Godrej Consumer

BSE SENSEX

29,933

Bloomberg

Equity Shares (m)

M.Cap.(INRb)/(USDb)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

Avg Val, INRm/ Vol ‘000

Free float (%)

S&P CNX

9,317

GCPL IN

340.6

656.8 / 9.9

1956 / 1286

13/20/27

354

36.7

9 May 2017

Q4FY17 Results Update | Sector: Consumer

CMP: INR1,929

TP:INR1,950(+1%)

Neutral

Domestic branded volumes grow 5% led by Hair color portfolio

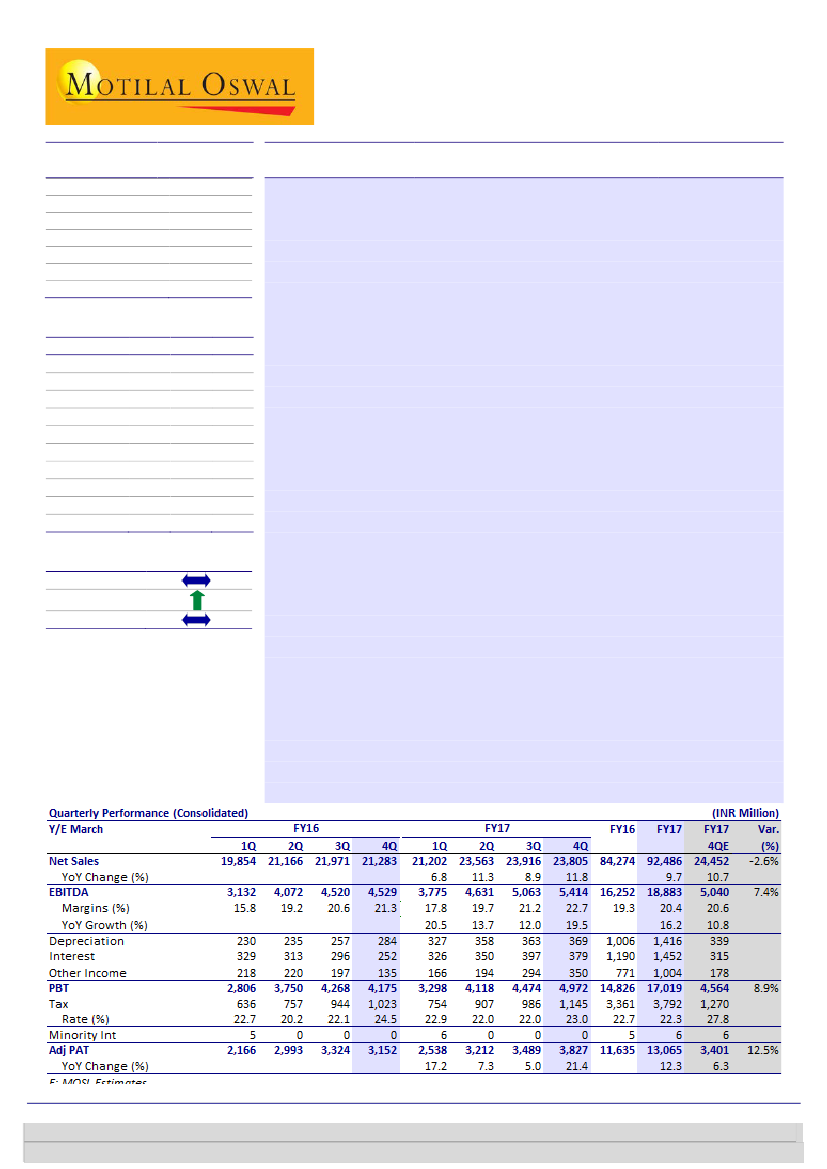

Godrej Consumer’s (GCPL) 4QFY17 consol. net sales grew 11.8% YoY

to

INR23.8b (est. of INR24.5b). Consol. EBITDA growth of 19.5% YoY to INR5.4b

(est. of INR5.04b) and adj. PAT growth of 21.4% YoY to INR3.83b (est. of

INR3.4b) were both better than expectations. Organic consol. CC sales grew 6%

YoY, while India business sales were up strongly by 10% YoY in 4QFY17.

Gross margin expanded 260bp YoY to 56.6%.

Ad spend to sales declined 70bp

YoY to 6.5%, but the fall was not as steep as witnessed by peers for the

quarter. EBITDA margin expanded 150bp YoY to 22.7% in 4QFY17. Consol.

EBITDA grew 19.5% YoY to INR5.4b (est. of INR5.04b). Thus, despite consol.

sales being 2.6% below expectations, EBITDA was 7.4% ahead of forecasts.

Higher-than-expected other income and a lower-than-forecast tax rate led to

PAT beat of 12.5%. Adj. PAT grew 21.4% YoY to INR3.83b (est. of INR3.4b).

India branded business volume growth stood at 5% YoY.

Household

Insecticides business reported 4% YoY sales growth, Soaps grew 9% YoY, while

Hair color sales were up 13% YoY (double-digit revenue growth in Hair colors

after five quarters).

International:

CC sales grew 22% YoY (with 1% organic sales growth). On CC

basis, Indonesia sales were flat, Africa/LatAM grew 61%/19%, while Europe

sales declined 5%.

FY17 performance:

Consol. sales, EBITDA and adj. PAT growth stood at 9.7%,

16.2% and 12.3%, respectively.

Valuation and view:

At 38.6x March 2019E EPS, the stock appears fairly valued.

While earnings growth has been more consistent than FMCG peers (FY17

reported eighth consecutive year of double-digit EBITDA and PAT growth), we

believe that due to its exposure to various geographies, attendant currency

risks and relatively low RoE (mid-20s), the stock does not warrant a higher

multiple. Maintain

Neutral

with TP of INR1,950 (39x March-19E EPS, a 10%

premium to 3-year average owing to higher earnings consistency relative to

peers).

Financials & Valuation (INR b)

Y/E Mar

2017 2018E 2019E

Net Sales

92.4 107.3 122.4

EBITDA

18.9

22.1

24.9

PAT

12.9

14.8

17.0

EPS (INR)

37.8

43.6

50.0

Gr. (%)

12.4

15.4

14.6

BV/Sh (INR)

155.7 200.6 233.5

RoE (%)

24.6

24.5

23.0

RoCE (%)

16.8

16.6

16.5

P/E (x)

51.0

44.2

38.6

P/BV (x)

12.4

9.6

8.3

Estimate change

TP change

Rating change

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

Krishnan Sambamoorthy

(Krishnan.Sambamoorthy@motilaloswal.com); +91 22 3027 8029

Vishal Punmiya

(Vishal.Punmiya@motilaloswal.com); +91 22 3980 4261