17 October 2017

Q2FY18 Results Update | Sector: Technology

Wipro

Neutral

BSE SENSEX

32,634

Bloomberg

Equity Shares (m)

M.Cap.(INRb)/(USDb)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

Avg Val, INRm

Free float (%)

S&P CNX

10,231

WPRO IN

Asymmetrical growth dynamics…

4,867

…continue restricting broad-based revival

1,411.6 / 21.8

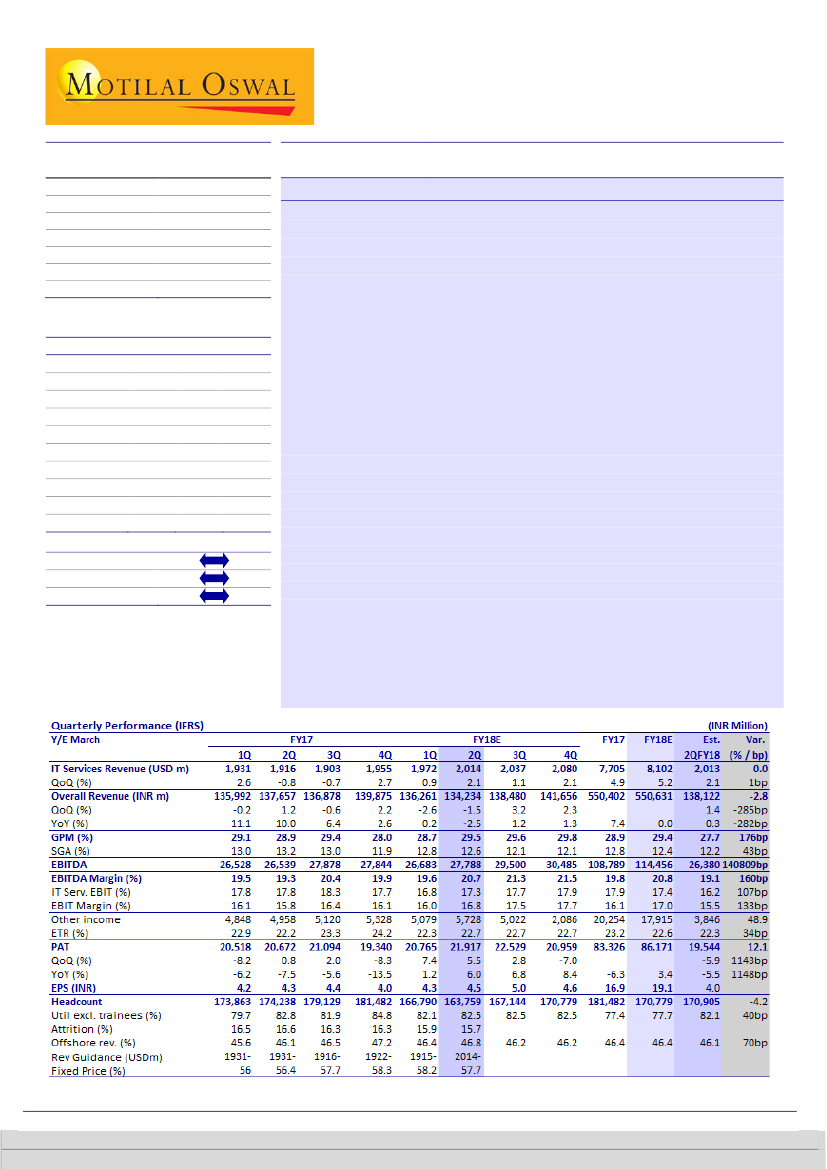

Revenue growth below expectations:

2QFY18 CC revenue growth of 0.3%

304 / 205

QoQ was below our estimate of 1% QoQ and at the lower end of WPRO’s

0/5/4

guidance of -0.5% to +1.5% QoQ. Barring Communications (-4.4% QoQ CC)

868.5

and Healthcare (-5.9%), performance across verticals was impressive, mainly

26.8

CMP: INR290

TP: INR280(-3%)

Financials & Valuations (INR b)

2017 2018E

Y/E Mar

550.4

550.6

Net Sales

108.8

114.5

EBITDA

83.3

86.2

PAT

16.9

19.1

EPS (INR)

-6.3

13.0

Gr. (%)

105.9

110.3

BV/Sh (INR)

16.9

17.0

RoE (%)

13.6

13.9

RoCE (%)

17.1

15.2

P/E (x)

2.7

2.6

P/BV (x)

2019E

598.7

129.3

90.7

20.1

5.2

130.4

16.7

15.2

14.4

2.2

Estimate change

TP change

Rating change

in BFSI (+3.3%). Though WPRO expects bottoming out of these problem

areas, the guidance tells a different story.

3Q guidance not signifying revival:

For 3Q, WPRO expects revenue of

USD2,014-2,054m, implying CC growth of 0-2%. On YoY CC basis, this implies

growth of 2.3-4.4% for 3Q, which at its midpoint is not materially higher

than +2.9% YoY CC in 2Q. Given that the two problem verticals alone pulled

overall growth down by 180bp QoQ, a revival there is necessary to translate

into broad-based performance; portfolio issues and lopsided growth are a

familiar story in the case of WPRO.

Profitability beat across businesses:

IT Services EBIT margin at 17.3% (+50bp

QoQ) beat our estimate by 110bp. Margin expansion, despite wage hike

impact, was commendable, driven by improved operational efficiency (also

reflected in steady 80%+ utilization and headcount reduction). Products

business saw sharp profitability improvement as WPRO consolidated its

operations (business is half the size of previous quarter). This aided overall

EBIT margin of 16.8% (130bp beat). Apart from this, higher other income led

to PAT of INR21.9b (+5.5% QoQ, est. of -5.9% QoQ).

Valuation view:

We raise EPS by 3% for FY19/20E, factoring in margin beat

in Services/Products. However, we believe it would be crucial for WPRO to

start seeing recovery on organic growth and it to be reflected in optimistic

guidance to sustain current valuations. WPRO trades at 15.2/14.4x FY18/

FY19E EPS. We expect revenues/earnings (led by buyback) CAGR of 6.3/9.0%

over FY17-19E. Our TP of INR280 discounts FY19E EPS by 14x.

Neutral.

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

Ashish Chopra – Research Analyst

(Ashish.Chopra@MotilalOswal.com); +91 22 6129 1530

Sagar Lele – Research Analyst

(Sagar.Lele@MotilalOswal.com); +91 22 6129 1531