board exploring merger opportunities

Good traction across core, adjacencies and DLM

In-line; RE margin stable, VECV performance a big positive surprise

Bachupalli 483 observations-no data integrity issue, but approvals

may get delayed

Payout of INR12b cash a huge boost to return ratios

Weak results; margin improvement is key

Risk aversion mars growth; bank transition dragged profits lower

Expect steady EBITDA growth, RoIC improvement

Stable revenue growth and positive outlook

Profitability uptick led by cost efficiencies

Above-estimate excluding one-offs

ABB | Bharti Infratel | Union Bank

Market snapshot

Equities - India

Close

Chg .%

Sensex

29,859

-0.9

Nifty-50

9,285

-0.8

Nifty-M 100

18,049

-1.0

Equities-Global

Close

Chg .%

S&P 500

2,399

0.4

Nasdaq

6,101

0.4

FTSE 100

7,297

0.7

DAX

12,717

0.5

Hang Seng

9,926

-1.6

Nikkei 225

19,446

-0.7

Commodities

Close

Chg .%

Brent (US$/Bbl)

49

2.4

Gold ($/OZ)

1,222

-0.5

Cu (US$/MT)

5,563

0.8

Almn (US$/MT)

1,896

-0.6

Currency

Close

Chg .%

USD/INR

64.4

0.3

USD/EUR

1.1

0.1

USD/JPY

112.7

0.6

YIELD (%)

Close

1MChg

10 Yrs G-Sec

6.9

0.0

10 Yrs AAA Corp

8.2

0.0

Flows (USD b)

5-May

MTD

FIIs

-0.1

-0.1

DIIs

0.0

0.3

Volumes (INRb)

5-May

MTD*

Cash

335

313

F&O

4,013

4,722

Note: YTD is calendar year, *Avg

YTD.%

12.1

13.4

25.8

YTD.%

7.2

13.3

2.2

10.8

5.7

1.7

YTD.%

-11.8

6.0

0.7

11.3

YTD.%

-5.2

4.6

-3.6

YTDchg

0.4

0.6

YTD

6.1

1.9

YTD*

284

4,640

Piping hot news

Royal Enfield revving up to buy Ducati?

v

Royal Enfield is understood to have been approached to acquire Italian superbike

maker Ducati, owned by Germany's embattled Volkswagen group.

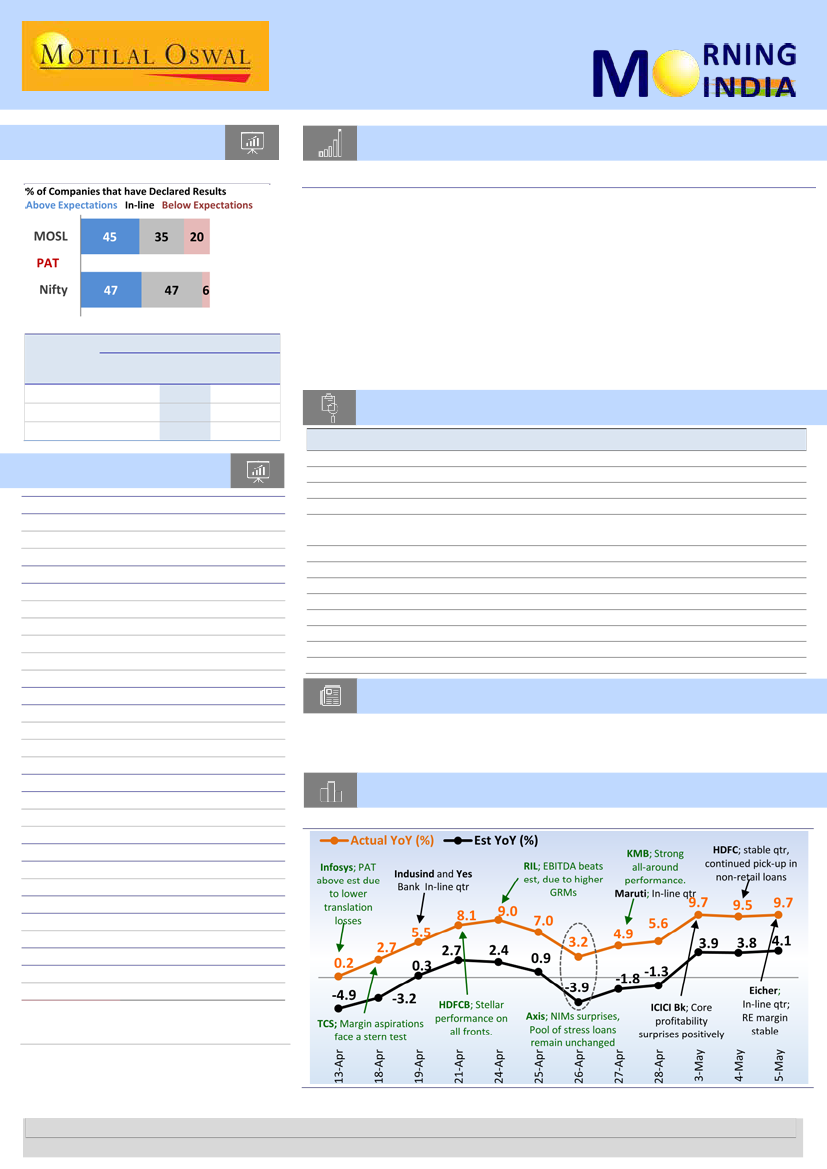

Chart of the Day: Nifty-50: Performance-expectation gap

4QFY17 PAT growth for 17 companies that have declared results

Quote of the day

Keep your eye on the goal, keep moving

toward your target

Research Team (Gautam.Duggad@MotilalOswal.com)

Source: Company, MOSL

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

Investors are advised to refer through important disclosures made at the last page of the Research Report.