Oriental Bank of Commerce

BSE SENSEX

30,188

Bloomberg

Equity Shares (m)

M.Cap.(INRb)/(USDb)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

Avg Val, INRm

Free float (%)

Financials & Valuations (INR b)

Y/E March

2017 2018E

NII

49.1

52.9

OP

41.7

37.6

NP

NM

5.9

EPS (INR)

-31.6

17.1

EPS Growth (%)

NM

NM

BV/Sh. (INR)

365.3

382.3

RoE (%)

-8.4

4.6

RoA (%)

-0.4

0.2

P/E (x)

-5.2

9.6

P/BV (x)

0.45

0.43

S&P CNX

9,401

OBC IN

Another weak quarter; Stress addition increases to AQR levels

346.2

OBC reported loss of INR12.2b (~2x of FY15 and FY16 PAT combined) v/s est.

43.3 / 0.6

loss of INR1.1b, primarily due to elevated credit costs of INR30.5b (8.2%

138 / 75

annualized, highest in the history of the bank). Asset quality remains under

7/4/4

469

pressure, led by elevated stress additions (INR39b v/s INR27b in 3Q) and

41.6

muted recoveries/upgrades.

12 May 2017

4QFY17 Results Update | Sector: Financials

CMP: INR163

TP: INR150 (-8%)

Neutral

2019E

58.2

41.4

7.4

21.4

25.3

403.7

5.4

0.3

7.6

0.40

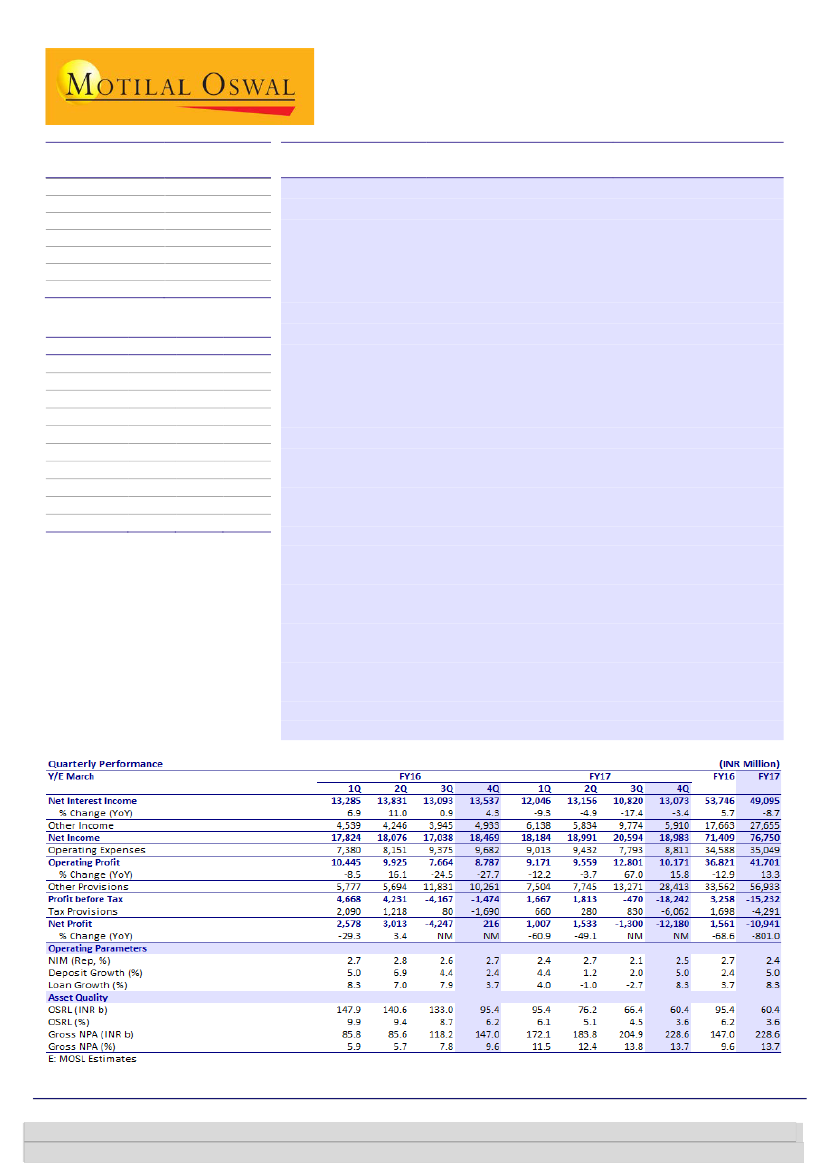

Overall pool of NSL (NNPA+ OSRL+ all other forms of stress) was stable QoQ

at ~14.5%; large relapse into NPA from restructured portfolio (INR9.4b) and

SDR/S4A accounts (8 accounts amounting to INR16.9b). Steel accounted for

28% of overall slippages. This sector already has 68% NPA, and management

does not expect incremental large slippages from this book. Absolute GNPAs

increased 12% QoQ, but remained stable in % terms at 13.7% due to strong

sequential loan growth (11%) and large write-offs (INR11b).

NII grew 21% QoQ to INR13b (in-line), led by NIM improvement of ~40bp

QoQ to 2.5%. NIM was aided by a sharp fall in CoF of ~38bp QoQ.

FY17 highlights:

(1) Operating profit for FY17 grew 13% YoY; however, high

NPL provisions of ~57b led to pre-tax loss. (2) Overall gross advances grew

8.3%, with strong growth in retail loans of ~37.2%.

Other highlights:

(1) Trading gains declined 70% QoQ, driving 15% miss in

other income. (2) CASA ratio declined 180bp QoQ to 30.5% owing to

redemption of temporary SA deposits (-6% QoQ) built up post demon. (3)

CET1 declined 113bp, led by large quantum of losses during the quarter.

Valuation and view:

Sharp rise in slippages continues to remain a concern

for the bank. NPL ageing will result in high expected credit costs in FY18/19.

Return ratios are likely to be sub-optimal at 0.2/5% RoA/RoE, and hence, we

downgrade our earnings by 19% for FY18. Resolutions in key stress sectors

like steel remain a key trigger for the bank. Maintain

Neutral

with a TP of

INR150 (0.4x FY19BV).

Alpesh Mehta

(Alpesh.Mehta@MotilalOswal.com); +91 22 6129 1526

Subham Banka

(Subham.Banka@MotilalOswal.com); +91 022 6129 1567

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.